Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

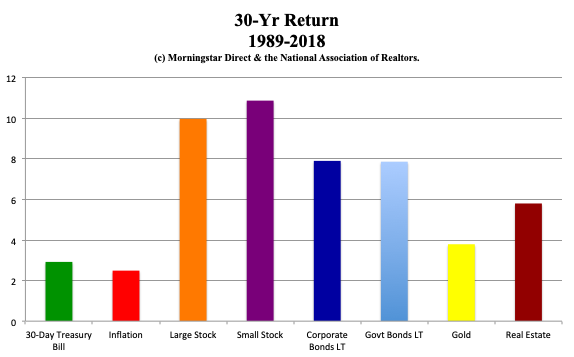

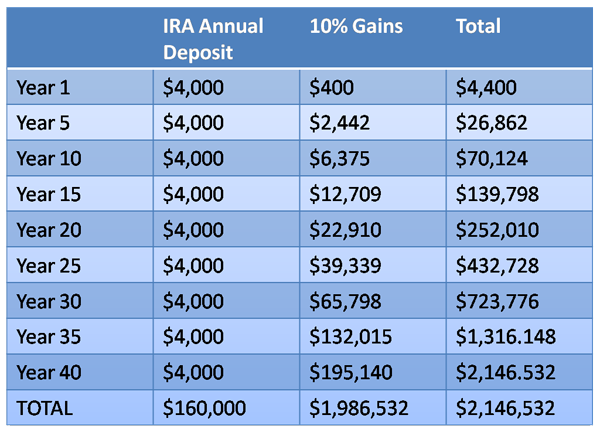

Natalie Pace, author of the bestselling book The ABCs of Money (and others) and co-creator of the Earth Gratitude project. Many people today are overwhelmed with their bills. We’re juggling school, family, soccer, test scores, skinned knees, taxes, college funds and our aging parents. Acckk! It’s easy to just get swallowed up by the system, which is one that will have you making everyone else rich at your own expense. Part of the solution is to reduce your big-ticket bills. Smarter choices in housing, transportation, utilities and taxes will offer you savings of thousands of dollars annually. That’s a bucket list vacation each year! Learn more about those strategies in the 2nd edition of my bestseller, The ABCs of Money. Cutting out café lattes can save you a few hundred dollars, but it is not your ticket to financial freedom. Another piece of the winning formula is to start earning money while you sleep. When your assets (home, retirement plan, savings, etc.) increase in value, everything becomes easier. Your assets to debt increase, which raises your FICO score. Your wealth increases. You can read how investing was my springboard out of almost losing my home to a dream come true lifestyle in my book, You Vs. Wall Street. The math is simple. If you earn $100,000 a year and you put 10% of your gross salary in a 401K, IRA and/or health savings account, and that money earns 10% annually (what stocks and bonds have done over the last 30 years, on average), then you'll have $50,000 in your nest egg within four years, over $100,000 in seven years and by year 25, your money will earn as much as you do in your annual salary, and you’ll be a millionaire.  Data provided by and (c) Morningstar, Inc. and the National Association of Realtors. Used with permission. NataliePace.com. Investing alone can make you a millionaire before you’re 50 (if you start at 25). It will offer your child half a million in her college fund within 18 years. Investing yields four times (or more) the money you gain if you were just saving it. (25 years of $10,000 annual deposits with zero interest is $250,000.) Now, you might say, “I don’t earn $100,000 a year!” But the ratios work the same, even if you earn minimum wage. If you deposit 10% and that earns 10% returns, then your nest egg will equal your salary in just seven years, and by year 25, your nest egg will earn as much as you do. By comparison, if you are just saving, you only earn a fraction of that – missing out on all of the gains that compound year after year. If you’re not saving at all, you’re overspending and trapped in the vicious cycle of debt and debt consciousness.  Chart (c) 2019 Natalie Pace. All rights reserved. If you’re investing in an account that is not tax-protected, then you’re also getting killed in capital gains taxes. (401Ks, IRAs, college funds and HSAs offer many protections, including savings on income and capital gains taxes). Qualified retirement funds are also financial predator-proof. No matter who you owe money to, they can’t touch your retirement accounts. This is just one of the reasons why you must pay yourself first, even if you’re in debt. If you wait to pay off debt before you start investing in your own financial freedom, wealth and future, then you’re just making the debt collector rich at your own expense. You’re missing out on compounding gains. You’re suffering from debt consciousness. Your financial freedom depends upon you adopting wealth consciousness and providing for and protecting your own livelihood and future first. (Yes, you’ll still want to pay down debt. However, you’ll understand how increases your own assets and money while you sleep is one of the most effective tools to doing that.) Over the last two decades, stocks have been pretty rough sailing – for Buy and Hope investors. The NASDAQ Composite Index lost 78% in the Dot Com Recession. The Dow Jones Industrial Average dropped 55% in the Great Recession. Buy and Hope has investors losing more than half every 8-10 years, then crawling back to even, only to see another plummet.

The financial indicators today are even more troubling than they were in 2000 or 2008. However, investors that diversified properly and used annual or quarterly rebalancing, earned gains during the last two recessions and have far outperformed the bull markets in between. That strategy is easy as a pie chart. You can read about this time-proven system in my books. You can learn and implement it firsthand by attending my Investor Educational Retreat. Check out Nilo Bolden’s testimonial by clicking on her name. The most important first steps to take are to open the account, put 10% of your income on auto-deposit and to switch your thinking about money. Which is why I’m encouraging you to toss out the phrase "retirement plan" and select a sexier name for your personalized “Buy My Own Island Plan" or “Send My Kid to College Fund” or “Trip Around the World Dream.” Why? Because you’ll want to grow the gains of the fund that is working toward a goal. Whereas, odds are, you’re filing the “retirement plan” statements directly in some drawer without looking at them, hoping they’ll surprise you one day -- pleasantly. That is, if you have even bothered to sign up for the 401k, Individual Retirement Account or Health Savings Account in the first place. If you want a pleasant surprise, you need a time-proven plan. So, if you really want to go from paying bills to life’s a beach! get started now. Once you learn and implement a winning strategy, and commit to rebalancing it 1-3 times a year, you’ll be on the right track. Wisdom is the cure, and the time is now. Call 310-430-2397 to learn The ABCs of Money that we all should have received in high school.

Other Blogs of Interest The Manufacturing Recession. An Interview with Liz Ann Sonders, the Chief Investment Strategist of Charles Schwab, Inc. Gold Mining ETFs Have Doubled. The Gold Bull Market Has Begun. The We Work IPO. The Highs and Hangovers of Investing in Cannabis. Recession Proof Your Life. China Takes a Bite Out of Apple Sales. Will the Dow Hit 30,000? A Check Up on the Economy Red Flags in the Boeing 2Q 2019 Earnings Report The Weakening Economy. Think Capture Gains, Not Stop Losses. Buy and Hold Works. Right? Wall Street Secrets Your Broker Isn't Telling You. Unaffordability: The Unspoken Housing Crisis in America. Are You Being Pressured to Buy a Home or Stocks? What's Your Exit Strategy? Will the Feds Lower Interest Rates on June 19, 2019? Should You Buy Tesla at a 2 1/2 Year Low? It's Time To Do Your Annual Rebalancing. Cannabis Crashes. Should You Get High Again? Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth The Zoom IPO. 10 Rally Killers. Fix the Roof While the Sun is Shining. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. Tesla Delivery Data Disappoints. Stock Tanks. Why Did Wells Fargo's CEO Get the Boot? Earth Gratitude This Earth Day. Real Estate is Back to an All-Time High. Is the Spring Rally Over? The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What's Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed