Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

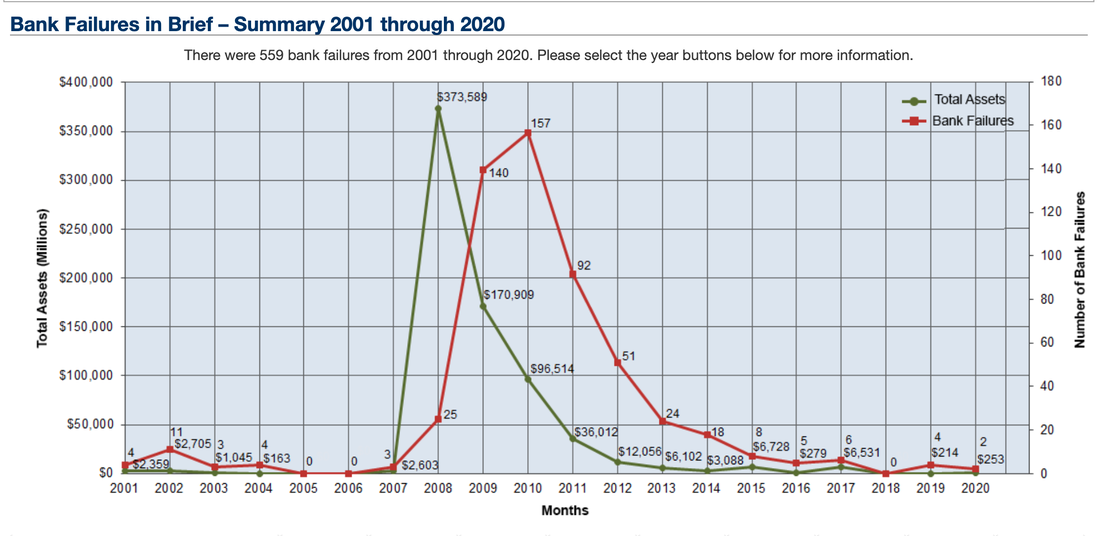

FDIC eagle seal in the main lobby of the headquarters building by the White House. 2009. Author: Matthew G. Bisanz. Wiki Commons. Used with permission.  Dear Natalie. Does the Bank Bail-In Plan put my FDIC-Insured deposits at risk? I recently read a blog that said the IMF has approved a bank bail-in plan that allows them to seize FDIC-insured deposits. Signed: Whom can I trust? Dear Trust Results: I’m starting my answer off with the reminder to trust results. Before you read anything, grade your guru. Does s/he have a background in economics or an impressive track record for more than 15 years? Is s/he endorsed by real people and experts, or is s/he simply a self-proclaimed expert? The reason that I’m starting here is that I saw a number of red flags when I looked at the writer of the blog. The writer uses a pen name, hides his identity, calls himself a Jack-of-all-trades, has no background in economics or finance (but rather in engineering) and doesn’t know even basic financial terms. When I read the blog itself, my suspicions were confirmed. This writer has based his entire premise upon one inaccurate claim. (I’m not naming the blogger or linking to his blog specifically. This could be something claimed by anyone.) Here is what the blog claimed: “During the recent G20 meeting (mid-November), the member nations decided that your bank deposits will become property of the bank if a crisis takes it down.” He quoted from an IMF document that described that the IMF could “restructure the liabilities of a distressed financial institution by writing down its unsecured debt and/or converting it to equity.” He then claimed that unsecured debt includes deposits. That is a false claim, and it is also refuted by the very document that he quotes from. As one other point, he wrote his blog in 2019, whereas the IMF document he refers to is from 2012 (i.e. not recent). Unsecured debt refers to bonds and loans that are specifically “unsecured.” This is a common financial term. (It appears that the blogger is not aware of the definition of it, however.) In the IMF document it specifically states, “To improve transparency and avoid uncertainty, only subordinated and senior unsecured debt should be subject to bail-in. Insured/guaranteed deposits, secured debt (including covered bonds), and repurchase agreements should be excluded from restructuring… Pre-restructuring shares are completely written off, but deposits, repos, and other short-term funding are not affected by the bail-in power.” (Bold emphasis added.) I’m linking to the IMF document so that you can read it yourself. One of the most important things to understand is that “debt” does not include deposits. Deposits are not loans or bonds. Real-World Examples of How This Works Did you know that there have already been two bank failures this year? The First State Bank in West Virginia became MVB Bank on April 3, 2020. Ericson State Bank in Nebraska became part of Farmers and Merchants Bank on February 14, 2020. We can expect more to come, as the current pandemic crisis unfolds. During and after the Great Recession, between 2008 and 2012, 465 banks failed. Depositors kept their money. Shareholders lost everything. Bondholders were given a “haircut” on their principal investment, and oftentimes were given new stock in the new bank. That is why it is so important to re-evaluate your stock and bond portfolio, and strategy, now.  Source: FDIC. Most depositors don’t even notice because the sign on the door changes, and operations continue under the new name. If you want to see how deposits are treated, check out the First Federal Bank failure from 2009 for details. You can also refer back to my blog on FDIC, SPIC, money market funds and cash under the mattress. Money Market Funds and Certificates of Deposit In 2017, there was a new rule applied to money market funds allowing them to apply redemption gates and liquidity fees. Redemption gates and liquidity fees were designed to prevent “runs” on money market funds. If the fund gets into trouble, it can suspend your ability to withdraw your cash and/or charge you a fee to withdraw your money. Since the funds did indeed get into trouble in March 2020, it is very important that you understand what those terms mean, and that money market funds can lose money. They, like all mutual funds and insurance products, are not FDIC-insured. The current Money Market Mutual Fund Liquidity Facility ends on September 30, 2020, unless the Federal Reserve Board agrees to extend it. Certificates of Deposit can be FDIC-insured or not. So, you have to read the fine-print on your CD to determine what the terms are. There can be an opportunity cost for CDs. If you need or want the money before the term ends, your early withdrawal penalty fee can be far above what the return on the investment is. High-yielding CDs are typically not FDIC-insured, and are often subject to capital loss if the underlying index it is tied to loses money. This is also true of annuities and other insurance products. Getting Safe is a 2-Step Process Getting safe is a two-step process. Hard assets will hold their value better than paper assets in the years to come. However, hard assets are expensive right now, and vulnerable to capital loss, too. If you buy them too high, you’ll lose money. If you’ve borrowed to buy them, you could lose the hard asset to boot. So, the first step to getting safe is to keep your money. FDIC-insured cash is safer than “debt” of all kinds, money market accounts and non-insured CDs. After you keep your money, start looking for safe, income-producing hard assets that you can purchase for a good price (when prices correct). Liquidity affords you the opportunity to buy low. What are some safe, income-producing hard assets that you can purchase for a good price? That is something that we spend one full day discussing in my Investor Educational Retreats. In short, you have to think about Return on Investment differently. You’ll also need to apply 21st Century strategies. What worked just a few months ago, like buying a place and putting it on Airbnb for top dollar, has put a lot of opportunists in financial despair. Wisdom and time-proven strategies are the cure. Avoid reading blogs before you grade your guru. If you are interested in learning what's safe in a world where stocks, bonds and money market funds are all subject to capital loss, consider joining me for my next Financial Empowerment Retreat, June 13-15, 2020. Get additional information by clicking on the banner ad below.  Other Blogs of Interest Why Did my Bonds Lose Money? Cannabis Update. Recession Proof Your Life. Free Videocon Monday, May 10, 2020. The Recession will be Announced on July 30, 2020. Apple Reports Terrible Earnings. We Are in a Recession. Unemployment, Rising Stocks. What's Going On? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. 21st Century Solutions for Protecting Your Home, Nest Egg & Job. Wall Street Insiders are Selling Like There is No Tomorrow. Why Are My Bonds Losing Money? Tomorrow is Going to be Another Tough Day. Price Matters. Stock Prices are Still Too High. Should You Ride Things Out? 7 Recession Indicators Corona Virus Update. The Bank Bail-in Plan on Your Dime. NASDAQ is Up 6X. CoronaVirus: Which Companies and Countries Will be Most Impacted. Is Tesla Worth GM and Ford Combined. Artificial Intelligence is on Fire. Is it Time to Buy S'More? Take the Retirement Challenge. 2020 Investor IQ Test. Answers to the 2020 Investor IQ Test. The Cannabis Capital Crunch and Stock Meltdown. Does Your Commute Pollute More Than Planes? Are Health Care Costs Killing Your Budget? 2020 Crystal Ball. The Benefits of Living Green. Featuring H.R.H. The Prince of Wales' Twin Eco Communities. What Love, Time and Charity Have to do with our Commonwealth. Interview with MacArthur Genius Award Winner Kevin Murphy. Unicorns Yesterday. Fairy Tales Today. IPO Losses Top $100 Billion. Counting Blessings on Thanksgiving. Real Estate Prices Decline. Hong Kong Slides into a Recession. China Slows. They Trusted Him. Now He Doesn't Return Phone Calls. Beyond Meat's Shares Dive 67% in 2 Months. Price Matters. Will There be a Santa Rally? It's Up to Apple. Will JP Morgan Implode on Fairy Tales and Unicorns. Harness Your Emotions for Successful Investing. What the Ford Downgrade Means for Main Street. The Dow Dropped Over 1000 Points Do We Talk Ourselves into Recessions? Interview with Nobel Prize Winning Economist Robert J. Shiller. Ford is Downgraded to Junk. From Buried Alive in Bill to Buying Your Own Island. The Manufacturing Recession. An Interview with Liz Ann Sonders. Gold Mining ETFs Have Doubled. The Gold Bull Market Has Begun. The We Work IPO. The Highs and Hangovers of Investing in Cannabis. Recession Proof Your Life. China Takes a Bite Out of Apple Sales. Will the Dow Hit 30,000? A Check Up on the Economy Red Flags in the Boeing 2Q 2019 Earnings Report The Weakening Economy. Think Capture Gains, Not Stop Losses. Buy and Hold Works. Right? Wall Street Secrets Your Broker Isn't Telling You. Unaffordability: The Unspoken Housing Crisis in America. Are You Being Pressured to Buy a Home or Stocks? What's Your Exit Strategy? It's Time To Do Your Annual Rebalancing. Cannabis Crashes. Should You Get High Again? Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth. The Zoom IPO. 10 Rally Killers. Fix the Roof While the Sun is Shining. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. Earth Gratitude This Earth Day. Real Estate is Back to an All-Time High. The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2018 is the Worst December Since the Great Depression. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed