Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

A view from the Member's Gallery inside the NYSE. Photo by Ryan Lawler. Wiki Commons. Used with permission. On Feb. 5, 2018, after a drop of 666 points in the Dow Jones Industrial Average on Friday, Feb. 2, 2018, the Dow Jones Industrial Average experienced the single biggest point drop in its history – of 1,175. That put Wall Street flat so far on the year, even with the “Tuesday Turnaround,” and has raised questions of whether the U.S. might experience a long-overdue correction soon, or if this is the beginning of a bear market. Alan Greenspan said bluntly on January 31, 2018 that “We have a stock market bubble, and we have a bond market bubble.” With real estate prices at all-time highs, consumer debt at all time highs and U.S. public debt in the stratosphere, you could say we have five bubbles. 4 Things the 1,175 drop on Monday taught us.

And here is additional information on each line item. 1. The descent will be rapid. Anytime you have a landmark occurrence, it pays to pay attention. Why did the Dow drop so far so fast? The Dow dumped 800 points in 10-minutes, very similar to the Flash Crash of 2010. About 30% of trades on Wall Street are “quant-focused,” sophisticated math formulas that have little to do with consumer trends and balance sheets, run by computers, not humans. With hedge funds dominating the trading, there is also a cascading effect of puts and calls that kick in automatically in certain scenarios, causing whichever direction the market is heading to ratchet up to time-warp in seconds. On Wall Street, this is referred to as trying to “catch a falling knife.” 2. Time to get a second opinion. You probably remember what it felt like on March 9, 2009, when the Dow sank to a low of 6547. If you lost more than 1/3 in your retirement plan/nest egg then, it’s not because the markets dropped. It is because your investments are not properly diversified. Don’t expect the broker-salesman who designed your plan to make changes. Many times they simply get paid a lot more to put you more at risk than you should be. There is an inherent conflict of interest between many financial advisors and their clients. Once you learn the ABCs of Money that we all should have received in high school, which includes an easy formula for a healthy nest egg, then you can be the boss of your money and make sure that your wealth strategy is sound. Until then, especially if you are losing 1/3 or more every eight years in recessions, you are vulnerable to market downturns and recessions. The markets do not just keep going up, up, up forever. 3. Volatility is back. From the beginning of 2014 to the end of 2016, stocks were essentially flat, with cliffs and valleys of volatility. 2016 has enjoyed a rise of euphoria, largely on corporate buybacks. Corporations could borrow money almost free and then repurchase their own stock, something that typically makes investors interested in buying, too. So, what happened last Friday and Monday? Who sold? It’s difficult to know which large institution initiated the massive sell-off. However, once the selling began, the programed algorithms kicked into gear, trying to leapfrog other big sellers at a better price. That kind of volatility is rigged into today’s trading. It worked to investor’s favor in 2016. But it works against investors when the correction occurs. 4. Bitcoin isn’t the answer. Bitcoin is an exciting new currency, with implications far beyond just having an alternative payment source (such as the technological innovation of blockchain). However, few people are actually using Bitcoin (or Ethereum or Litecoin) to buy or sell anything. For the most part, the massive price movements are happening as a result of trading. Big hedge funds have joined the trading game, meaning winning against these titans is about as easy as winning a tennis match against Roger Federer. In addition, there re an extraordinary amount of MLM scams in this space. Do not buy into anything until you are fully informed, and only with money that you are willing to lose. It’s still the Wild West in crytocurrency, and quite frankly, the SEC and FINRA can’t keep up with the amount of sketchy shysters in the space.  Coinbase Chart. February 7, 2018. https://www.coinbase.com/charts. What Does This Mean For Your Pension, Annuity, 401K, IRA and Future? Isn’t economic growth the story? The rise of Wall Street? That is what the politicians want to focus on. However, behind the scenes there is a sea of red flags that you should be aware of. Some are listed below. Pension plans are severely underfunded, by over half a trillion dollars. Annuities shave almost 10% off of your principal the minute you purchase them (surrender fees). Insurance companies, the only “guarantee” behind your annuity and policy, wouldn’t even be in business today, if they hadn’t been bailed out in 2008. AIG lost money this year. Many publicly traded companies have lower earnings this quarter over last year. Market downturns tend to exacerbate things. You Shouldn’t Panic. You Should Act, However. Employ a Time-Proven System, Not a Long-term Mind Frame (which is a time-proven loser) I’m seeing lots of media coverage where “experts” say that you should do nothing on days like yesterday, and that you need to employ a long-term mind frame. That’s good advice only if your plan works. That is terrible advice in today’s marketplace. Buy and Hold only works when the general economic trend is up. That was the case from World War II through Y2K. However, since 2000, we’ve seen two catastrophic recessions, where investors lost more than half, and then barely crawl back to even before losing half again. So, rather than do nothing or have a long-term view, it’s a very good time to treat Monday like a wake-up call. Know what you own, and know that your plan is well-diversified and that you are protected from the next recession. You cannot simply have blind faith in what your broker-salesman is telling you, particularly if the proof of the inefficacy of your plan lies in your losses in the Great Recession and the Dot Com Recession. Here’s the Math Riding the Wall Street rollercoaster has been devastating in the New Millennium. Your stock broker might say, “Yes, but the markets always come back.” However, they are neglecting to tell you that when you lose more than half, your assets take twice as long to recover. That is because a 10% return on $1,000,000 is $100,000 whereas a 10% return on $450,000 is $45,000. So, a loss of $550,000 can take more than a decade to recover. In both the NASDAQ Dot Com Recession (2000-2002) and the Great Recession (2008), the next devastating drop occurred before investors had a chance to fully recover. So, What Time-Proven Nest Egg Strategies Do Work? Call 310-430-2397 to find out easy strategies that have earned gains in both of the last two recessions, and have outperformed the bull markets in between.  Red Flags in the Economy

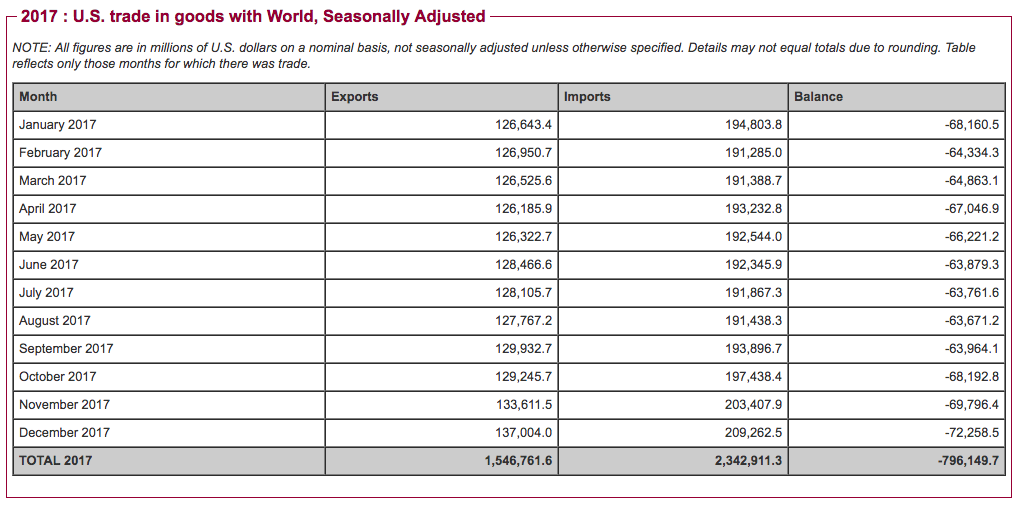

Source: Census.gov. Trade in Goods with World. These red flags are all things that the quant-based hedge funds are overlooking, for now. However, as we saw on Monday, when the view turns toward the challenges, the correction is like trying to catch a falling knife.

Being ahead of that trend is a life-saver, a nest egg saver. Call 310-430-2397 now to learn more. Other Articles of Interest Why Did the Dow Drop 666 on Friday? Feb. 3, 2018. Warren Buffett is On the Sidelines. GE Investors Lose Half. Bitcoin and the Cryptocurrency Flash Crash.

Sterling Harris

10/2/2018 09:21:10 am

is Natalie going to be having any teleconferences, blog radio about this gathering storm clouds anytime soon. i realize she is prepping for her February event at the moment. 28/2/2018 01:58:14 pm

Hi Sterling, Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed