Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

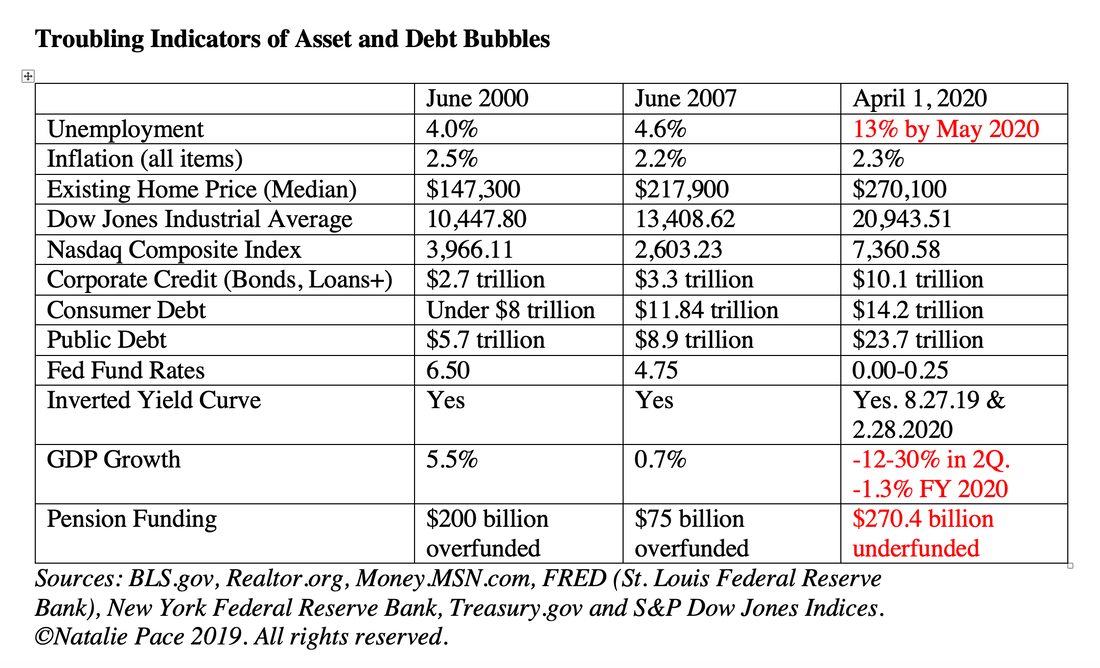

|

|

|

|

|

|

|

|