Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

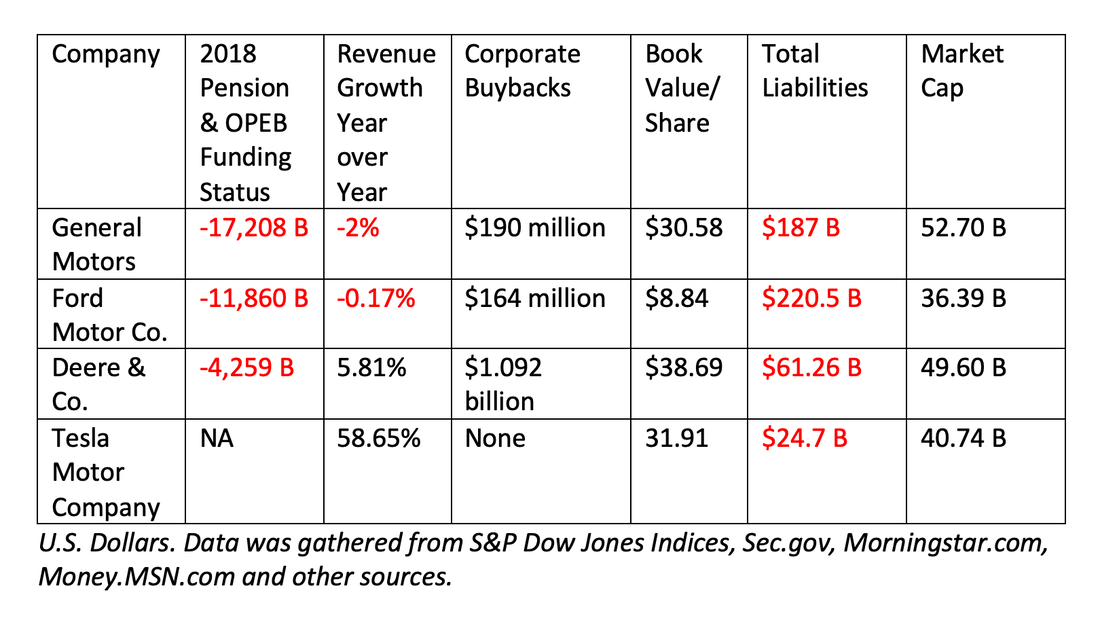

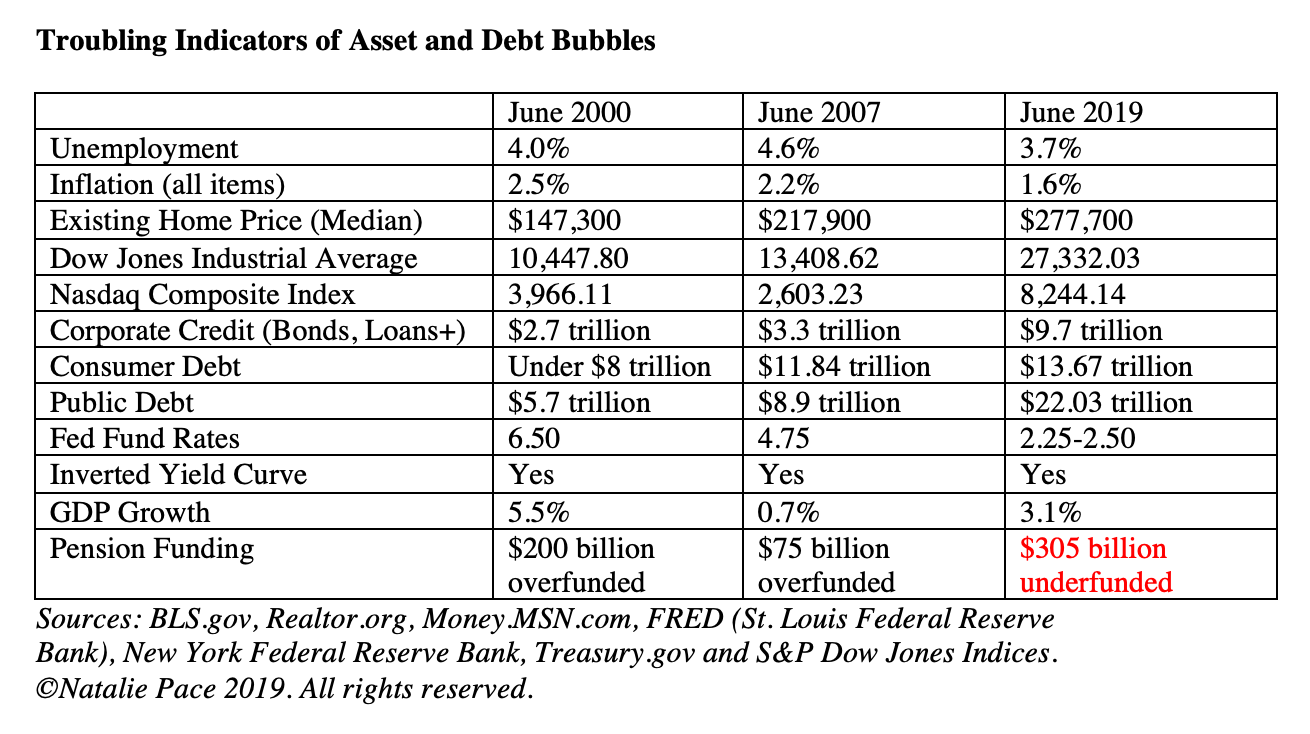

Ford Bonds Cut to Junk By Moody’s. Over 50% of investment grade bonds are at the lowest rung (as Ford was) – just above a junk rating. On September 9, 2019, Moody’s Investors Service downgraded Ford bonds to junk. According to a press release from Bruce Clark, a Senior Vice President with Moody's, "Ford is restructuring from a weak position and [is] below the performance of investment-grade rated auto peers." Ford is expected to “remain weak through the 2020/2021 period, including a lengthy period of negative cash flow from the restructuring programs.” The last time Ford bonds were cut to junk was in 2005, a few years before the Great Recession. Ford managed to avoid bankruptcy at that time, and returned to investment grade in 2012. Chrysler and General Motors both went through restructuring. However, both Ford and General Motors continue to have financial health challenges. Check out some of the fiscal issues that are still present below.  Report Card (c) 2019 Natalie Pace. All rights reserved. As you can see, Ford’s liabilities are over $220 billion, while the market value of the company is a mere $36.4 billion. Revenue is down year over year. And the auto company is over $11 billion underfunded on its pension and other post-employment benefit obligations. None of this bodes well for Ford’s ability to withstand restructuring in the years ahead, unless the company has a dramatic market disruption product up its sleeve. Looking at this information, it makes more sense why Moody’s is now classifying Ford bonds as speculative. However, the problems in the bond market are not limited to the auto industry. Over 50% of investment grade bonds are almost junk. The Federal Reserve Board continues to monitor this leverage concern in their Financial Stability Report. In the May 2019 report, the Feds wrote, “Borrowing by businesses is historically high relative to gross domestic product (GDP), with the most rapid increases in debt concentrated among the riskiest firms amid signs of deteriorating credit standards.” In my interview with Liz Ann Sonders last month, she warned that “This highly indebted, weak component of the corporate sphere will mark the end of this cycle in some way.” The Safe Side of Your Nest Egg is Vulnerable to Capital Loss During the last two recessions it was easy to stay buoyant in your retirement plan simply by overweighting more into bonds. In the next recession, that’s unlikely to be the case for two reasons: 1. Overleverage, and 2. Interest rates are starting out too low to begin with. In fact, in 2018, both stocks and bonds lost money – as a signal and warning of how the two markets could move in tandem going forward. Overleverage Many of the risky firms that are borrowing from Peter to pay Paul are using corporate buybacks to juice their earnings and keep their stock price high, while they rack up more debt and liabilities. General Electric is the poster child of what happens when companies prioritize stock price (which helps the C-suite executives bank their own profits) above products and staff. General Electric’s share price has lost 75% of its value. The dividend has been cut to 4 cents. Pension and other post-employment benefits are underfunded by $27.2 billion, while total liabilities are an astonishing $258 billion, compared to $71 billion in market cap. Other firms with debt and liabilities above the value of the company include AT&T, GM, IBM, Ford, Exelon and Deere & Co. The problem with overleverage is that banks have exhibited little appetite to curb themselves from this risky behavior. During the run up to the great recession, Wall Street financiers knew that they were selling mortgages to people who could not afford to pay them, and reselling mortgage products to investors who thought they were of higher quality than they were. Many Americans were using their home-equity as an ATM machine. If you go back and Google articles on homeowners using equity as an ATM machine, you’ll see a plethora of hits dating back as early as 2005. So why did mortgage banks continue to lend based on liars’ loans to people who really weren’t creditworthy? And why did big banks like Goldman Sachs, JP Morgan Chase, Wells Fargo, Bank of America, Washington Mutual, Wachovia, Bear Stearns and Lehman Brothers continue to package those mortgages into credit default swaps and structured investment vehicles? Because they were making a lot of money doing so. The term being used at the time was the Biggest Fool Theory. It was like a game of hot potato. They knew the music would stop. You just didn’t want to be the one left holding the potato when it did. Today the risk festival is concentrated in corporate bonds (although consumer debt is also higher than ever, at just under $14 trillion). Banks rack up high fees and decent interest borrowing at 2% and lending at 5% to over-leveraged corporations. (They can lend at 25% or higher to individuals with credit cards.) The financial sector is also borrowing to buy back their own stock – with the result of earnings looking stronger than they would otherwise be, and the share price looking more affordable to the less-sophisticated investor. Interest Rates Are Starting Out Too Low As you can see from the below chart, interest rates are starting out far too low for the late stage of this business cycle. During recessions, when the Central Bank cuts interest rates, bonds typically enjoy a bull market. The top performing asset in 2001 was bonds, with many being sold for up to a 25% premium. Bonds did quite well in 2008, too. By 2009, we started to see elevated risk, which culminated in the Greek bond crisis, and the bankruptcy of counties and cities across the US., including Stockton California and Detroit Michigan. Low interest rates have stoked the fire of risk since that time, to the levels seen today. Low interest rates also create asset bubbles, another area of concern mentioned in the Federal Reserve Board’s Financial Stability Report.  This time around, with interest rates at only 2%, there is not enough room to cut rates to cause a rally in bonds. With so many bonds concentrated at just above junk status (over 50%), the overleverage could mean restructuring – which means your capital is at risk, in addition to the measly return you are being offered to take on that kind of risk. Junk bonds face liquidity risk – meaning that if you want to dump them, you might not find a buyer on the other side of that trade. So, “investment grade” bonds and bond funds are not nearly as “safe” as the name implies. The bottom line is the safe side of your portfolio is at risk of capital loss, just like the “at risk” side is. (Again, 2018 exhibited this in spades with bonds losing money in tandem with the stock market.) Main Street has not been adequately forewarned of this – or appraised of the risks posed by perpetually low interest rates. Relying upon someone else to protect your assets during this challenging time could be a losing proposition, particularly if your financial manager lost 1/3 or more of your assets during the last downturn (the Great Recession). Even if your portfolio did okay in 2008, you might be vulnerable, if you are overweighted in bonds. Yes, there are solutions, time proven solutions that earned gains in the last two recessions and have outperformed the bull markets in between. So, why don’t more brokerages offer them? They just don’t offer the kind of fees and profits to the financial services industry that keeping you invested in risky assets do. The industry is moving more toward Modern Portfolio Theory and annual rebalancing. However, there are still a lot of firms and managers who are employing the outdated, losing system of Buy and Hope. Buy and Hope has lost more than half in the last two recessions. That’s why now is the time to learn the basics – the ABCs of money that we all should’ve received in high school. You must be the boss of your money. If someone else loses a significant portion of your nest egg while they are managing it, it is with your permission, and the losses are yours to keep. The brokerage can still make money, even when you lose. Complacency was not a friend in 2000 or 2008, and it will not be your friend in the next downturn. Wisdom is the cure. The sooner you learn and incorporate time-proven solutions, the faster your life transforms. Call 310-430-2397 or email info @ NataliePace.com to learn how to get an unbiased 2nd opinion on your current plan. Join me at my next investor educational retreat in Arizona, Oct. 19-21, 2019.

Other Blogs of Interest From Buried Alive in Bill to Buying Your Own Island. The Manufacturing Recession. An Interview with Liz Ann Sonders. Gold Mining ETFs Have Doubled. The Gold Bull Market Has Begun. The We Work IPO. The Highs and Hangovers of Investing in Cannabis. Recession Proof Your Life. China Takes a Bite Out of Apple Sales. Will the Dow Hit 30,000? A Check Up on the Economy Red Flags in the Boeing 2Q 2019 Earnings Report The Weakening Economy. Think Capture Gains, Not Stop Losses. Buy and Hold Works. Right? Wall Street Secrets Your Broker Isn't Telling You. Unaffordability: The Unspoken Housing Crisis in America. Are You Being Pressured to Buy a Home or Stocks? What's Your Exit Strategy? Will the Feds Lower Interest Rates on June 19, 2019? Should You Buy Tesla at a 2 1/2 Year Low? It's Time To Do Your Annual Rebalancing. Cannabis Crashes. Should You Get High Again? Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth The Zoom IPO. 10 Rally Killers. Fix the Roof While the Sun is Shining. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. Tesla Delivery Data Disappoints. Stock Tanks. Why Did Wells Fargo's CEO Get the Boot? Earth Gratitude This Earth Day. Real Estate is Back to an All-Time High. Is the Spring Rally Over? The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What's Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed