Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

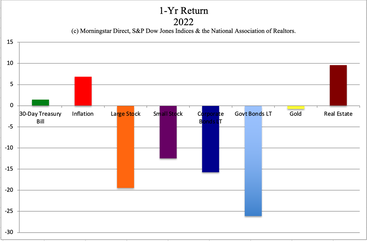

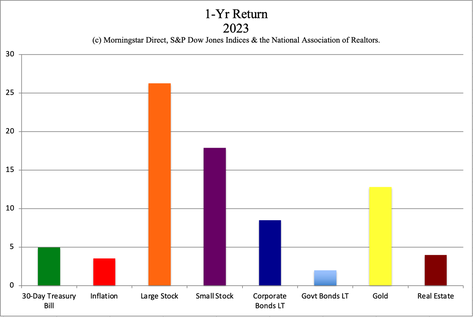

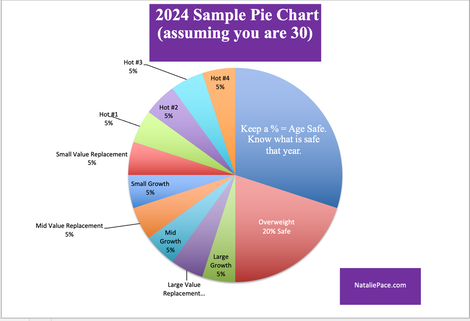

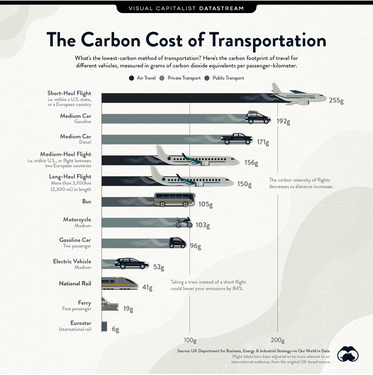

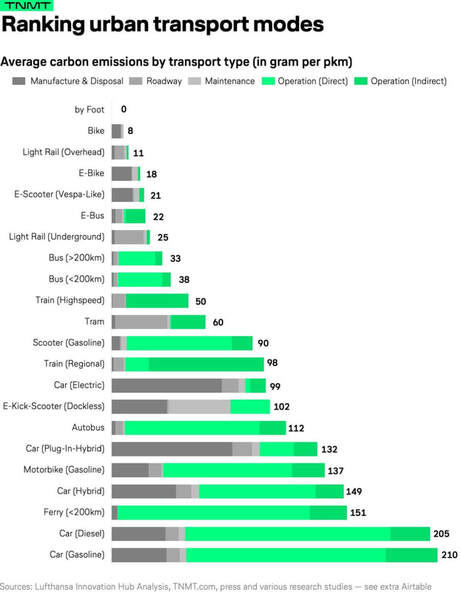

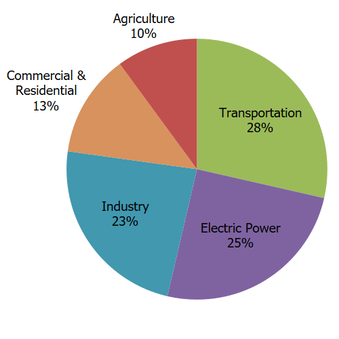

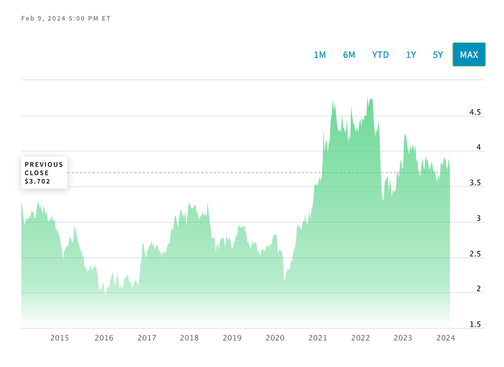

Stocks are Flying High. Why Aren’t Mine? Investors Ask Natalie. Dear Natalie: Every day I hear that stocks are hitting new highs. Yet my personal plan isn’t seeing such spectacular gains, and many of my positions are losing money. Why aren’t my stocks performing as well as the stock market is? Not FOMO – RMO (Really Missing Out) Dear Really Missing Out, Your brokerage statement is showing that your returns were terrible last year, with 26% total gains in 2023 in the S&P500 vs. your 5% gain. FYI: The Dow Jones Industrial Average gains were only 13.9% in 2023. Without the Magnificent 7, the S&P500 gains would have been just 9.94%. It's also important to put things in perspective. As you can see in the chart above, the superior returns of 2023 didn't even bring the S&P500 back to the highs of 2021. The index finally started ringing in new highs this month -- February of 2024. In addition to having a properly diversified plan that protects our wealth, it's important to rebalance regularly to capture gains. Otherwise, we could be riding a Wall Street rollercoaster (as is exemplified in the performance chart above.) After taking a look at your plan, there are a few problem areas that are causing your portfolio to severely lag the performance of the S&P500. These issues are pretty common in both retirement plans (especially those target date retirement funds) and managed portfolios. So I’m encouraging everybody to take a forensic look at their statements, and see how your plan is performing next to the S&P500. Many plans are performing at half the speed, and some, particularly for people who are closer to retirement, might even be losing money. Here’s why. Five reasons many portfolios are lagging the spectacular 2023 performance of the S&P 500. 1. The Magnificent 7 2. Long-Term Bonds 3. Missing Hot Industries 4. Overweighted in Value 5. Underweighted in Growth And here is more information on each point. 1. The Magnificent 7 A lot of people aren’t aware that the Magnificent 7 is largely responsible for Wall Street ringing up record highs this month. The Magnificent 7 stocks have doubled over the last year. Nvidia more than tripled. As you can see in the data I listed at the top of this blog, without the support of the Magnificent 7, the stock market would’ve been up 13%-ish rather than 26%. You don’t have any large cap growth in your portfolio (where the Magnificent 7 stocks would be), or a fund that specializes in the Magnificent 7. The few stocks you have are ones that actually lost money. 30% of the Dow Jones Industrial Average companies lost money in 2023. (Click on the blue-highlights to read more.) 2. Long-Term Bonds Long-term bonds lost even more than stocks did in 2022, at -26%. 2023 saw a small recovery, but nowhere enough to make up for the losses in 2022. Since this is on the safe side of our portfolios, it’s very important to know what is safe in the post-pandemic Debt World that we live in. Even the banks, with their Ivy-League C-Suites, are having trouble getting this right, as evidenced in the bank failures. (We’re still underweighting the financials industry, including insurance companies and brokerages.)   Everyone is counting on a recovery of bonds if interest rates start getting cut in the latter part of 2024 and in 2025. However, there’s a great deal of duration risk and credit risk that remain even if the interest rate risk has abated. With regard to bonds, it’s a good idea to keep the terms short and the creditworthiness high until the duration and credit risks have been worked out. (That process can be painful to bond investors who have skin in the game.) We spend one full day on What’s Safe in our Financial Freedom Retreat. Commercial real estate is one of the areas of heightened risk in bonds and the economy, with potential ramifications on the banking industry and financial stability. 3. Missing Hot Industries In addition to having large cap growth and proper size/style diversification, we could lean in even more to the Magnificent 7, with a hot slice in our nest egg pie chart. It’s a good idea to invest in hot industries, such as artificial intelligence, cyber security, copper, crypto, gold, or even other countries. A well-diversified portfolio can include up to four slices of hot industries. Regular rebalancing helps us to capture and keep our gains when a particular industry or country shoots the moon, rather than riding the Wall Street rollercoaster. This plan, which we teach at our retreat, also helps us to invest the appropriate amount, rather than bet the farm.  4. Overweighted in Value Value funds are very problematic, particularly in the United States. When stocks are at all-time highs with elevated price-earnings ratios, nothing is actually on sale. The other side of the issue is that the companies/funds that are trading for a muted price tend to be market laggards with a great deal of concerns, including massive debt, pension and other post-employment benefit liabilities, and slow growth. Many of the Dow components that lost money in 2023 are stuck in the value funds. For this reason, we’re suggesting value replacement funds in our sample pie charts. We can diversify into other countries and get exposure to industries that are very underweighted in most of the U.S. funds, including materials, utilities, and consumer staples. As I mentioned above, many of these funds offer a higher dividend, and some also come with higher credit quality. 5. Underweighted in Growth Growth funds offer much lower dividends than value funds. However, missing out on growth industries in 2023, such as artificial intelligence, cyber security and technology, meant we missed out on the spectacular gains of equities. Knowing what we own, and having the proper mix of value, growth, small, medium and large caps, and hot industries, is a great way to protect our wealth, while also improving performance. Bottom Line Your plan has too many long-term bonds, bond funds and value stocks. This could continue to be a problem even if interest rates get cut. So, now is the time to get properly diversified and protected. If others reading this blog are worried about their wealth plan, now is the time to really know how to read your brokerage statement properly. The statement should reveal what your portfolio performance is compared to the S&P500 over the last year, and even the five or 10-year period. Knowing why your plan is underperforming might require getting an unbiased 2nd opinion. I have a coaching client who was told that he was earning 5-7% on his “conservative” investments. The real return was under 2%, due to the principal loss in value of his holdings. This was written in plain sight on the statement. He (and many of us, really) just didn’t know where to locate that information, and how to decipher the document. (Click to learn more.) When we consider how much money we have in our retirement plans and brokerage accounts, it can be more than we make in many years of earned income. So, being the boss of our money and protecting our wealth, while growing the at-risk side safely on par with the S&P 500, can be time and wisdom that is well-spent. Once we learn the life math that we all should’ve received in high school and college, and implement these strategies, all we need to do is to rebalance once, twice, or three times a year. Once we build our solid financial house, we just need to Spring clean once a year. (If you’d like an unbiased 2nd opinion on your plan, such as the person sending in this question received, email [email protected] for pricing and information.) Join us at our April 27-29, 2024 Spring Financial Freedom Retreat. Learn how to invest and grow your wealth, green your retirement plan, easy and efficacious nest egg strategies, how to get hot and diversified (including in artificial intelligence), and what's safe in a Debt World. You'll even discover how to save thousands annually with smarter big-ticket choices. Yes, it's a complete money makeover. Email [email protected] to register. Learn the 15+ things you'll master and read testimonials in the flyer on the home page at NataliePace.com. Register by Feb. 29, 2024 to receive the best price. "Ten minutes into the first day I was already much smarter about investing than I ever thought I would be in my life and I knew I was in exactly the right place at this retreat. I am amazed at how EASY and FUN it is to make my money work for me and those I love. I think this kind of information should be compulsory in schools. I wish I'd learned this sooner." CM  Join us for our Online Spring Financial Freedom Retreat. April 27-29, 2024. Email [email protected] or call 310-430-2397 to learn more. Register by Feb. 29, 2024 to receive the best price. Click for testimonials, pricing, hours & details.  Join us for our Restormel Royal Immersive Adventure Retreat. March 7-14, 2025. Email [email protected] to learn more. Register by April 30, 2024 to receive $200 off the regular price. Click for testimonials, pricing, hours & details. There is very limited availability, and you must register early to ensure that you get the exact room you want. This retreat includes an all-access pass to all of our online training for a full year for two and three 50-minute private, prosperity coaching sessions!  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money and the 2nd edition of Put Your Money Where Your Heart Is are the most recent releases of these books. Follow her on Instagram. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Substack podcast on Apple and Spotify. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Cut Your Tax Bill in Half. 9 Tips. Celebrity Jet CO2. Green Washing. The Facts. Some Solutions. Copper: Essential to the Clean Energy Transition. Uh. Oh. More Bank Trouble. Are Amazon, Square and Other Tech Companies Ripping Us Off? Housing. Unaffordable. What Works? Case studies and creative solutions. Don't Reach for Yield. Closed-End Funds. 2024 Investor IQ Test. Answers to the 2024 Investor IQ Test. Apple's Woes Drag Down the Dow. The Winners & Losers of 2023. Ozempic, Magnificent 7 & Beyond. 2024 Crystal Ball. The Underperforming DJIA, Full of Fossil Fuels and Forever Chemicals. A Spectacular Year for 3 of the Magnificent 7. The Best ROI* (Almost 40%!) & 7 Life Hacks That Save Thousands. Portugal Eliminates Tax Advantages for Ex-Pats. Holiday Gift Giving on any Budget. Including No Budget. Once in a Century Events are Happening Every Day. The Crypto Winter Enters Its 3rd Year. Earn $50,000 or More in Interest. Safely. Finally. Freebies and Deals for Black Friday and Cyber Monday. Auto Strikes End. EV Price Wars Continue. WeWork's Bankruptcy. Half-Empty Office Buildings. Problems in our Personal Wealth Plan. Solutions for Unaffordable Housing. Cruise Ships Give Freebies to Investors. Should You Take the Bait? Should You Take a Cruise? Bonds. Banks. The Treacherous Landscape of Keeping Our Money Safe. 7 Rules of Investing Air B N Bust? Barbie. Oppenheimer. Strikes. Streaming Wars. Netflix. Monero: A Token of Trust? 13 Lifestyle Choices to Reduce Waste, Pollution & CO2 & Save a Boatload of Dough. China Bans Apple 11-Point Green Checklist for Schools. Artificial Intelligence and Nvidia's Blockbuster Earnings Report Biotech in a Post-Pandemic World 10 Wealth Secrets of Billionaires and Royals. What Happened to Cannabis? Bank of America has $100 Billion in Bond Losses (on Paper) Lithium. Essential to EV Life. I'm Just Not Good at Investing. Investors Ask Natalie. Should I Buy an S&P500 Index Fund? Investors Ask Natalie. Bonds Lost More than Stocks in 2022. Do Cybersecurity Risks Create Investor Opportunities? I Lost $100,000. Investors Ask Natalie. Artificial Intelligence Report. Micron Banned in China. Intel Slashes Dividend. Buffett Loses $23 Billion. Branson's Virgin Orbit Declares Bankruptcy. Insurance Company Risks. Schwab Loses $41 Billion in Cash Deposits. Fiat. Crypto. Gold. BRICS. Real Estate. Alternative Investments. BRICS Currency. Will the Dollar Become Extinct? The Online Global Earth Gratitude Celebration 7 Green Life Hacks Fossil Fuels Touch Every Part of Our Lives Are There Any Safe, Green Banks? 7 Ways to Stash Your Cash Now. Lessons from the Silicon Valley Bank Failure. Which Countries Offer the Highest Yield for the Lowest Risk? Why We Are Underweighting Banks and the Financial Industry. 2023 Bond Strategy Emotions are Not Your Friend in Investing Bonds Lost -26%, Silver Held Strong. Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  Natalie Pace in Powerscourt, Ireland. Photo by: Marie Commiskey. Cut Your Tax Bill in Half! 9 Tips. A lot of you have heard me say, “Stop making everyone else rich, including the tax man, the debt collector, the landlord, the gas station, the utility company, the insurance salesman, etc.” Tax season is the perfect time to start keeping more of your dough, which you can then use to invest (money while you sleep), to have more fun, and to buy things you like a lot more than the IRS. Even if you are taking the standard deduction, you’ll want to know about these strategies because many are tax credits that apply whether or not you itemize. Additionally, these strategies can also save us thousands annually in our budget. Below are 9 tips to start on the path. 9 Tips to Stop Making the Tax Man Rich! These tips will help you put your best leg forward on the path to financial freedom. See the list below for what applies to you, and then details on each tax credit/deduction below the list. 1. Health Savings Accounts. 2. IRA Contributions. 3. Mortgage Interest Deduction 4. Student Loan Interest Deduction. 5. Qualified Education Expenses. 6. Energy Efficiency and Clean Power Tax Credits. 7. Charitable Contributions. 8. Capital Gains 9. Facing an Audit or Tax Levy? 1. Health Savings Accounts. HSAs are one way to increase your net worth and beautify your bottom line, while giving less to Uncle Sam AND the health insurance company. Health Savings Accounts work best for healthy people. An HSA, combined with a high deductible health insurance, could save you thousands of dollars in insurance premiums each year. The IRS offers an annual tax credit of $3,850 for individuals (and $7,750 for families), which can be invested for tax-free gains. (This increases to $4,150 and $8,300, respectively, in 2024.) The tax benefit is available even if you don’t itemize deductions. To learn more, visit IRS.Gov and enter Health Savings Accounts in the search box. NOTE that opening a HSA with a brokerage should offer you more investment options than opening the account with an insurance company or bank. 2. IRA Contributions: You can still contribute to your IRA and receive credit for 2023, up until April 15, 2024. (Roth IRAs are not tax deductible.) Should you opt for a Roth, a traditional IRA or a SEP IRA? Most people earn more in their working years, when they can most benefit from the tax credit, and less in their retirement years, when they will have to pay income taxes on their traditional IRA (but not their Roth IRA). Peter Thiel reportedly has over $5 billion in his Roth IRA (source: ProPublica). If you are self-employed, consider a SEP-IRA, where you might be able to sock away $27,000 (50+) or $20,500 (under 50) each year. All of these IRAs offer tax-free gains. Self-directed IRAs offer more freedom of choice in your investments than 401Ks, RSPs, 529Bs, etc. So, rather than just maxing out your employer-offered retirement plan, it’s a good idea to contribute up to the employer match, and then consider maxing out your HSA and personal IRA. We discuss this in greater detail at our Financial Freedom Retreats.  Join us for our Online Spring Financial Freedom Retreat. April 27-29, 2024. Email [email protected] or call 310-430-2397 to learn more. Register by Feb. 29, 2024 to receive the best price. Click for testimonials, pricing, hours & details. 3. Mortgage Interest Deduction. Mortgage interest paid on a qualified first and second home can be deducted. Click to read the IRS rules. This is a huge tax deduction that allows us to stop making the landlord rich, and pay less to the taxman. Home prices on a nationwide basis are at all-time highs and are largely unaffordable, so it’s not a great idea to just race out and purchase. (Over 20 million homes were foreclosed on before, during and after the Great Recession.) However, there are opportunities for smart buyers to rethink their housing and to vision and prepare, so that they can create a win-win-win for themselves when the opportunities arise again. These are some of the tools we teach in our Investor Educational Retreats. You can also read case studies in the Real Estate section of The ABCs of Money, 5th edition. 4. Student Loan Interest Deduction. If you earned less than $90,000 in MAGI (modified adjusted gross income) in 2023, and you paid on a student loan, you could deduct up to $2,500 of the interest you paid. 5. Qualified Education Expenses. You may be able to deduct education costs for yourself and/or a student in your immediate family. You may also be able to take an early distribution from an IRA without paying the early distribution penalty and additional taxes, if the withdrawal was made to cover a qualified education expense. And if the education is work-related, you may qualify for a Lifetime Learning Credit or a business deduction. 6. Energy Efficiency Credits. If you made energy-efficiency improvements to your home, you could qualify for up to $3,200 in tax credits. If you purchased an electric vehicle or installed solar or wind energy products, you could qualify for a generous tax credit. EV credits go up to $7,500 and wind/solar power products can be as high as 30 percent of the purchase price. The EV tax credit and the Residential Clean Energy Credit are both good through 2032. Certain rules apply to both, so be sure to visit the IRS pages and understand how to dot the I’s and cross the T’s. 7. Charitable Contributions. Your charitable contribution is tax deductible, provided it is made to a qualified 501c3. In addition to deducting your cash contributions, you generally can deduct the fair market value of any property you donate to qualified organizations. It is my experience that donating goods yields a better value in tax credits than you’d earn sitting all day through a yard sale. 8. Capital Gains. It’s important to do as much of our investing as possible in tax-protected retirement accounts. Doing so can eliminate capital gains taxes, which can be up to 37% for short-term capital gains. Did you know that you can even invest in real estate in your IRA? Email [email protected] to learn more. 9. Facing an Audit or Tax Levy? Hire an experienced, qualified accountant to review your case and communicate with the IRS on your behalf. As Wayne Layton, CPA, reminds us: "From time to time the IRS may suspect an error on a tax return or underpayment of tax and send my clients a letter assessing additional tax, along with penalties and interest. Most taxpayers become fearful upon receiving these letters as some of them even refer to liens and levies. Out of fear, many people just write a check to the IRS. As I see it, the letters from the IRS are simply telling the taxpayer to pay or prove why you do not owe the balance. There are many times that, on behalf of my clients, I write a letter disagreeing with the IRS’s position, attaching proof of why the taxpayer does not owe the additional tax, and the additional tax assessed is either reduced or the balance is adjusted to zero." Sometimes the IRS will agree with the accountant and adjust the balance due. Other times, if there is a good reason, the IRS may waive the penalties. And, of course, there may be times when you have to pay everything the IRS claims is owed. Most importantly, do not simply write the check before discussing your options with a qualified Certified Public Accountant. Bottom Line You don’t need to itemize deductions to take a tax credit. Many of the above tax benefits are available whether or not we itemize, and almost all of them offer additional savings in health premiums, capital gains taxes, utility costs, housing, gasoline and more. We can live a much richer life when we learn how to keep more of our money and stop making the taxman and billionaire corporations rich at our own expense. Join us at our April 27-29, 2024 Spring Financial Freedom Retreat. Learn how to invest and grow your wealth, green your retirement plan, easy and efficacious nest egg strategies, how to get hot and diversified (including in artificial intelligence), and what's safe in a Debt World. You'll even discover how to save thousands annually with smarter big-ticket choices. Yes, it's a complete money makeover. Email [email protected] to register. Learn the 15+ things you'll master and read testimonials in the flyer on the home page at NataliePace.com. Register by Feb. 29, 2024 to receive the best price. "Ten minutes into the first day I was already much smarter about investing than I ever thought I would be in my life and I knew I was in exactly the right place at this retreat. I am amazed at how EASY and FUN it is to make my money work for me and those I love. I think this kind of information should be compulsory in schools. I wish I'd learned this sooner." CM  Join us for our Online Spring Financial Freedom Retreat. April 27-29, 2024. Email [email protected] or call 310-430-2397 to learn more. Register by Feb. 29, 2024 to receive the best price. Click for testimonials, pricing, hours & details.  Join us for our Restormel Royal Immersive Adventure Retreat. March 7-14, 2025. Email [email protected] to learn more. Register by April 30, 2024 to receive $200 off the regular price. Click for testimonials, pricing, hours & details. There is very limited availability, and you must register early to ensure that you get the exact room you want. This retreat includes an all-access pass to all of our online training for a full year for two and three 50-minute private, prosperity coaching sessions!  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money and the 2nd edition of Put Your Money Where Your Heart Is are the most recent releases of these books. Follow her on Instagram. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Substack podcast on Apple and Spotify. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Celebrity Jet CO2. Green Washing. The Facts. Some Solutions. Copper: Essential to the Clean Energy Transition. Uh. Oh. More Bank Trouble. Are Amazon, Square and Other Tech Companies Ripping Us Off? Housing. Unaffordable. What Works? Case studies and creative solutions. Don't Reach for Yield. Closed-End Funds. 2024 Investor IQ Test. Answers to the 2024 Investor IQ Test. Apple's Woes Drag Down the Dow. The Winners & Losers of 2023. Ozempic, Magnificent 7 & Beyond. 2024 Crystal Ball. The Underperforming DJIA, Full of Fossil Fuels and Forever Chemicals. A Spectacular Year for 3 of the Magnificent 7. The Best ROI* (Almost 40%!) & 7 Life Hacks That Save Thousands. Portugal Eliminates Tax Advantages for Ex-Pats. Holiday Gift Giving on any Budget. Including No Budget. Once in a Century Events are Happening Every Day. The Crypto Winter Enters Its 3rd Year. Earn $50,000 or More in Interest. Safely. Finally. Freebies and Deals for Black Friday and Cyber Monday. Auto Strikes End. EV Price Wars Continue. WeWork's Bankruptcy. Half-Empty Office Buildings. Problems in our Personal Wealth Plan. Solutions for Unaffordable Housing. Cruise Ships Give Freebies to Investors. Should You Take the Bait? Should You Take a Cruise? Bonds. Banks. The Treacherous Landscape of Keeping Our Money Safe. 7 Rules of Investing Air B N Bust? Barbie. Oppenheimer. Strikes. Streaming Wars. Netflix. Monero: A Token of Trust? 13 Lifestyle Choices to Reduce Waste, Pollution & CO2 & Save a Boatload of Dough. China Bans Apple 11-Point Green Checklist for Schools. Artificial Intelligence and Nvidia's Blockbuster Earnings Report Biotech in a Post-Pandemic World 10 Wealth Secrets of Billionaires and Royals. What Happened to Cannabis? Bank of America has $100 Billion in Bond Losses (on Paper) Lithium. Essential to EV Life. I'm Just Not Good at Investing. Investors Ask Natalie. Should I Buy an S&P500 Index Fund? Investors Ask Natalie. Bonds Lost More than Stocks in 2022. Do Cybersecurity Risks Create Investor Opportunities? I Lost $100,000. Investors Ask Natalie. Artificial Intelligence Report. Micron Banned in China. Intel Slashes Dividend. Buffett Loses $23 Billion. Branson's Virgin Orbit Declares Bankruptcy. Insurance Company Risks. Schwab Loses $41 Billion in Cash Deposits. Fiat. Crypto. Gold. BRICS. Real Estate. Alternative Investments. BRICS Currency. Will the Dollar Become Extinct? The Online Global Earth Gratitude Celebration 7 Green Life Hacks Fossil Fuels Touch Every Part of Our Lives Are There Any Safe, Green Banks? 7 Ways to Stash Your Cash Now. Lessons from the Silicon Valley Bank Failure. Which Countries Offer the Highest Yield for the Lowest Risk? Why We Are Underweighting Banks and the Financial Industry. 2023 Bond Strategy Emotions are Not Your Friend in Investing Bonds Lost -26%, Silver Held Strong. Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. .png) Taylor Swift at the 2023 MTV Video Music Awards. Photo by: iHeartRadioCA. Celebrity Jet CO2. Green Washing. The Facts. Taylor Swift: The Average American Would Have to Live 600 Years to Match Her CO2 Emissions of 2022. How bad are commercial flights and cruise ships? Taylor Swift is in a league of her own these days, and it’s not just for being the only artist to win Album of the Year four times at the Grammys (congratulations on this monumental achievement), or because her Eras Tour is the highest-grossing music tour ever – surpassing a billion dollars in revenue (extraordinary). She is also being called out as the top CO2 emitter of all celebrities with private planes*. The emissions from her flight from Japan to Super Bowl Sunday on Feb. 11, 2024 were an estimated 40 tons of CO2. Total emissions from Swift’s private plane in 2022 were 9,293 tons (source: DGB Group), placing her at the top of celebrity plane polluters, followed by Floyd Mayweather, Jay-Z, A-Rod, Blake Shelton, Steven Spielberg, Kim Kardashian, Mark Wahlberg, Oprah Winfrey and Travis Scott – many of whom flew into Vegas for the Super Bowl.  *Taylor Swift reportedly sold her Dassault Falcon 900 jet in January of 2024, after owning it since 2009. She allegedly purchases carbon offsets double the amount of her emissions. Offsets aren’t as effective as carbon drawdown and do nothing to actually remove the massive CO2 generated. Keep reading. Swift (and others) claim that their carbon credits offset their polluting ways. However, it’s quite important to note that the average American would have to live 600 years to contaminate the air as much as Taylor Swift did in just one year in 2022. It would take the average person living in France or the U.K. over 1,800 years to emit as much. (The U.S., Australia and Canada have 2-3 times the CO2 footprint of Europeans.)  So, how bad is flying coach, especially compared to driving? What about cruise ships? See below for a graph of CO2 by transportation. As you can see, SUVs are worse on the environment than flying coach. CO2 by Transportation  Private jets are in a horror league of their own, but cruise ships are terrible, as well. According to the Friends of the Earth analysis: One individual on a typical cruise ship emits roughly 421.43kg of CO² per day – more than double the emissions of most commercial flights. Alternatively, one individual staying in a high-end hotel, using carbon-heavy transportation and choosing higher carbon activities emits just 81.33 kg of CO² per day. The carbon footprint of an average land-based vacationer is around 51.88kg, less than one-eighth of the average cruisegoer. The lowest CO2 footprint is bike power. Followed by public transportation. In cities like Amsterdam, where bikes are everywhere, the denizens also enjoy greater health and far lower rates of obesity. Also, it bears repeating. Europeans often have a CO2 footprint of 5 or fewer tons per year per capita, while the Middle East, Australia, Canada, and the U.S. are 3X that. China is the biggest emitter by far, with 31% of the global CO2 emissions in 2020 (source: Union of Concerned Scientists).  The greatest threat to our survivability on this beautiful planet is thinking that someone else will save things, while we continue on with business as usual. Celebrities are not immune from the effects of climate change. If we make excuses to keep our status quo, nothing improves. Let’s thank the scientists and environmental organizations for helping us to know better. Once we know better, it’s time to make the change. We can be the change we wish to see, and challenge leaders and famous folks to be accountable, too. While government leaders and celebrities may face a security risk if they fly coach, there are still many ways to substantially lower their CO2. There’s a massive difference between all and nothing. Additionally, if they have the resources for a private plane, they have the money to drawdown their emissions (not just “offset”). Below are just a few ways that all of us, including celebrities, can rethink our transportation CO2 footprint. Since transportation is the biggest CO2 emitter, reducing our personal footprint would be a game changer. We can also make smarter food, housing, electricity and consumption choices as well.  Total U.S. Greenhouse Gas Emissions by Economic Sector in 2021. Source: EPA.gov Incidentally, green transportation is not just great for planetary health, but can also improve our physical and fiscal health. Did you know that most people spend more than $8000/annually on their personal vehicle, or that the dramatic rise in respiratory illnesses is directly linked to air pollution? Urban planner Brent Toderian consults with cities to eliminate congestion and reminds us that having too many cars on the road, even if they are electric, is an inefficient, gridlock transportation design. Making Smarter Transportation Choices: 6 Questions to Ask Ourselves Can I zoom instead of flying at least for the preparation stage of things? Can I plan my travel strategically, so I’m not zigzagging across the world? Is flying in a private plane necessary for my security, or am I using it as a party plane? Do I need a full-on bedroom in the sky, or will a cubby bed suffice? Can I downsize? Can the support team be incentivized to reduce their CO2 footprint? Instead of carbon offsets, should I invest in carbon drawdown, such as planting trees in a rainforest, donating to regenerative farming education, or sponsoring student gardens in public schools?