Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

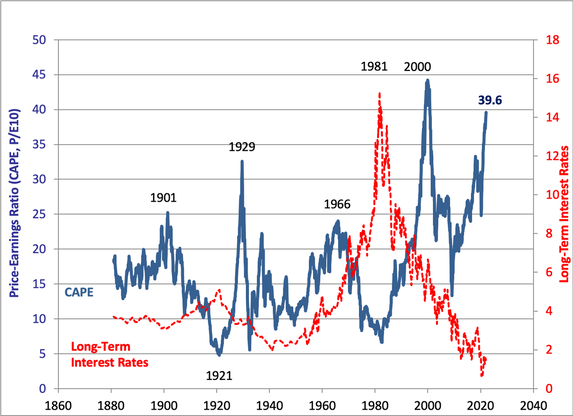

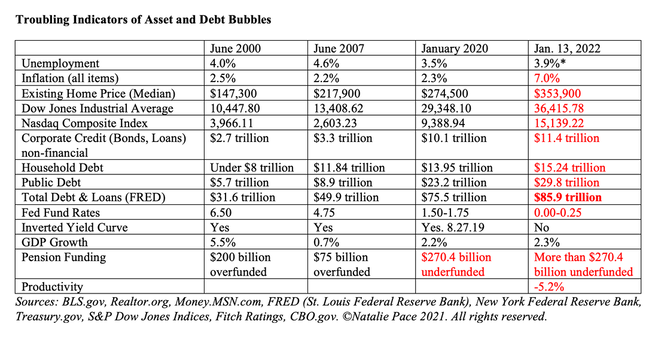

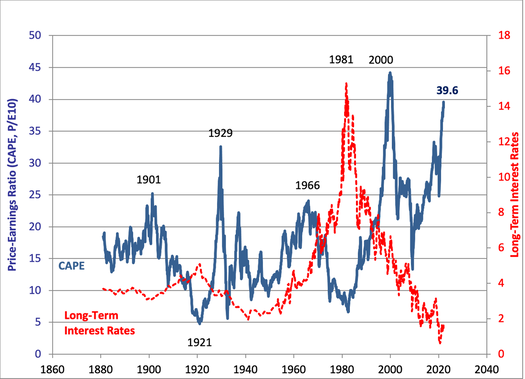

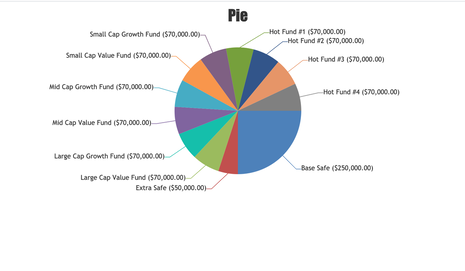

The NASDAQ Composite Index was down -15.1% from its 52-week-high (set on Nov. 19, 2021) and -12% since Jan. 1, 2022, as of Friday, Jan. 21, 2022. The S&P500 sank -10.7% on the year today (Jan. 24, 2022). Is this the beginning of another plunge a la Feb. 19-March 23, 2020 (-38% in the S&P500), or Oct. 2007-Oct. 2009 (-55% in the Dow Jones Industrial Average), or March 2000-October 2002 (-78% in the NASDAQ Composite)? What’s your best plan? Will stocks recover or continue to sink? Stocks in 2022: Churn As Liz Ann Sonders, the Chief Investment Strategist at Charles Schwab, told me in an interview on Thursday, the current weakness in the indexes is something that has been happening under the surface all last year on the individual company level. More than 90% of the NASDAQ Composite Index endured a correction of at least 10% in 2021, and almost half lost 50%. Of course, that’s an average. Some stocks had far wilder gyrations, while others were in a more limited range. The smaller the company, the more likely it was to experience rapid-fire, extreme volatility. Who’s Doing the Selling? According to Howard Silverblatt, the Senior Index Analyst of the S&P 500®, it appears that the selling is institutional. That means the big money is making the move. That is often the case early in a correction. It was institutional money that initiated all the selling that happened between February 19 and March 23 of 2020. The real question now is… Will Stocks Recover or Continue to Sink? There’s a lot of pressure on stocks these days. Equities are very overvalued. You can look at Professor Robert Shiller’s CAPE ratio below, or link to the Buffett Indicator in Liz Ann Sonders’ Market Outlook from Nov. 29, 2021.  CAPE Ratio Jan. 24, 2022. Source and (c): Professor Robert Shiller. Yale.edu. Used with permission. According to the Federal Reserve Financial Stability Report, when asset prices become elevated (as they are today), the correction can be swift and severe, and other financial risks become elevated. On Nov. 8, 2021, the report warned: Elevated valuation pressures tend to be associated with excessive borrowing by businesses and households because both borrowers and lenders are more willing to accept higher degrees of risk and leverage when asset prices are appreciating rapidly. The associated debt and leverage, in turn, make the risk of outsized declines in asset prices more likely and more damaging. What other headwinds are on stocks? Rising interest rates will slow the economy, as will the sunset of government programs. Inflation can be negative for stocks. The University of Michigan consumer sentiment survey indicates that the high prices of homes, cars and other consumer goods has tanked buyer intentions. With almost 70% of GDP linked to consumer spending, GDP will slow. It is predicted to still be relatively strong, at 4.0% in the U.S. (and 4.8% in China). However, the outlook might change if the headwinds get stronger. In fact, another way to look at the institutional selling could be a signal to Washington and the Feds that the economy and the consumer still need more support. What Could Help Stocks to Rise Again? The Federal Reserve Board has certainly been a friend to the stock market under Jerome Powell. However, the last meeting minutes indicated that the FOMC members were committed to stopping their purchase of assets, to rolling down their massive $8.9 trillion balance sheet and to raising interest rates. Interest rates are expected to climb to almost 1% this year and 1.75% by 2023. When money gets tighter, Wall Street gains are muted. It’s rare for a recession to occur in the first year of the tightening. Of course, with so much leverage and debt in the world and the elevated asset prices (on average, not on all stocks), there is always a more heightened risk of that “outsized decline.” In my Crystal Ball videoconference from last Thursday, I warned that there are many indicators that 2022 would be in the low single-digits for gains – far from the 26.6% S&P500 scorecard of 2021. The Feds are keenly aware of their influence on stock market movements. So, the Jan. 25-26, 2022 FOMC meeting will be a lively discussion. Inflation is forcing their hand to raise interest rates. Having too much on the balance sheet has definitely got them interested in reducing that. We’ll see whether or not the January plunge of stocks will inspire them to stay on course with their deleveraging and interest rate hikes, or offer language and a slower trajectory that calms the markets. If they decide to slow down their action to settle stocks, it may well do so. If they stay on course, it’s possible that the Taper Tantrum will continue. So, there will be a lot riding on the press release that comes out at 2 PM ET this Wednesday. Corporate Buybacks The large corporations have a lot of cash. 2021 set records for corporate buybacks, with about $850 billion of stock repurchased. Apple alone repurchased $92.5 billion of their own stock over the 12-month period (3Q 2021 – 3Q 2022). Corporate buybacks are a driver of market gains. According to Howard Silverblatt, corporations are expected to continue their buybacks in 2022. Speaking of buybacks, the last major downturn (outside of the pandemic recession between Feb. and March of 2020) in Dec. of 2018 had a lot to do with Apple stopping their repurchase plan that December. The company dropped from an average $20 billion a quarter in purchases to $10.1 billion for the 4th quarter in 2018, with almost no purchases in December. That resulted in the worst December on Wall Street since the Great Depression. 2019 then went on to rack up 28.9% gains, with Apple back on track for their quarterly $20 billion repurchases. There has been a high correlation between Apple’s purchases and general index performance over the last few years. Churn In 2021, we saw a substantial amount of churn. Moderna, with outstanding sales growth of over 3000% in the 3rd quarter of 2021, rocketed from $150/share to almost $500/share and then dropped back down to $160. Tilray is trading at $5.60 but soared to $67 in February 2021. The volatility has been more prevalent in smaller companies than larger companies, with micro caps suffering the most. Hedge funds and hot money adore volatility. If you’re going to own individual companies, particularly if they are in the small or midcap range, you have to babysit them. If you get lucky enough to shoot the moon, you have to have a strategy for taking your profits swiftly. Liz Ann Sonders phrase, “Add low, trim high” is applicable for a company you believe in that is experiencing extreme volatility (and also in your nest egg strategy). It doesn’t have to be all or nothing. Market timing just doesn’t work. What’s Your Best Plan? Early in 2021, when it was clear the year would be on fire, we took off the overweight safe on our pie charts, which had been in place in early 2019 (before the pandemic). With all of the volatility and market headwinds, it’s a good idea to overweight safe again in 2022. See below for what a 30-year-old overweighting 10% and 20% safe, with proper diversification, would look like.   What does overweighting safe mean? You should always start your plan by keeping a percentage equal to your age out of stocks, and in a place that won’t lose principal. It’s very important to know what is safe in a Debt World. That’s tricky. Because in your retirement plan, if you overweight safe you might be in a money market fund. Money market funds can lose value. They have redemption gates and liquidity fees. They are not federally insured. Bonds are illiquid, highly leveraged and negative-yielding. Your best plan is knowing how to properly diversify and how to get as safe as you possibly can in a world where that is difficult. By 2023, yields may be high enough that you can take on a midterm creditworthy bond that pays you a nice dividend of at least 5% or 6%. If you try to get a 5%-6% yield in today’s world, you have to go into junk bond territory, where your principal is at risk. You can read about our time-proven 21st-century strategies in The ABCs of Money, or you can learn and implement this time-proven plan by attending our February 11-13, 2022 Financial Empowerment Retreat. A small investment of time and money could save your nest egg! These time-proven 21st Century strategies earned gains in the Dot Com and Great Recessions, and outperformed the bull markets in between. Call 310-430-2397 or email [email protected] to learn more now. You can also click on the banner ad below to get testimonials, to learn the 15 things you’ll learn at the retreat, and to get pricing and hours information. It’s going to be conducted online, so it feels like it’s you and I talking directly in your living room. It’s a great way to learn, and you have no travel or lodging expenses.  Join us for our New Year New You Financial Empowerment Retreat. Feb. 11-13, 2022. Email [email protected] to learn more. Register with a friend or family member to receive the best price. Click for testimonials & details. Other Blogs of Interest Investor IQ Test Investor IQ Test Answers Real Estate Risks. What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Investor IQ Test 2021. Investor IQ Test Answers 2021 Crystal Ball. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  About Natalie Pace

Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden.

2022 Investor IQ Test Are you an Einstein in investing? A complete novice? Check your Investor IQ with the 26 questions below. If you score 21 correct answers or higher, then you’re in great shape! If you score 18, then you are C-level. Below 18 correct indicates that you are in need of a refresher course in life math. (Even math geniuses might not know the basics of Wall Street…) So, consider joining us at our next Investor Educational Retreat.

Answers are listed in the article "Investor IQ Test Answers 2022" in my blog at NataliePace.com. https://www.nataliepace.com/blog/ Email info @ NataliePace.com or call 310-430-2397 if you have any questions about this test, or about the answers, or if you are interested in learning time-proven investing, budgeting, debt reduction, home buying solutions that will transform your life.  Join us for our New Year New You Financial Empowerment Retreat. Feb. 11-13, 2022. Email [email protected] to learn more. Register with a friend or family member to receive the best price. Click for testimonials & details. Other Blogs of Interest Investor IQ Test Answers Real Estate Risks. What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Investor IQ Test 2021. Investor IQ Test Answers 2021 Crystal Ball. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  About Natalie Pace

Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden.

Answers to the 2022 Investor IQ Test. by Natalie Pace. If you score 21 correct answers or higher, then you’re in great fiscal shape! If you score 18, then you are C-level. Below 18 correct indicates that you are in need of a refresher course in life math. We’ve hosted attendees with a Ph.D. in math or computer science, with MBAs, options traders and other Wall Street pros. Our strategies are enthusiastically recommended by Nobel Prize-winning economist Gary Becker, former TD AMERITRADE chairman and CEO Joe Moglia and thousands of Main Street investors. So, consider joining us at our next Investor Educational Retreat. 1. What is the most important question you should ask your Certified Financial Advisor before hiring him/her? "How much of my portfolio should I keep safe?" This question will help you to determine whether you are dealing with a trusted professional who is looking after your best interest, or a salesman who is looking to make a quick buck. The answer to this question is, "A percentage equal to your age.” As stocks are trading at elevated prices and bonds are illiquid and negative-yielding, it would be even better if s/he adds, “But given the valuation and leverage concerns, we might consider overweighting more safe." If they just sidestep this question and redirect you to a risk tolerance questionnaire, that is a red flag. One more important thing. Since bonds are highly leveraged, subject to credit risk, vulnerable to capital loss and are illiquid to boot, you need to understand what’s safe, rather than just rely upon bonds or money market funds. Now is the time to clearly know exactly what you own and why. Consider getting an unbiased 2nd opinion. Call 310-430-2397 or email [email protected] for pricing and details. 2. What are 3 red flags that your financial plan is on a Wall Street rollercoaster and at risk of losing half or more of its value?

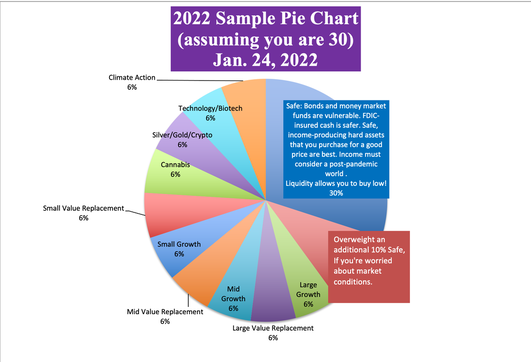

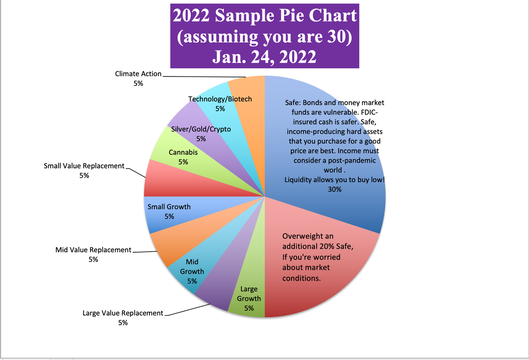

Remember: Your nest egg recovered in the pandemic because the Treasury printed up $5.4 trillion and threw free, easy cash at everyone. Student loans, foreclosures and evictions were paused. The wind has been at our backs. 2022 will be slower and more challenging than 2021. When/if the tides turn, losses can incur quite swiftly due to the high valuations. (The 38% plunge between February 19, 2020 and March 23, 2020 was the fastest that any bull market had ever about-faced into a bear.) Wisdom and time-proven systems are the cure. (Our easy-as-a-pie-chart nest egg strategies, with annual rebalancing, earned gains in the Dot Com and Great Recessions and have outperformed the bull markets in between.) 3. How much of your nest egg should you keep safe? A percentage equal to your age. Consider overweighting more safe when assets are overpriced, the economy is stumbling, a pandemic is closing borders or you are nervous. Again, in today’s Debt World, it is important to know what’s safe. Bonds are losing money and are illiquid, which makes them substantially riskier than most investors realize. (Our safe side isn’t supposed to lose money!) Money market funds have redemption gates and liquidity fees, are vulnerable to capital loss and are not FDIC-insured. Annuities are more vulnerable than most investors know because insurance companies are carrying a lot of risk and leverage, and annuities are not federally insured. 4. What's safe? Getting safe is a two-step process. First, you must keep your money, which means that you want to have as much of your cash as you can in federally insured accounts, such as FDIC or CDIC. Liquidity allows you to buy low, when everyone else is cash-strapped. Hard assets will hold their value better than paper assets in a Debt World. So, the mantra is “safe, income-producing hard assets that you purchase for a good price.” You have to also consider what will safely produce income in a post-pandemic world. Real estate is at an all-time high in the U.S., so it will be difficult to purchase for a good price in 2022. You don’t want to be all in on hard assets because you also need liquidity and cash flow. That is why some of the best hard asset investments are those that reduce your monthly expenses (for life). We spend one full day on What’s Safe at the Investor Educational Retreats. Educate yourself now on the best income-producing hard assets that are right for you, so that when prices are more attractive, you know what you want and have the means to take action and close the deal. Call 310-430-2397 to learn more. Interest rates will rise in 2022 and 2023, so there will come a time when you can get a creditworthy mid-term bond that pays you for the risk you take on. In the meantime, if you’re sold into something it could lose money and also carry an opportunity cost by tying your money up. 5. What is the average return of stocks over the last 10 and 30 years? Large cap stocks earned 16.55% annualized over the last decade and 10.65% over the 30-year period (source: Morningstar). Small cap stocks performed at 13.69% and 12.05%, respectively. (Asset performance graphs, and more data and resources, are distributed to Retreat Attendees.) 6. What is the average return of gold over the last 10 and 30 years? Gold returned 0.68% annualized over the 10-year period and 5.31% over the last 30 years. Gold mining stocks doubled in 2016, were flat in 2017 and were worth almost double their 2018 lows by Jan. 17, 2022. The all-time high for gold of $2,089.20 was hit on January 5, 2021. The last high of $1,895/ounce in gold occurred in September of 2011, the month after S&P Global Ratings stripped the U.S. of its AAA credit score. Fitch Ratings currently has the U.S. on a negative outlook, meaning the AAA rating from Fitch could be downgraded this year. (Moody’s still has a stable outlook for the U.S. AAA, as of Dec. 1, 2021.) 7. What is the average return of real estate over the last 10 and 30 years? Over the last decade, real estate has performed at 9.6% annualized. (The devastating losses of the Great Recession are no longer included in this statistic.) Over a 30-year period, real estate increased 8.0% annualized. Real estate prices are at an all-time high. However, the trend has been down since October. Real estate is largely unaffordable to many Americans. According to AttomData, average income-earners are unable to purchase in their community in 77% of U.S. counties. Rising interest rates will make this problem even more pronounced. 1.9 million U.S. homes are still underwater – even with prices higher than ever. (This is largely due to loan mods.) There is nothing worse than buying high in real estate, and watching the value of your home sink below the amount that you owe on it! It can ruin your life and FICO score for years, if not decades. Be sure to read the Real Estate section of the 5th edition of The ABCs of Money. There are at least seven real-world case studies to inform your real estate decisions. 8. What was the top performing investment in 2021? Bitcoin gained 57% in 2021. Oil came in second, with gains of 55%. The NASDAQ Composite Index scored 21.4% gains, with real estate soaring 14.45%. Oil prices were the biggest losers of 2020. In April of 2020, oil prices went negative, for an all-time low price of -$37.63/barrel. (Futures investors were paying not to take delivery!) Bonds performed poorly as well, with negative yields and illiquidity issues. The total bond fund return was -3.3%. (Again, the safe side of your nest egg is not supposed to lose money.) 9. How long will it take for you to have a nest egg as big as your annual salary if you put 10% of your income into a tax-protected (and financial predator proof) individual retirement plan and invest in stocks and bonds*? 7 ½ years. This is based upon 10% average annualized returns of stocks and bonds over a 30-year period, which is about what those assets did between 1992-2021. 10. How long will it take for your nest egg to earn more than you earn, if you put 10% of your income into a tax-protected (and financial predator proof) individual retirement plan and invest in stocks and bonds*? 25 years. This is based upon 10% average annualized returns of stocks and bonds over a 30-year period, which is about what those assets did between 1992-2021. 11. What’s the safest investment in a slow-growth, high-debt world? Hard assets hold their value better than paper assets when there is too much paper floating around. However, pouring everything into real estate can be vulnerable, as you still need liquidity. It’s not a good idea to just put everything into cash and real estate. So, learn how to diversify properly (you don’t need 18-pages of holdings), avoid the Bailouts, add in hot industries, keep enough safe, overweight safe in volatile times and rebalance 1-3 times a year. Market timing doesn’t work. This may sound complicated, but it is actually easy-as-a-pie-chart, once you learn our strategies. Most, but not all, hard assets are overpriced right now. If you are equity-rich, you still want to do the analysis to make sure that will remain the case if real estate asset prices decline significantly in value, as they did in the Great Recession. Be sure to read the Real Estate section of the 5th edition of The ABCs of Money. There are some excellent safe, income-producing, value-priced hard assets that are worth considering now, which is why we spend one full day on What’s Safe at the Investor Education Retreats. Think capital preservation. Liquidity will allow you to buy low when things are on sale. In other words, don’t be suckered into a risky investment with the idea that you are earning nothing on the safe side. You have to take on a lot of risk to earn anything when interest rates are at zero – which isn’t safe. 12. Which countries hold the most gold? The United States is the top holder of gold worldwide, by far, with 8,133.5 tons, followed by All ETFs, Germany, the International Monetary Fund, Italy, France, Russia and China. China and Russia have been on a gold buying spree since 2008. Reports are that they are trading oil and other commodities using their own currency backed by gold, in an effort to break free from the dollar hegemony. Additionally, there were multiple reports between 2011 and 2017 that the U.S. banks and brokerages were selling their client’s gold assets (sometimes without permission) in a price fixing scandal, which kept gold prices in the U.S. and Europe lower than the rest of the world. Deutsche Bank settled a lawsuit, and agreed on Dec. 2, 2016 to name names of other banks that were price-fixing gold.  © The World Gold Council at Gold.org. Used with permission. 13. Are annuities safe? Insurance products, including life insurance and annuities, aren't insured by the FDIC. If we had not bailed out AIG in 2007, more than 50 million annuity holders would have been in real trouble. Your annuity product is only as safe as the insurance company that is selling it to you. According to the Federal Reserve Board’s Nov. 2021 Financial Stability Report, leverage is high at insurance companies. Insurance products are like being a renter. If you can’t pay, you get tossed out. Many people pay for life insurance their entire working life, and then can’t pay when they retire – when they are really most in need. If you put that money into your own tax protected account, you could save on taxes, compound your gains, and it would be there for you when you retire, even offering some income, in addition to the capital. When you can no longer contribute to it, it supports you. You can be a better steward of your wealth than any insurance company, once you learn the ABCs of money that we all should have received in high school. It’s time to be the boss of your money. 14. What were the top performing and the worst months for stocks over the past five years? April, November, July and January performed best over the 5-year period (in that order), on average. February, March and September were negative months. Retreat Attendees receive charts of the top-performing months and election year trends. If you’re interested in learning more about our 3-day, life transformational investor educational retreats, call 310-430-2397 or email info @ NataliePace.com. 15. What was the top performing quarter for stocks over the past twenty years? October through December – the Santa Rally – performed the best over the 20-year period, but saw greater volatility in the 5-year trend. December 2018 was the worst performing December in history, killing the historical returns of the Santa Rally that year. Understanding seasonal trends can help you with your annual rebalancing in your nest egg, and with your selling strategy for your trading. We spend one full day on what’s hot, teaching you how to identify the best investments of the year, in our Investor Educational Retreats. 16. What was the worst investment in 2021, NASDAQ, gold, the Dow Jones Industrial Average, bonds, cannabis, oil or real estate? Cannabis was by far the worst investment in 2021. As one example, Tilray soared to $67/share on February 10, 2021. It was trading at $6.86 on Jan. 14, 2022. Gold lost money, too, with prices down 7.1%. Bonds were pretty poor performers, offering limp yields and capital losses. Will the U.S. decriminalize cannabis? Will cannabis stocks shoot the moon again, fueled by Reddit bulletin boards and Robinhood investors? Stay tuned into my blogs and videoconferences for ongoing news, analysis and vital investor information. Email [email protected] with VIDEOCON in the subject line to receive the logon information for the next monthly videoconference. 17. Which year is expected to perform better, 2022 or 2023, based upon historical returns of election years? 2022 is a mid-term year. Over the last 10-20 years, mid-term years have been the worst performers, with annual gains of 1-5%. 2022 GDP growth could be just 4.0%, lower than the GDP growth of 2021 (which is expected to come in at about 5.0%). Pre-election years (2023) can be some of the strongest in the election year cycle with annualized gains of 11.6%-16%. However, 2023’s GDP growth is predicted to slow to just 2.2% (as interest rates rise), which is a negative for returns. U.S. stocks in 2022 are quite pricey, which could mute gain possibilities this year. Having expensive stocks and real estate, as government support is pulled back, will increase the volatility on Wall Street. There could be some wild rides this year. 18. How many companies are in the Dow Jones Industrial Average? 30 companies. Many are household brands. Most have been around for over half a century, and many are carrying far more debt than the value of the company. Leverage has begun to concern economists. Over 50% of the S&P500 corporate bonds are at the lowest rung of investment grade, or at junk bond status. This includes a lot of banks, brokerages, financial services and insurance companies. Ford Motor Company was downgraded to junk bond status in fall of 2019. If you don’t understand how much debt corporations are holding, you can learn how to use this valuable tool to increase the performance of your nest egg on the 2nd day of the Investor Educational Retreat. Debt and leverage, along with subdued sales, are the main reasons why the DJIA has underperformed the NASDAQ Composite Index in the 21st Century. Click to access the names of the 30 companies. The Dow Jones Industrial Average was launched in 1896. 19. How many Dow Jones Industrial Average companies were bailed out or went bankrupt in the Great Recession? Most people don't realize that 20% of the companies of the Dow (6 companies: AIG, American Express, Bank of America, Citi, JP Morgan and General Motors) were bailed out or went bankrupt in the Great Recession. Others, like General Electric and Ford, received support. New Chips, like Google, Amazon, Nvidia, Meta and Zoom, are far safer, and higher performing, than the debt-laden Blue Chips, both in terms of growth, but also in terms of the fiscal health of their balance sheets. (Apple and Microsoft are now a part of the DJIA.) You’ve probably heard the acronym FANG. We’ve now changed it to ZANA MAD MAAX. (Click to read that blog.)  Learn more about how to add in performance and avoid the bailouts in your funds and retirement account at the Investor Educational Retreat and in The ABCs of Money. Value was such a dismal performer over the past few years that Wall Street is coming up with a new definition for this style of investing. (What’s of value when stocks are trading at all-time highs?) Remember: the higher the dividend, the higher the risk (read the chapter of the same name in The ABCs of Money for additional information). 20. Which index has performed better since the COVID-19 pandemic hit in February of 2020, the Dow Jones Industrial Average or the NASDAQ Composite Index? The NASDAQ scored 43.6% gains in 2020, with the DJIA limping along at 7.2%. 21. How much did investors lose between February 19, 2020 and March 23, 2020? Both the Dow Jones Industrial Average and the NASDAQ Composite Index dropped 35%. Some of the hottest stocks, including Nvidia (-38%), lost even more. However, technology stocks surged, once everyone started working and doing everything from home. 22. How much did investors lose during the Great Recession and the Dot Com Recession? The Dow Jones Industrial Average lost 55% in the Great Recession. The Dot Com Recession saw a drop in the NASDAQ Composite Index of up to 78%. It took the NASDAQ 15 years to crawl back to even. Investors haven’t fully recovered from those ruts. According to Pew Research, most Americans are worth less today than they were in 1995.

You can’t afford to lose more than half every 8-10 years, crawl back to even, only to lose more than half again. It’s time to step off of the Wall Street Rollercoaster and into time-proven, easy systems that protect your wealth, while outperforming the major indices. 23. Does Buy & Hope work? If not, what does? Buy & Hope lost more than half in 2000 and 2008 and 35% (or more) between February and March of 2020. Due to the amount of debt and leverage, and the slow rate of growth, Buy and Hold will not work going forward (until those problems are dealt with and cycled through). That is why Buy & Hope investors are worth less today than they were worth in 1995. Our easy-as-a-pie-chart nest egg strategies earned gains in the Dot Com and Great Recessions and have outperformed the bull markets in between. Working off of the pie charts, instead of the brokerage statement, allows you to take the emotions out of the plan, and rely, instead, upon a time-proven system. This pie chart system, with annual rebalancing, is a buy low, sell high plan on auto-pilot – prompting you to do what you should be doing at each rebalancing session. Email [email protected] or call 310-430-2397, if you’d like to customize your own sample pie chart. (We teach you this at the Investor Educational Retreat.) One more thing: low interest rates create asset bubbles. That is one of the reasons why assets drop so severely and swiftly in 21st Century recessions. Having the right amount safe is our best protection. 24. Why is it that so many investors are unable to Buy Low and Sell High? Buy low, sell high is a mantra that everyone knows. So, why do so few investors do it? There are a few reasons…

25. What is the 3-Ingredient Recipe for Cooking up Profits? 1. Start with what you know and love 2. Pick the Leader 3. Buy low; sell high (easy to say; hard to do) This recipe, along with my Stock Report Card, Four Questions, market strategies and data drilling, is how I earned the ranking of number one stock picker. The recipe is easy. Learning how to use these tools requires practice. You must begin by locating and analyzing data, which is actually less time and far more informative than reading blogs, which have a fraction of the information and might be written by a novice. Come to our next Investor Educational Retreat to learn firsthand how easy and effective this strategy is, and why it has worked through bull and bear markets for more than two decades now. Call 310-430-2397 or email [email protected] to learn more. 26. What are the Four Questions for Picking Winning Stocks? The Four Questions for Picking Winning Stocks. 1. What’s the product? 2. Who’s the customer? 3. Can the company continue to make a superior product going forward and get it to their customer at the best price before the competition? 4. Who’s the CEO and can s/he motivate the employees to make the best product faster, better and cheaper than the competition? As you can see, three out of four questions can be answered by being a good customer of the company. The 3rd question will benefit from you completing a Stock Report Card, and understanding how to use the data. So, the more you know about a company (ingredient #1 of the recipe for Cooking Up Profits), the easier it is to pick the leader. In the 2nd edition of Put Your Money Where Your Heart Is, I used these questions and tools to compare two companies. Google scored an A (in 2006, when it had only been publicly traded for 2 years). The Dow Component that I gave a D- to went on to declare bankruptcy a few years after this prediction was made (General Motors). Using the Stock Report Card and 4 Questions, I identified both of these trends years before these major events occurred. The book was written in 2006, three years before GM went bankrupt. In fact, I applauded Google on national television before its IPO, when most pundits pooh-poohed it. This is the power of asking the right questions and relying upon the data, rather than just listening to the mainstream media. (We also warned about General Electric years before it was booted from the DJIA.) So, are you an Einstein in investing? A complete novice? If you scored 21 correct answers or higher, then you’re in great shape! If you scored 18 right, then you are C-level. Below 18 correct indicates that you are in need of a refresher course in life math. (So, consider joining us at our next Investor Educational Retreat.) Call 310-430-2397 or email [email protected] to learn more. The High Cost of Free Advice A few years ago, our team was told yet another story about someone who lost a substantial amount of money by trusting the "free" advice of a financial advisor. Learn the truth about commissions & conflicts of interest & how to get a 2nd opinion now in the guest blog “They Trusted Him." Now He Doesn’t Return Phone Calls.” Know what you own. Protect your future now! Data Sources: (c) 2020 Morningstar Direct and The National Association of Realtors. All rights reserved. Used with permission. The information contained herein: (1) is proprietary; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar, the National Association of Realtors, the World Gold Council, Natalie Pace, nor any content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Learn time-proven 21st-century strategies, at our February 11-13, 2022 online Investor Educational Retreat. Call 310-430-2397 or email [email protected] to learn more now.  Join us for our New Year New You Financial Empowerment Retreat. Feb. 11-13, 2022. Email [email protected] to learn more. Register with a friend or family member to receive the best price. Click for testimonials & details. Other Blogs of Interest Real Estate Risks. What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Investor IQ Test 2021. Investor IQ Test Answers 2021 Crystal Ball. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  About Natalie Pace

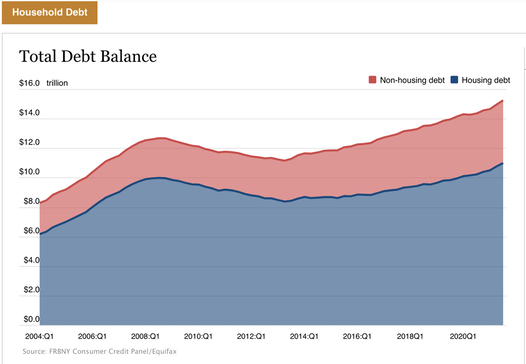

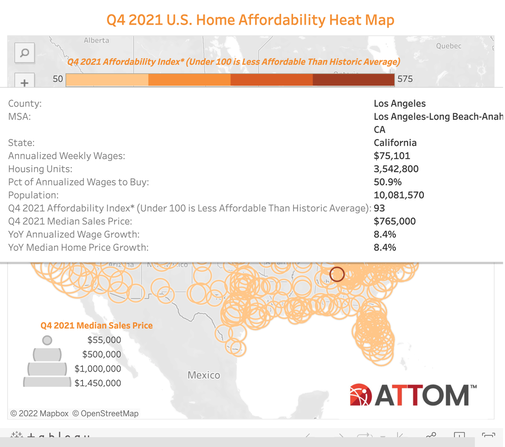

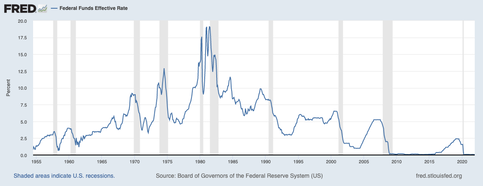

Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden.  Let’s start with the good news. The median price of a single-family existing home was $353,900 in November 2021 (source: National Association of Realtors). (This is lower than it was in June, when prices hit an all-time high of $362,800.) Interest rates are at rock-bottom. Student loan payments were recently paused through May 1, 2022. Low interest rates, government support, Work From Home, and a flight to more affordable suburbs lit housing on fire in 2020 and 2021. What will 2022 bring? The U.S. Economy in 2022 2021 GDP growth should come in at 5% or may be slightly higher. The 4Q 2021 GDP growth could actually be 4.7% or higher, which is a great deal better than 3Q’s 2.3%. When this is reported by the Bureau of Economic Analysis on January 27, 2022, investors might get happy again. We certainly have seen a lot of volatility on Wall Street, with the NASDAQ Composite Index down 6% on the year, as of the Jan. 14, 2022 close. How will Main Street homeowners react to the news? Home sales could continue to remain strong – until student loans must be paid, lenders rein in their loan approvals and interest rates rise, in May/June of this year. We’ll get our first look at the 2022 economy at the end of April, when the 1Q 2022 GDP is reported. Predictions are that 2022 GDP growth will be around 4.0%. It’s important to remember that investors are forward thinking. Institutional money is aware that the Fed Fund Rate is expected to rise on June 15, 2022, and again on September 21, 2022. The Fed Fund Rate is projected to be close to 1% by the end of 2022, and at 1.75% by the end of 2023 – unless inflation forces the Federal Reserve to act more aggressively. So, while housing might remain strong until summer, publicly-traded homebuilders might find themselves out of favor a few months before. (If you haven’t locked in your personal mortgage fixed rate, now is a great time to do so.) Unaffordability is Another Headwind for Housing 77% of counties are registering in the unaffordable price range, according to Attomdata. With housing taking up 25.2% of wages for homebuyers, on average, lenders are likely to be a lot pickier about who is approved for a mortgage. It’s also important to note that consumer debt hit an all-time high of $15.24 trillion in the third quarter of 2021. Add inflation to the mix of rising interest rates, the end of government support, unaffordable housing and tighter bank policies, and we could be seeing a dramatically reduced pool of buyers for real estate.   Homeowners I’m hearing first-time homebuyers talking about purchasing now to “lock in the low interest rates.” However, it’s even more important to understand what happens if you buy high, and the price of your home drops dramatically. When you have an underwater mortgage, your credit score plunges. You could be locked into a home that you can’t sell, with a lousy credit score, for up to a decade. The cycles in real estate are long. The high before the Great Recession was in 2006. The low occurred in 2011, and the recovery to 2006 prices didn’t happen until 2015. If you or someone you care about are thinking of buying a home at this time, it’s very important to go through the checklist that is outlined in the Real Estate section of the 5th edition of The ABCs of Money. It would also be a good idea to read the case studies that are listed there. One example illustrates a person who watched too many get-rich-quick ads and lost everything in 2008-2009, while another features a family that purchased low in 2011, doubled their money by 2017, and then used the proceeds to build an off-grid solar home.  Homebuilder Stocks Homebuilders, such as Hovnanian, Toll Brothers, KB home and Beazer Homes are all below investment grade, with very high debt. That means that few of these companies pay dividends. Their share prices soared in 2021 because housing was on fire. Hovnanian stock was trading at $6.44 in April 2020. It closed on January 14, 2022, at $120/share. KB home was it $12/share on March 23, 2020, and is now at $49. If you purchase these stocks now, you’re buying at a 4-year high. Could the stocks go higher? Homebuilders traded much higher in 2005, during the last housing heyday. Most of these homebuilders have a very large backlog. However, they are also affected by a supply shortage in building materials. (Supply chain issues hit Beazer Homes revenue in the 3rd quarter of 2021.) Most homebuilders are reporting extremely low cancellation rates – another good sign. But it is important to remember that cancellation rates were as low as they are now back in 2006, at 15%, but jumped to 42% by the end of 2008. The Optimism (Delusion?) of Commercial Real Estate CEOs In the 3Q 2021 earnings call, Boston Properties CEO Owen D. Thomas predicted that “It's only a matter of time before employers more strongly encourage their teams to return to in-person work.” Meanwhile BXP‘s leading region is New York City, and it is only 52% occupied. San Francisco is a ghost town with only 18% occupancy. Subleases are elevated and are going for under the market rate. Technology CEOs are embracing Work From Home. And Citrix did a survey with Millennials and Gen Z that showed 90% do not want to return to the office full-time and half wish to work from home full-time. One of the biggest reasons why the two largest working demographics don’t want to return to the city and the skyscraper office is that cities are just too expensive to live in. It’s important to remember that long-term leases are keeping the revenues at these office buildings stable. If a company wants to break the lease, there are punitive fees to pay. WeWork is perhaps the biggest red flag in this industry. The company took on long-term leases and required only a short-term commitment before Work From Home became a trend. It is believed that a great deal of the subleases on the market in NYC are from WeWork. (Building owners aren’t disclosing which tenants are subleasing.) WeWork recently went public via a SPAC. The company has a CCC+ rating with a negative outlook, lost $844 million in the 3rd quarter and has lower revenue in 2021 than it did in 2020 (by -18.5%). Judging from the surveys conducted by Citrix, Work-From-Home is a structural shift that is not going to go away. The Great Resignation that is currently happening has shifted the power from employers to the employed. Companies are forced to raise salaries, increase benefits and make concessions (such as flexible schedules and WFH) to attract talent. Private Placement REITs Private placement rates are even more troublesome. Many of these companies are cash negative and have been for quite a while. They pay a high yield to investors and a very high commission to broker-salesmen. If you’re being sold into these products as a safe way to earn income, then you better read D&T’s story. They fell for that sales pitch, and lost 18% of their principal. One of the most important market aphorisms is this: the higher the dividend, the higher the risk. https://www.nataliepace.com/blog/they-trusted-him-now-he-doesnt-return-calls Malls Malls are reporting 90% occupancy. However, a walk through the mall yields different results, with far more than 10% of the storefronts papered over with advertising or just glaringly empty. How are malls are coming up with their numbers? It could have something to do with accrual accounting or leases, even though the actual store fronts are shuttered. However, when the story that you hear doesn’t add up to what you’re seeing, that’s a red flag. Some of the biggest mall REITs pay 3-4% yield. You’re not getting paid very much at 3-4%, particularly if your principal investment is at risk of evanescing. Rising Interest Rates and Recessions At his confirmation hearing, Federal Reserve Board Chairman Jerome Powell made it clear that interest rates must rise to cool off inflation. The Summary of Economic Projections revealed that most of the Federal Reserve Board Governors believe interest rates will be closer to 2% by the end of 2023. That’s a lot higher than it is now, at zero. The chart below reveals just how correlated recessions are with rising interest rates. (The gray lines indicate the recessions.) The Federal Reserve Board will try to negotiate a soft landing – to raise rates without triggering a plunge in asset prices. However, as was mentioned in the Financial Stability Report released in November of 2021, “Asset prices remain vulnerable to significant declines should investor risk sentiment deteriorate, progress on containing the virus disappoint, or the economic recovery stall.” 2022 isn’t expected to stall, but it is expected to slow down.  “As the pandemic arrived our immediate challenge was to stave off a full scaled depression,” according to Jerome Powell. During the pandemic, stocks and real estate prices soared, while debt became absolutely astronomical. A depression was averted. However, it will take decades to pay off the trillions that have been borrowed.   Professor Robert Shiller's CAPE (P/E) Ratio. Jan. 13, 2022. The combination of expensive assets and overleverage are two of the reasons why we see such outsized and swift corrections in 21st-century recessions. Below are stock charts from the last three recessions. As you can see, the S&P 500 dropped 38% in the 2020 pandemic. The Dow Jones Industrial Average sank 55% in the Great Recession. It took 6 years to climb back to the 2007 highs (by 2013). The NASDAQ Composite Index plunged 78% in the Dot Com Recession, and took 15 years to recover.

Now would be a very good time to know what you own, and to begin underweighting real estate. It’s very important to understand what a properly diversified portfolio looks like, and not just rely upon somebody else to do this for you. If you had the nerve to lean into housing at the bottom in March 2020, then you have done quite well. Now is a great time to take your profits. If you’re interested in a 2nd opinion on your current plan, email [email protected] with 2nd opinion in the subject line to receive pricing and information.  Sample Pie Chart for a 25-year old. Are you acting your age? Do you know what is safe in a Debt World? You can learn the ABCs of money that we all should have received in high school, including time proven 21st-century strategies, at our February 11-13, 2022 online Investor Educational Retreat. Call 310-430-2397 or email [email protected] to learn more now.  Join us for our New Year New You Financial Empowerment Retreat. Feb. 11-13, 2022. Email [email protected] to learn more. Register with a friend or family member to receive the best price. Click for testimonials & details. Other Blogs of Interest What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Investor IQ Test 2021. Investor IQ Test Answers 2021 Crystal Ball. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  About Natalie Pace

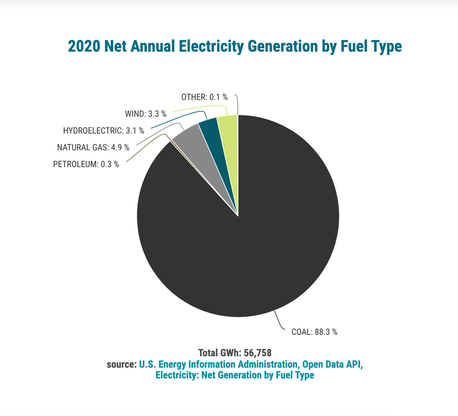

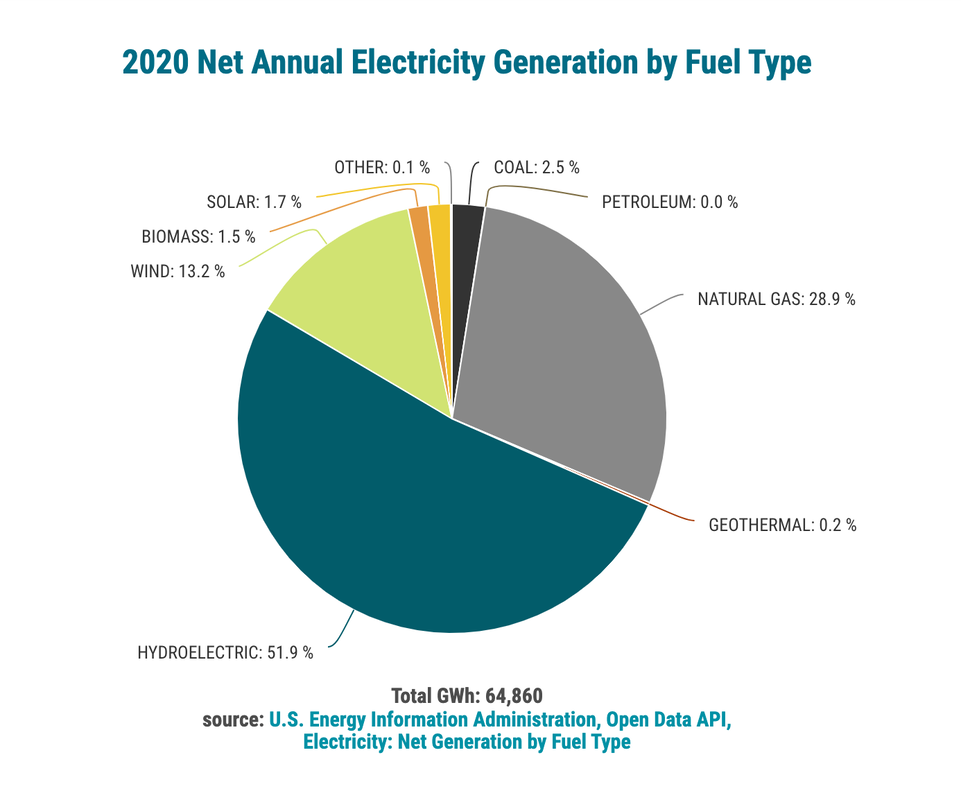

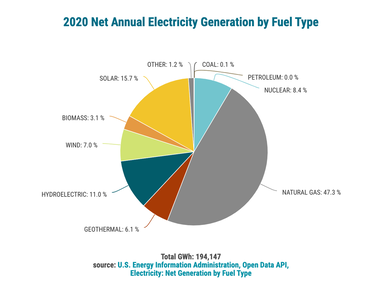

Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden.  Is it Solar’s Turn to Shine? Will the Winds Blow Favorably for Clean Energy? After COP26 in November 2021, the Glasgow Climate Act warned that greenhouse gas emissions must fall by 45% from 2010 levels by 2030 (just 8 years from now) in order for global warming to be maintained at 1.5°C above preindustrial levels. Why is this so important? 40% of Americans who experienced a climate emergency in 2021 understand, as do 80% of the country that experienced unprecedented heat waves. Imagine what happens as the world gets hotter and hotter. Global warming will end lives. Species will go extinct. Sea levels will rise. Storms will become more fierce and frequent, as will fires and droughts. Under the existing emissions reduction pledges agreed to act COP26, emissions will be nearly 14% higher in eight years. If countries do not meet their 2030 targets, we’re on track for temperatures to rise 2.4°C above preindustrial levels by the end of the century. There is a tipping point where we’ll all need to be much better swimmers and desert survivalists. This is not something in the distance (of 8 years). Here and now, climate disasters cost lives and a lot of money. Swiss RE projects that climate change will reduce the global economy by up to 18%. The National Flood Insurance Program is underwater again after being bailed out in 2017, when Congress canceled $17 billion of its debt. The leaders at COP26 all know what’s at stake, as do CEOs, Senators, Presidents and NGOs. So, will countries meet their targets? Will an emphasis on clean energy mean that it is solar power’s time to shine? Will the winds blow favorably for other renewable energy projects, such as wind, anaerobic digestion, biofuel and more? To see how clean energy stocks might receive tailwinds from climate action, I took a brief look at the policies of Canada and the United States. Currently, the U.S. and Canada have some of the highest CO2 footprints in the world, at 14 metric tons per person. Australia’s is 15 per capita. That compares to 4.85 in the United Kingdom (and most of Europe), 2.8 for Mexico and under 1 for most of Africa. China is the world’s biggest polluter (with 7.4 metric tons per capita), followed by the U.S. and India (1.77 per capita). If Europe can have a CO2 footprint that is 65% lower than the U.S. and Canada per person, clearly there is a great need for reducing our reliance on fossil fuels. We can’t see what happens in the rooms where decisions are made, but we can follow the money, and dig into the comments of the Joes who are in charge of climate policy. Here in the U.S., climate change policies have been hindered by one senator, namely Joe Manchin. Joe Manchin is the Democratic senator from West Virginia. West Virginia has the dirtiest electrical grid in the United States with about 93.5% of its electricity derived from fossil fuels. West Virginia’s grid is powered 88.3% by coal, with natural gas at 4.9% and petroleum at 0.3%. Clean energy makes up just 6.4% of the grid with hydro & wind.  West Virginia powers its electrical grid with 93.5% fossil fuels. Senator Manchin makes a lot more money from the coal industry, through his investments, than he does by being a Senator. Additionally, since coal is one of the main drivers of the West Virginian economy, he’s beholden to a lot of fossil fuel business leaders, including the billionaire coal baron who happens to be the governor of West Virginia, Jim Justice. Governor James "Jim" Justice (R) was worth $1.2 billion in 2020, according to Forbes. Justice is West Virginia’s only billionaire. In April 2021, he agreed to pay the federal government $5 million for coal mine violations (source: Forbes). When asked about his recalcitrance to champion clean energy projects, particularly since Manchin is the chairman of the Senate's Energy and Natural Resources Committee, Senator Manchin told CNN on Oct. 19, 2021, "The transition's already happening. So, I'm not going to sit back, and let anyone accelerate whatever the market's changes are doing.” Manchin has been quoted as saying that clean energy is unreliable and will cost ratepayers more money. Thankfully a lot of clean energy solutions come at the state and local level. There are incentives for utilities to increase the renewable mix, and there are tax credits for homeowners to power with solar and to improve the energy efficiency of their homes (26% this year and 22% in 2023). State level solutions are why California is powered 43% by renewables and Oregon’s grid is almost 70% clean, while many Gulf States and West Virginia are still heavily reliant on fossil fuels.

Despite Congressional gridlock, Richard Sansom, the Head of Commodities Research at S&P Global Market Intelligence, believes that 2022 will be a big year for clean energy. In a report released on November 10, 2021, Sansom wrote, “It’s going to be a record year for renewable energy development in the U.S. in 2022, with 44 GW of solar and 27 GW of wind power set to be installed alongside more than 8 GW of battery storage.” Canada’s Clean Energy Commitment Steven Guilbeault is the Canadian Minister of Environment and Climate Change. Guilbeault was a director and campaign manager for Greenpeace for 10 years, and is a founding member of Quebec’s largest environmental organization. It’s not too difficult to bet that Canada reaches its climate targets before the United States does. Leadership can make swift and powerful changes. Uruguay went from having its electric grid only 40% clean a decade ago to almost 100% today. Costa Rica is 95% powered by renewables. Sweden has a goal of being the world’s 1st fossil fuel free nation. Power to the People While leaders can shape policy and fund projects, consumers have more power than we realize. We could switch off the electricity when we don’t need it and save a lot. We could take public transportation and micro mobility for at least our local errands. We could work from home. We can make a commitment to stop being addicted to oil and gassing up so frequently. We can even install our own rooftop solar, particularly if we live in a sunny state. When the pandemic forced us to stay home, global CO2 emissions dropped further than any time since World War II, at -7% below 2019 globally and down -12% in the U.S. Tax credits make rooftop and commercial solar far more affordable. Some solar companies, such as Sunpower, are providing the financing for the project. Prices are low. The benefits are fantastic for homeowners who live in sunny states (who can save thousands annually on their electric bill) and for the planet (lowering CO2 emissions might heal our home). If you’re interested in greening your portfolio, many solar and wind companies are trading at very low prices, especially compared to last year. Below is a quick rundown of the companies and what they specialize in, along with some of the math on their business. If you’d like a copy of my Solar & Wind Stock Report Card, simply email [email protected] with Solar & Wind Stock Report Card in the subject line. Daqo (symbol: DQ) is a polysilicon manufacturer based out of China. Sales growth is an astonishing 367% year over year. Their products are in very high demand. Meanwhile, the share price is the $40 range, whereas it traded above $130/share last year. Having a company with this kind of astronomical growth trading at a price-earnings ratio of just 4 is a rare and potentially wonderful buying opportunity. Sunrun (symbol: RUN) is a rooftop solar provider based in San Francisco. California is a sunny state, so it’s not surprising that sales are more than doubling year over year. Sunrun’s share price is trading at a discount of 2/3 from its 52-week high. Renesola (symbol: SOL), based out of Connecticut, is a global solar provider. The company handles both large and community-based solar projects in the United States, Europe, Canada and China. Renesola’s sales are up 57% year over year, while the share price is down over 80% from its 52-week high. If S&P Global’s projections that solar power generation will increase by 44 GW turn out to be accurate, Renesolar should benefit. Canadians might prefer to bet on the domestic solar provider Canadian Solar (symbol: CSIQ). (Americans can invest, as well.) Canadian Solar’s revenue growth is about 36% year over year. However, with a new Canadian climate czar in charge, CSIQ should see brighter days. Canadian Solar has a very low price-sales ratio and is trading at a 52-week low. AMSC (symbol: AMSC) is a company that specializes in wind power, among other product lines. Wind had a challenging 2021. However, in AMSC’s most recent earnings call, AMSC’s CEO Daniel McGahn said, “We are in position for growth through the reemergence of our wind business, which we see coming as early as next fiscal year.” One of AMSC’s other divisions is its Resilient Electric Grid technology (REG). As McGahn explains it, “The REG system can be a critical asset for utilities in helping them deal with an evolving and more complex distribution grid” (a grid where multiple different sources are providing the power). AMSC’s REG system is in place in Chicago, with the potential to expand into other major utility providers. AMSC sales were up about 32% in the most recent quarter compared to the prior year. AMSC’s share price is down by 2/3. An additional 27 GW of wind power generation in the US in 2022 will also benefit TPI Composites (symbol: TPIC), a maker of wind turbines that is based out of Scottsdale, Arizona. Supply chain issues continue to be headwind for this company. The company sales are flat year-over-year. However, if the wind business accelerates and supply chain bottlenecks get unclogged, TPIC could see a better second half of 2022. TPIC’s share price is down 80% on the year’s high, and is trading at a very low price-sales ratio. Sunpower (symbol: SPWR) is the #1 U.S. solar company, with over 35 years in the industry. The company is vertically integrated, with a solar panel manufacturing division, rooftop solar installation, homeowner financing and large-scale projects. The company’s panels are highly efficient and have helped many collegiate teams win the Solar Decathlon over the years. The company also powers commercial campuses for Toyota, Johnson and Johnson, JFK Airport and Mt. Rushmore. Sunpower’s year-over-year sales growth was 18% in the most recent quarter. Having a marketing specialist as their new CEO could bode well for the company’s rooftop expansion – particularly now that they have their own financing division. Homeowner solar tax credits are 26% in 2022 and 22% in 2023. If their sales team is successful, Sunpower could shine in 2022. Sunpower is another clean energy company that has seen its share price sink by 2/3 from its 52-week high. If you’re more interested in dividends, then you might look into a few utilities that have been leading the clean energy revolution for many years – National Grid (symbol: NGG) and Portland General Electric (POR). Both companies have share prices near their 52-week highs. (So, have a dollar-cost-averaging plan for your purchase.) National Grid’s dividend is a little higher. Sunpower, National Grid and Portland GE all have elevated debt. I didn’t mention Enphase, First Solar or JinkoSolar in this blog. However, I did include them in the Stock Report Card. I'm also giving away 21 Days of Green video coaching (free) to anyone who is interested in living a more planet-friendly life and reducing your personal CO2 emissions. Email [email protected] with 21 Days of Green for your free gift from us. Full Disclosure: I have investments in some of the companies mentioned in this blog. If you're interested in protecting your wealth, earning money while you sleep, the power of compounding gains, how to invest tax-free or how to construct and evaluate your own Stock Report Card, join us for our Financial Empowerment Retreat February 11-13, 2022 online. Email [email protected] with Retreat in the subject line or call 310-430-2397 to learn more and to register now. Access additional information, including pricing, curriculum and testimonials, by clicking on the banner ad below.  Join us for our New Year New You Financial Empowerment Retreat. Feb. 11-13, 2022. Email [email protected] to learn more. Register with a friend or family member to receive the best price. Click for testimonials & details. Other Blogs of Interest What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions Will There Be a Santa Rally? The Dangerous Debt Ceiling Game The Robinhood IPO. Will the Crypto Crash Hit Tesla, Square & Coinbase? China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! 2021 Financial Freedom Sweepstakes Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? Will Cannabis be Decriminalized This Summer? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Beyond Meat, Oatly & The Very Good Food Co. Is Cryptocurrency the New Gold? Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Tesla & Nio Will Report Spectacular Earnings. The Coinbase IPO. Restore Our Earth on April 22nd (and Every Earth Day). Should You Sell in May and Go Away? Adding Shoot the Moon Performance to Your Nest Egg. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Kushner's Times Square Building Plunges 80% in Value. Will There be a Spring Rally? Cannabis and the Road to Decriminalization in the U.S. Hot ETFs Return Up to 50% Since October. Investor IQ Test 2021. Investor IQ Test Answers Shoot the Moon Stock Picks 2021 Crystal Ball. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? Can Medmen Avoid Bankruptcy? Bitcoin is Back, Baby! Real Estate Prices are Going Up. And Down. Cannabis is Decriminalized. Stocks Triple. Thanksgiving in a Pandemic. The Sustainability Silver Lining. Money Stress Killed My Friend Real Estate and Housing 2021. Challenges & Opportunities Real Estate in a Pandemic. Interview with Mike Fratantoni, the Chief Economist of the Mortgage Bankers Association. Bonds are Illiquid & Negative-Yielding. Annual Rebalancing is a Buy Low, Sell High Plan on Auto-Pilot. Is Your Bank a Junk Bond Put Your Money Where Your Heart Is. Schwab's Chief Fixed Income Strategist on What's Safe. China's Tesla (Nio). 2Q Sales Soar. Why Are You Still Renting? (Errr. There is More Than This to Consider!) Wealth Myths That Keep You Poor. Prosperity Truths That Make You Rich. Technology and Silver are Golden. Real Estate: Feeling Equity Rich? Make Sure That Feeling Isn't Fleeting. Airline Revenue Plunges 86%. 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  About Natalie Pace