Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

Flooding in Houston, Texas from Hurricane Harvey is said to be "unprecedented" by the National Weather Service. If you are interested in helping out Houston and the Gulf Coast during Harvey’s flooding and deluge, below is a list of nonprofit organizations offering on the ground emergency services and post-storm recovery. Click on the name to access the organization's website and donation page.

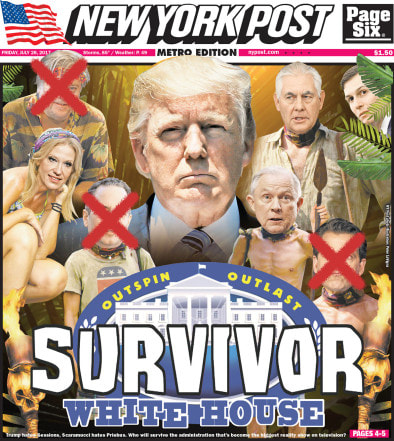

All Hands Volunteers has already mobilized a response team for on the ground support. The American Red Cross has shelters, supplies and volunteers in place to assist people affected by Hurricane Harvey. Habitat for Humanity has been involved with disaster recovery and home building for those in need since 1976. The Texas Diaper Bank has been helping underserved communities since 1997. Diapers (for babies and elders) are not provided by disaster relief agencies, according to the organization. Designate that you want your donation to go to Disaster Relief for Hurricane Harvey. United Way Houston: If you or someone you know needs help in the Houston area, dial 2-1-1, the Texas/United Way Help Line. This 24/7 call center offers shelter, food, prescriptions and more. Donate to the Houston United Way here. The United Way Relief Fund assists with storm-related needs and recovery. Be wary of any organization that you are not familiar with by name. There will be a few sham shysters capitalizing on your care and concern, without any intention of helping those in need. If you aren’t sure about who runs the organization or how long it has been around, just move on to an organization that you are sure about. Your donations to a qualified 501(c)3 are tax deductible. Be sure to write down the 501(c)3 number for your accountant. Please feel free to list your favorite organization in the comments below. If you notice a scam, please alert all of us in the comments below as well. “The only time in history going back to 1881 when [CAPE] has been higher are, A: 1929 and B: 2000. We are at a high level, and its concerning. People should be cautious now.” Robert Shiller, Nobel Prize winning economist and Yale professor of economics Last week was a historic week. The White House was under fire after a deadly protest in Charlottesville. The fallout included another White House official being voted off the island Survivor-style, with the unceremonious ousting of Stephen Bannon. A CEO exodus from the White House business advisory councils forced the 45th President to disband them. With that kind of upheaval in the central government, as one might expect, the U.S. stock market took its second straight week of losses. As of today’s close, the Dow Jones Industrial Average was at 21,703.75, trading down 2% from its August 7, 2017 high.  The New York Post poster: Survivor: White House. (Click to view the article.) Investors were looking for signs of stability from the central government. However, the real reason for the losses was fundamental economics, not politics. In fact, after the ousting of Bannon, the markets applauded only briefly, and then headed south again as news of an earnings miss by Foot Locker made the rounds. Foot Locker sales declined 4.4%. Net income was off 60% year over year, as the company was hit with a $50 million pre-tax litigation charge relating to its handling of a pension plan conversion in 1996. Incidentally, S&P 500 companies are underfunded on their pension and Other Post Employment Benefit obligations by over half a trillion currently. Only 4.52% are fully funded on their pensions and OPEBs, with OPEBs (like health insurance) the furthest behind. “If OPEB were a patient, it’s status would be critical,” according to Howard Silverblatt, the senior index analyst S&P Dow Jones Indices. Foot Locker isn’t the only retailer suffering. There has been a wave of bankruptcies in retail, with over half liquidating completely, rather than just restructuring debt. Malls across America are like expensive ghost towns, with no one, save the salesmen, inside the well-appointed and overstocked stores. Marketing firms say that Millennials prefer experiences to shopping. However, that’s a convenient simplification of what’s really happening. Many Millennials are strangled with college debt, working multiple jobs and still not able to make ends meet. Shopping is a luxury many simply cannot afford. The Middle Class has been squeezed out of its comfort zone. Home prices are higher than they have ever been. Consumer debt is higher than it has ever been. "Flows of credit card balances into both early and serious delinquencies climbed for the third straight quarter—a trend not seen since 2009," according to the Federal Reserve Bank of New York. Wages have stagnated. The “Gig” Economy has many people trying to piece together a living with multiple part-time jobs. Health care costs are out of reach and unsustainable. (There are ways to personally put yourself in the best position during these hard times. Click to learn more about my Investor Educational Retreat this October, if you want to save thousands of dollars every year in your annual budget, protect your retirement plan from the next crash, live a richer life and have more money for retail and bucket list vacations. It’s less time and less money than you are currently spending, with solutions that will last a lifetime.) With 69% of the GDP growth reliant upon the American consumer, and the Middle Class being squeezed, can the American Consumer continue to carry this economy? The Stock Market and Earnings According to Robert Shiller, Nobel Prize winning economist and Yale professor of economics, “The CAPE ratio that John Campbell and I devised 30 years ago is at unusual highs. The only time in history going back to 1881 when it has been higher are, A: 1929 and B: 2000. We are at a high level, and its concerning. People should be cautious now.” 1929 marked the beginning of the Great Recession; 2000 was the market high before the Dot Com Recession. Click to hear Professor Shiller discuss this in greater detail on CNBC. Essentially, the CAPE ratio takes a look at 10-years of earnings when calculating the price to earnings ratio because earnings fluctuate wildly year-to-year. By either the CAPE or the annual average Price to Earnings ratio, the current PE ratio is high. Interestingly, the PE ratios are high even though corporations have done massive buying and retiring of stock – which reduces the PE. NASDAQ dropped 78% between its highs in March of 2000 and its lows of October 2002.  Chart by Finance.Google.com. (c) Google. Used with permission. The Dow Jones Industrial Average lost 55%, sinking to a low of 6547 on March 9, 2009.  Chart by Finance.Google.com. (c) Google. Used with permission. Is this the new normal? 8-year bull markets followed by colossal implosions? It’s entirely possible, particularly as long as the Middle Class is being squeezed out of profits and strangled with debt, while being expected to continue to buy buy buy and fuel earnings. As I’ve pointed out repeatedly, and as Robert Shiller stresses in his video interview with CNBC, market timing doesn’t work. PE ratios were high for a couple of years in the late 1990s before the Dot Com Crash. Also, if you move all into cash, then it’s very difficult to know when to move back in. If you did that just before two years of solid gains, then you’ll rue your actions and want to jump back in even if the prices are high and unsustainable. Overweighting safe, diversifying and annual rebalancing work great. Getting safe in today’s climate is tricky. There are lots of “safe” assets that are losing money, and other “safe” products that have recently adopted redemption gates and liquidity fees. You can’t rely on Buy and Forget About It or any of the old investment adages. Wisdom is the cure. Get the ABCs of Money so that you can be the Boss of Your Money. This has never been more important than now. The last time the U.S. was in this position, in terms of consumer debt and squeeze, it resulted in the Great Recession and a meltdown of the U.S. banking system. The Federal Reserve and taxpayers have already bailed out the banks. U.S. corporations have more cash than many countries – particularly Silicon Valley companies like Apple, Google, Microsoft and Oracle. Corporate buybacks have largely fueled the current bull market. When economists talk about a sustained rally, they often point to buybacks and the amount of cash being held in corporations. However, corporate cash can’t jumpstart personal consumption, when so many Americans have more debt than savings or retirement. Lower spending means lower sales and missed earnings. Financial engineering, like corporate buybacks, can only work for so long. Declining sales has already slain countless retail companies. What industry is vulnerable next? If Nobel Prize winning economist Robert Shiller is right about the CAPE ratio indicators, it could be all of them. Don’t get scared. Get smart. Call 310-430-2397 to learn more now. Below are other Warning Signs in the Economy, which I outlined in greater detail in my BlogTalkRadio show this month. Click to listen to that show.  Red Flags/Concerns

Bright Spots in the Economy

More Blogs With Additional Information and Data What is the Smart Money Doing? http://www.nataliepace.com/blog/what-is-the-smart-money-doing Are You Gambling With Your Future? http://www.nataliepace.com/blog/are-you-gambling-with-your-future Will Congress Raise the Debt Ceiling in Time? http://www.nataliepace.com/blog/will-congress-raise-the-debt-ceiling-before-august Social Security is Cash Negative, at 28% of the Public Debt and Growing http://www.nataliepace.com/blog/social-security-is-cash-negative-at-28-of-the-public-debt Minutes of the July 25-26, 2017 FOMC Meeting https://www.federalreserve.gov/monetarypolicy/fomcminutes20170726.htm Economic Projections from the June 2017 FOMC Meeting https://www.federalreserve.gov/monetarypolicy/fomcminutes20170614ep.htm PCE % of GDP Charts https://fred.stlouisfed.org/series/DPCERE1Q156NBEA Consumer Debt https://www.newyorkfed.org/microeconomics/hhdc.html  Thank You. In August 2000, a broker salesman attempted to take all of my hard-earned gains from a real estate sale, saying he would diversify and protect me, by investing in Enron, Global Crossing and AOL funds. I had 1000 sound reasons why all of those investments were a bad idea at the time, but I didn’t (then) have the confidence and wisdom to know definitively that I was right. If I had placed my trust and money with the salesman, I would've lost everything. I don't know as a single mother how I could've survived that.  Yours truly (Natalie Wynne Pace) with my young son son. It was then that I became determined to expose the conflict of interest that is inherent in much of the financial services industry, so that others could be saved, too. I developed simple, easy investing solutions that cost less time and money than having blind faith in a “financial planner” who often makes more commission when they sell you things that you don’t need. I also developed the Thrive Budget, which allows you to stop making the billionaire corporations rich at your own expense, which allows you to live a much richer life, have more bucket list vacations and provide far better for your future. I love my job. I love hearing the stories of people who earn gains when the economy and markets lose more than half. (Yes, we have those testimonials.) Or retired couples who downsize to a sustainable lifestyle, and are able to live a richer life in retirement as a result. Or college students who get a far better degree for half the cost of their colleagues, and exit college capable of finding a job without the crushing debt. There are people who complain about their problems, and there are those who can see beyond their problems, or at least have faith that there is a life beyond what crushes their spirit now. Having a vision of where you'd like to go and a plan to get there will always work better than throwing your hands up in the air and complaining that you have no control. Complaining and doing nothing are choices, too. However, none of this happens without you. The status quo has more money, more advertising and thus a larger reach than I do. It is your 5-star reviews, your passionate support, your shares, your likes and your questions that enable me to save another down the road. And for that, I thank you. All of my hottest tips, and most important alerts, from Bitcoin fraudsters to penny pot stock scams, from picking Tesla and Google at their product launches, all come from questions posed by people, like you, who follow my work. Money is a very personal topic, and that’s why we offer a number of ways that you can get your questions answered anonymously. Below are just a few ways you can do just that. There are solutions for your challenges. They just aren’t found in the mainstream. Otherwise, your problem would already be solved.  I wanted to take a moment to thank you for joining my mailing list, my Facebook page, Twitter, Instagram, YouTube, Medium, Blog, BlogTalkRadio, etc. If you are having difficulty making ends meet (who isn’t), if you’ve been approached with a surefire investment opportunity with promises of astronomical 100% guaranteed gains, or if you’re interested in a second opinion on the way your money is being managed, then it’s a very good idea to reach out for wisdom and a second opinion. Call 310-430-2397 or email info @ Nataliepace.com to reach my office directly.

Thank you for joining my mailing list, my Facebook page, Twitter, Instagram, YouTube, Medium, Blog, BlogTalkRadio, etc. Stay in touch. Ask your questions. Get your answers. Share hot opportunities (that you want me to check up on). Have a wonderful summer. Now is the time to make sure that the plan and path that you are on is a good one. I’m here to help. I love empowering Main Street with the easy systems needed to thrive in today’s volatile economy. It is an honor, and a job that I cherish and take very seriously – since 2000!

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed