Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

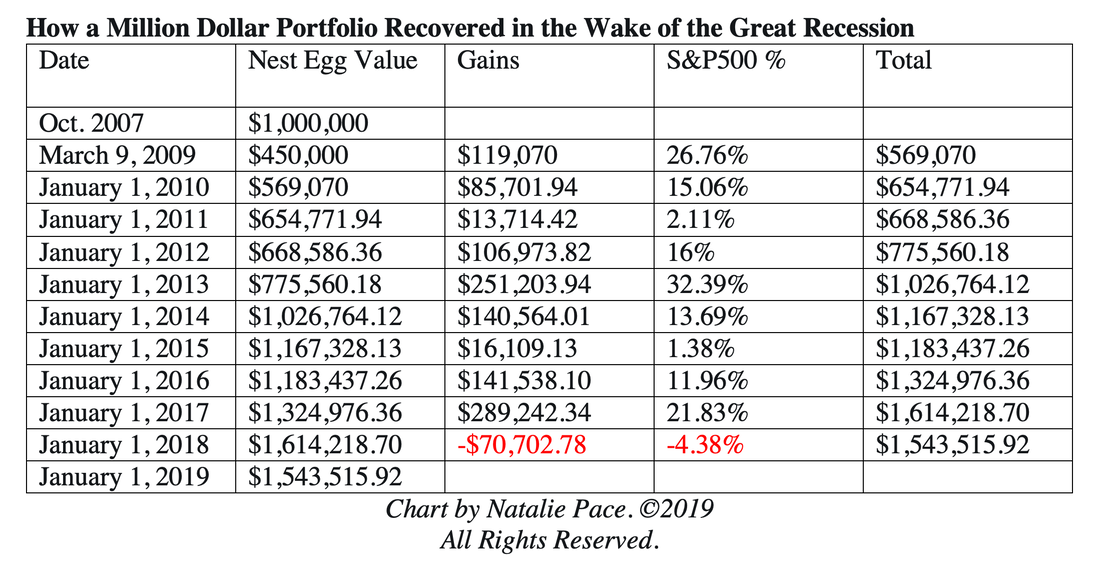

DJ Javy Union. Photo by Isabella Secus. (c) 2015. Wiki Commons. Used with permission. Dear Natalie, The Dow Jones Industrial Average return was 7.0% since January 2000 with dividends reinvested, or 197% total return. So, Buy and Hold did work. It was just gut-wrenching. Is there something that I’m missing here? I had a hard time with the markets for too many years which ultimately affected my current financial position. And although I understand "the markets" and the whole financial system way better now, I remain .... Gun Shy Dear Smart to Be Gun Shy, You can still ride a horse from LA to NYC. However, that doesn't mean that it "works." It's not just gut-wrenching when you lose more than half of your assets. It can wipe you out, prevent you from retiring, throw your credit score in the toilet, make you borrow at higher interest rates and affect your health. When someone loses more than half of their assets and retirement, this is not a math problem. It’s a life problem. I have seen far too many foreclosures, short sales, bankruptcies, deaths and even suicides to believe that you should buy into this very misleading statistic. When you lose 55% of your retirement (as the Dow Jones Industrial Average did during the Great Recession), it doesn’t recover at the same rate as the market. When you lose more than half, you are now earning gains on that much lower amount.  Between 2009 and 2018, the S&P500 rose to 2,506.35, from 903.25 (with a low of 676.53 on March 9, 2009). That equals a gain of 277% total, or 27.7% annualized over the 10-year period. This is just the gain of the market, not including dividends. However, the gain of your nest egg over that same 10-year period, including dividends, is still only 54.4%. That equals a gain of 5.44% annualized. Most of that decade would have been hell, and you’d be lucky to still own your own home. So, the annualized gain of the market does not come close to reflecting the real world. “Lies, damned lies and statistics,” Mark Twain. It took the NASDAQ Composite Index 15 years to crawl back to even. The Dow did fare better in that recession. However, as is human nature, there were a lot of people buying into the “New Economy” who were overweighted in Dot Com stocks. They watched in horror as the index lost 78% of its value between 2000 and 2000. Most Americans (and Canadians) have only slightly more money in retirement today using Buy & Hold than they did in 2000. Most of the increases would be contributions. On the other hand. If you were using my pie chart system, your losses could have been limited to 25% or less. On Dec. 24, 2007, I warned investors that the coming downturn was going to be nasty, and suggested overweighting 20% safe. So, the average 50 year-old would have had 30% at risk and would have lost about 17%. Again, many people were so horrified at the losses in 2009 that they sold low and went to cash at the bottom. No one who used my pie chart system was tempted to make that colossal mistake. In fact, our office received quite a large number of messages of gratitude. Click to watch Nilo Bolden's testimonial. What lies, damned lies and statistics are people buying into today? Actually, a lot of people are twice burned and wise. The real reason that the Dow Jones Industrial Average is trading so high is due to corporate buybacks. Companies can borrow money very cheaply, repurchase their own stock and make their earnings per share look stronger than it really is. It’s like bait in the water that the unsuspecting are supposed to snatch up. However, most of us live in the real world and we can see very clearly that no one in our circle of friends is better off financially today than they were twenty years ago. One other problem with Buy & Hold is that the closer you get to retirement, the less you are able to wait out a decade of hell. In theory, that is easily solved by keeping enough safe in bonds. However, there are many problems with that idea in today’s world. I’ve included just a few below. The Difficulty of Getting Safe in an Over-Leveraged World

The Bottom Line Buy and Hold worked just fine between 1970 and 2000. However, since 2000, we've had two recessions that look more like Great Depressions. The world is over-leveraged, drowning in debt, and using low interest rates to create asset bubbles. Buy and Hold does not work in a stagflation economy. Modern Portfolio Theory with Annual Rebalancing works great, provided you know what's safe in a world where stocks, bonds and real estate are all in bubbles. Getting your financial plan from a salesman is as bad an idea as…

Wisdom is the cure. It’s time to learn and master the ABCs of Money that we all should have received in high school. If you'd like to learn time-proven strategies that earned gains in the last two recessions and have outperformed the bull markets in between, join me at my Wild West Investor Educational Retreat this Oct. 19-21, 2019. Click on the flyer link below for additional information, including the 15+ things you'll learn and VIP testimonials. Call 310-430-2397 to learn more. Register by July 31, 2019 to receive the best price. I'm also offering an unbiased 2nd opinion on your current retirement plan. Call 310.430.2397 or email [email protected] for pricing and information.

Other Blogs of Interest Wall Street Secrets Your Broker Isn't Telling You. Unaffordability: The Unspoken Housing Crisis in America. Are You Being Pressured to Buy a Home or Stocks? What's Your Exit Strategy? Will the Feds Lower Interest Rates on June 19, 2019? Should You Buy Tesla at a 2 1/2 Year Low? It's Time To Do Your Annual Rebalancing. Cannabis Crashes. Should You Get High Again? Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth The Zoom IPO. 10 Rally Killers. Fix the Roof While the Sun is Shining. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. Tesla Delivery Data Disappoints. Stock Tanks. Why Did Wells Fargo's CEO Get the Boot? Earth Gratitude This Earth Day. Real Estate is Back to an All-Time High. Is the Spring Rally Over? The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What's Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed