Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

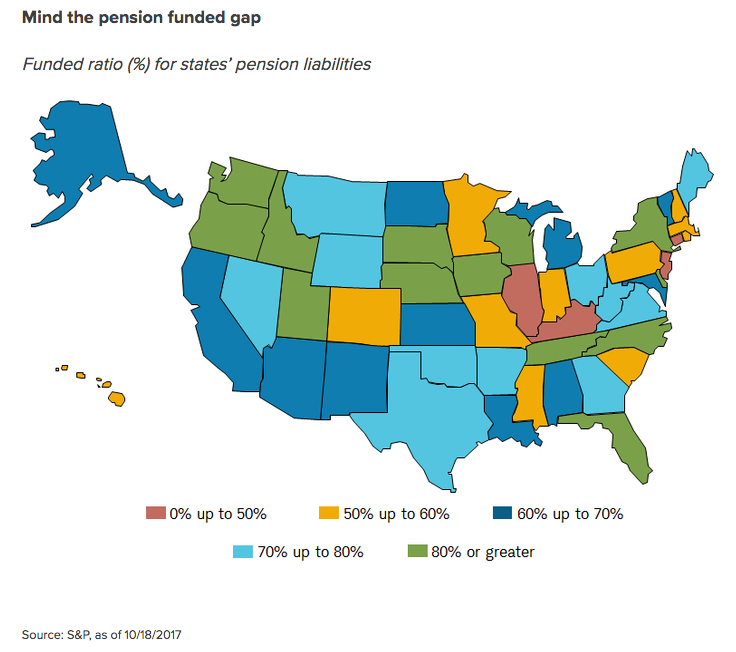

Kathy A. Jones, SVP, Chief Fixed Income Strategist, Charles Schwab Corporation. (c) 2018. Used with permission. On September 26th, 2018, the Federal Reserve Board increased the Fed Funds rate to 2-2 ¼ percent, and indicated that there will be another rate hike before the end of the year. Rates should move up to 3.1% in 2019 and 3.4% in 2020, according to the projections – a 70% increase from today. That’s great for savers, but not so fantastic for anyone holding bonds, as current bond values decline as interest rates rise. To compound matters, in January of this year, Alan Greenspan went on Bloomberg TV and said that bonds are in a bubble (stocks, too). It was a startling statement, however Warren Buffett has been bashing bonds for over a year now. Yet, most Americans own bonds in their retirement plans, whether they know it or not. So, how does one navigate the waters when the safe side of your portfolio – the “fixed income” bond side – could lose money? For answers, I turned to one of the leading bond specialists in the United States, Kathy A. Jones, the Chief Fixed Income Strategist for Charles Schwab Corporation, and a member of her team, Collin Martin. Ms. Jones loves diving into historical data, using her findings to inform her predictions for today. She quite famously and accurately predicted an extended period of very low interest rates back in 2010 – very early in this cycle. Now that interest rates have started to tick up, putting pressure on bonds, what should the Main Street investor do to protect herself? I asked Kathy that and more on Sept. 18, 2018. 9 Bond Tips for 2018 and Beyond. 1. Bond Ladders 2. Know What You Own 3. An Easy Way to Check Your Risk Level 4. Double Check Your Investment Grade Corporate Bonds 5. Underweight Your Exposure to High-Yield 6. Rebalance Quarterly or At Least Annually 7. Look Beyond the Name 8. Muni Maps. Avoid the Hot Spots! 9. The Duration Debate And here’s a little more color on each point. 9 Bond Tips for 2018 and Beyond. 1. Bond Ladders According to Ms. Jones, “Bond ladders are our favorite strategy. You can take advantage of rising yields to generate more income. That is going to offset the price change.“ A bond ladder is simply having bonds with staggered maturities and terms (10 years or less) that you roll into something new at maturity. If you are adding in a new bond each year, as interest rates are rising, then you’ll be capitalizing on higher yields. 2. Know What You Own It’s important for you to be the boss of your money, even if you have a financial planner. Ms. Jones encourages all of us to “know what you own, why you own it and how it might perform given a certain outlook.” Don’t assume that you’re safe. Make sure that you are not over-exposed to high-yield, highly leveraged, or risky bonds, which can become more vulnerable as credit tightens and money becomes more expensive to access. 3. An Easy Way to Check Your Risk Level You might think that getting a Ph.D. in economics would be easier than analyzing your retirement plan. However, Kathy Jones has a simple formula. “If the risk-free rate is 2%, and your fund is offering you 5%, you’re taking on some sort of risk.” Investors tend to think that everything is fine when they are getting a great yield – until something terrible happens, as happened with General Electric last year, when the company slashed its dividend in half and then saw its stock drop by half. 4. Double Check Your Investment Grade Corporate Bonds Corporate bonds are attractive to investors because in a world where Treasury bills are only offering 2%, some investment grade bonds, like Ford Motor Company, are paying 5% or higher. However, as Collin Martin pointed out in our interview, there is over $9 trillion in corporate debt and leveraged loans outstanding in U.S. corporations (public and private). Over half of the investment grade corporations are rated BBB, just one notch above speculative (more commonly called “junk” bonds). “Check to be sure that any bond fund you have has a higher allocation to A or higher rated bonds, and a lower allocation to BBB,” Collin Martin suggested, adding that it’s a good idea to “focus on higher quality.” 5. Underweight Your Exposure to High-Yield Not all bonds and bond funds are created equal! If you see the words “high-yield” or are getting above 4% dividend, you could be taking on more risk than you realize. High-yield bonds can lose money and become illiquid. In the worst-case scenario, the company might have to restructure their debt, as happened with Greek bonds in 2011 and General Motors bonds in 2009. So Ms. Jones and Mr. Martin suggest that you make sure your exposure to high-yield is appropriate to your risk tolerance and financial plan, and limited to a smaller portion of your portfolio. 6. Rebalance Quarterly or At Least Annually This simple nest egg strategy is as close as you can get to buying low and selling high, according to Kathy Jones. If you simply rebalance once or more a year, then you are capturing gains when an industry gets hot, and buying low when prices drop. 7. Look Beyond the Name Many very risky funds have alluring names, like BulletShares, to entice unsuspecting shareholders into a risky investment. Others just make it harder to find out that the holdings are risky. So, be sure to check the holdings and portfolio page of your fund to be sure that your “Income” producing bond fund isn’t stacked with below investment grade corporate bonds. Knowing what you own takes just a few clicks, if you know where to look. 8. Muni Maps. Avoid the Hot Spots! Kathy Jones and her team publish a map of states that are in trouble, making it easier for the Main Street investor to avoid the hot spots, like Illinois, Connecticut, New Jersey, Kentucky, and also cities, like Chicago. According to Ms. Jones, “The pension funding issue is the big one that everyone is concerned about.” While the state GO bonds could get downgraded in the most vulnerable areas, there are revenue bonds, even in troubled states, that Ms. Jones believes would be a “better bet, if you have confidence in the revenue stream, like water, sewer and the essential services.”  Map compiled by Charles Schwab Corporation. (c) 2018. Used with permission. 9. The Duration Debate Should you own a long-term bond? According to Collin Martin, not yet. Ms. Jones and Mr. Martin are still advising that long-term bonds are make up only a small percentage of your portfolio. The Bottom Line? In a world that is riskier than you might know and more leveraged than ever, your personal plan doesn’t have to be. Knowing what you own, and employing these 9 tips should help you to get safer and more diversified, while capitalizing on a plan that can capture higher yields as interest rates rise. If want to be sure that your current plan doesn't have any hidden time bombs and money pits, schedule an unbiased second opinion with me now. Call 310-430-2397 to learn more. About Kathy A. Jones Kathy A. Jones is responsible for credit-market and interest-rate analysis, as well as fixed income education for investors at Schwab.

Important Disclaimers

Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the U.S. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies.Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed