Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

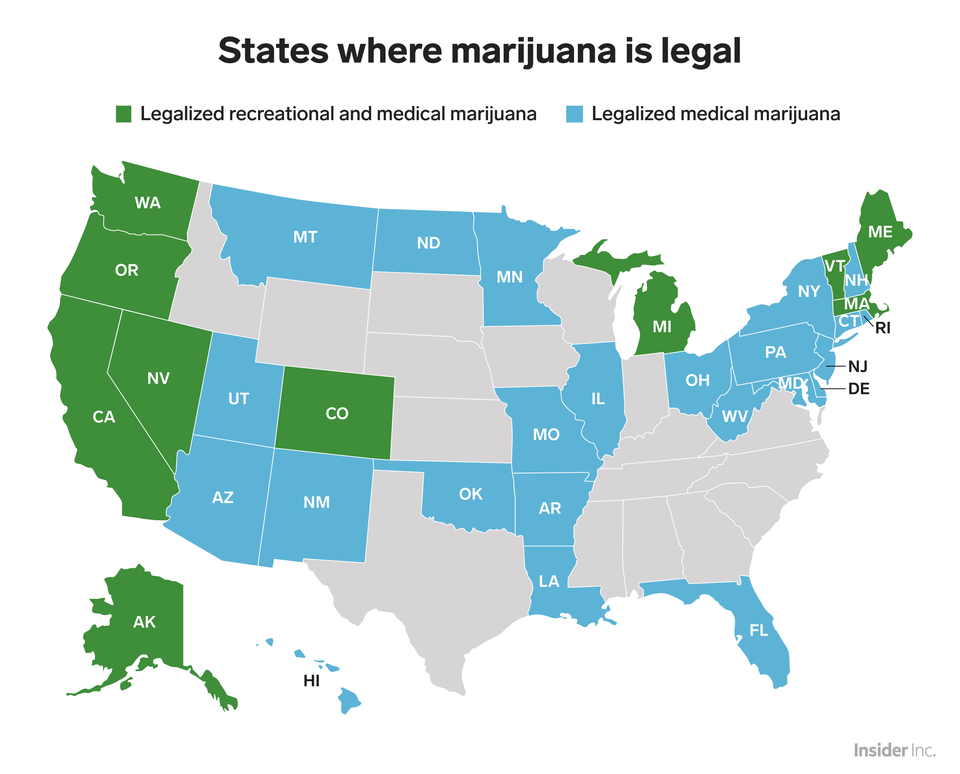

Peace Naturals cannabis oil, owned by the Cronos Group. It’s hard to imagine anything that has ever moved through politics faster than the legalization of medical and recreational marijuana, except perhaps the repeal of prohibition almost a century ago. In the past few months, one more state (Michigan) legalized recreational use in the U.S., bringing the total to 10. 33 states now allow medical use of marijuana. I’m seeing CBD Oil for sale over the counter in very conservative states, where being caught with a joint a few years ago could have brought a world of trouble. Customers claim CBD Oil cures virtually everything, and worry about how to sneak it into their luggage as they cross state and country lines.  The cannabis industry is attracting very established executives and politicians into their C-suite. Tilray’s new international advisory board includes Governor Howard Dean (Vermont), Joschka Fischer (vice chancellor of Germany), along with senior government officials from Canada, Portugal, Australia and New Zealand. Aphria’s new independent board chairman is Ira Simon, the founder and former CEO and chairman of Hain Celestial. Cronos was just infused with a $2.4 billion investment from Altria (the owner of Marlboro and Philip Morris), giving Altria 45% ownership, with the possibility of taking ownership up to 55% with warrants. Constellation Brands (the owner of Corona, Robert Mondavi and other beer, wine, vodka and whiskey) invested $4 billion in Canopy Growth. MedMen’s board includes former LA Mayor Antonio Villaraigosa. Andrew Modlin, MedMen’s co-founder & President, received the Emerging Leaders Award in 2017 from the American Marketing Association. In short, cannabis is mainstream. Companies are making legitimate deals with Colombian farmers for supply. Most of the publicly traded cannabis companies are Canadian based, with greenhouse grow farms. Gone are the days of gangster movies about weed smuggling. Your grandmother might have even tried one of the products, particularly the CBD Oil. So, it won’t surprise you to learn that cannabis companies are exploding in sales growth. Aurora Cannabis just announced that their revenue for the 2nd quarter (of 2019 fiscal year) will be $50-$55 million, compared to $11.7 million a year ago. This is 68% higher than 1Q 2019 and 327% higher year over year. The company will release their earnings report before the market opens on Feb. 11, 2019. Aphria’s revenue growth exploded with 255% ascension in the most recent quarter. Cronos Group’s revenue rocketed up 186%. Tilray’s growth was an impressive 85.8%. Canopy Growth is the largest and perhaps most well known of the publicly traded cannabis companies. However, Canopy’s year over year revenue growth was only 33% in the last quarter. All of these companies enjoy popularity among investors, trading millions of shares daily, and are listed in the NYSE or NASDAQ stock exchanges. Be careful of cannabis companies that are not traded on the big boards, have very thin trading activity and don’t have governance and financial information that is easily accessible. (MedMen is still trading off the boards in the U.S. with the symbol: MMNFF, and on the Canadian Securities Exchange in Canada, with the symbol: MMEN, putting this early stage company at higher risk than the other companies mentioned in this blog.) The challenge of all of these companies is scaling quickly enough to meet demand, without compromising quality. With the experienced executives that are joining up the companies I mentioned here, these companies should have the talent and experience in place to execute, escalate and start vertically integrating their supply chain. So, when you’re looking for cannabis companies to invest in, be sure to look into who is running the company, along with the board and their qualifications, rather than just blindly investing. There are still plenty of scams out there, and opportunists looking to cash in on the trend. Penny pot stock marketers are still pushing pump and dump schemes, where insiders sell en masse as soon as the ruse attracts enough naïve investors. A few more points:

Full disclosure: I own shares in many of the cannabis companies mentioned in this blog, including Cronos, Aurora and MedMen. Are You Interested in Learning How to Invest in Hot Industries, Like Cannabis? Join No. 1 stock picker Natalie Pace at a 3-day Investor Educational Retreat. Learn the ABCs of Money that we all should have received in high school. Only 2 seats remain available at the Valentine’s Retreat in Santa Monica. Make sure that your financial house is secure enough to withstand the economic storms that are on the horizon. A diversified, hot plan that is annually rebalanced and underweights the over-leveraged companies and municipalities is your best defense against a market downturn. Sadly, most people are not diversified, are heavily invested in companies that are drowning in debt, and are still using Buy and Hope, instead of Annual Rebalancing and Modern Portfolio Theory. (Many broker-salesmen say they are using MPT; few are, however.) That’s why your first and best step is to Know What You Own. If you’re interested in an unbiased 2nd opinion, which includes a report of what you own, outlining areas of strength and weakness in your current plan, alongside a personalized sample nest egg pie chart, email [email protected].

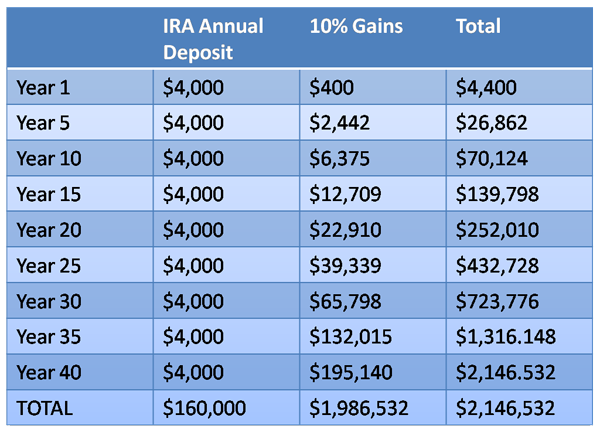

Other Blogs of Interest Canada Legalizes Marijuana. Penny Pot Stock Scams. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. Thanksgiving 2018 Stocks Losses. Black Friday Sales. Get a 2nd Opinion on Your Current Investing Strategy. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  Most of us rely upon financial advisors, who dispense their counsel freely, for what we believe is good financial advice on budgeting, investing and our retirement. However, as a study from the Rand Corporation discovered, that can be a very bad bet – particularly in market downturns. In Rand’s paper, “Impacts of Conflicts of Interest in the Financial Services Industry,” the researchers wrote clearly, “We find empirical evidence suggesting that financial advisors act opportunistically to the detriment of their clients.” The Financial Planning Commission (the industry itself) admitted the problem after the research was published, writing, “The current regulatory framework allows Advisors Interests to be misaligned with Retirement Investors interests… There are significant loopholes that allow for the sale of products that may not be in the best interest of the Retirement Investors.” So, what should you do about it? The first thing is to understand how the ruse works. Below are a few real-world examples of the high cost of free advice, and how the sales pitch is deceiving. 1. Bloggers. Bloggers with little experience and no proven track record, including broker/salesmen, are able to write on popular financial websites, which is why you must grade your guru before reading anything she writes. I recently came across a blogger on a popular platform who advised that the markets return after recessions 100% of the time. Therefore people should invest and ride out recessions, rather than letting “short-term pain impact your long-term gain,” he said. This is a popular sales line in recessions. What this blogger isn’t saying is that when you lose more than half, it takes more than a decade to crawl back to even. A 10% gain on a million is $100,000, whereas a 10% gain on $450,000 is $45,000 – taking 12 years to come back. Most investors who waited out the Great Recession are still underwater. That is why the better plan is to always keep at least a percentage equal to your age safe. A 25-year old can afford to lose more than half and then crawl back to even by the age of 35. A 65-year old might lose other assets in that same scenario, in addition to losing half of their retirement. When your assets implode, so does your credit score and your ability to pay bills. Sadly, due to the devastating losses in the last two recessions, many people had to postpone retirement. The blogger neglected to mention that. 2. Broker/Salesman. Many broker-dealers are paid commissions on the products they sell. The higher the commission, the higher the risk of the product. That means the broker/salesman earns more by putting you at greater risk, creating a conflict of interest between protecting you and paying their own rent. However, the client rarely knows what those back-door commissions are because when a client asks about fees, the broker discloses the costs that the client bears. She doesn’t necessarily reveal the commissions that are paid on the back-end. It is difficult to clearly understand how this works, how high the commissions are and the true risk of the product, if you are relying upon the “free” advice of the broker/salesman for your information. Another detail most broker/salesmen don’t disclose is that, while his percentage appears to be low, most clients are underperforming the markets, due to the fees. And that is in the good times bull markets. In recessions, clients who are not properly protected are losing more than half. (See the Recessions section below for additional information.) An easy way to see this is to ask the broker/salesmen for a chart of their portfolio returns compared to the S&P500 for the last ten and 15 years. That way you’ll see the bull market (probably underperforming) and the Great Recession (when most investors lost 55%). 3. Life Insurance Salesman. Insurance pays great commissions to their salesmen. However, most people pay into this product and never reap the gains. (If they did win big, insurance companies would be out of business.) The returns included in calculations are often much higher than reality, and the way the literature is written, most people don’t realize that their fees will increase dramatically, and their benefits will be slashed, as they age. Depositing that money into a tax-protected retirement account offers many benefits that life insurance doesn’t, including the most important benefit – that money is yours to keep no matter what. It doesn’t go away if you can’t make a payment. In retirement, instead of you having to pay life insurance (at a much higher price), your retirement pays you. That’s key because when you retire, your costs are typically higher (particularly your health costs) and your income is typically lower than when you are an income-earner. There comes a day when the choice is to eat, receive medical care, keep your home or make your insurance payment. Sadly, I knew one couple that chose to put all of the husband’s Social Security payments back into the insurance plan, where the million-dollar policy had been cut to $250,000, and the premiums had soared to $20,000/year. The husband is still alive, at 92. His uninsured wife passed away at age 66. Financial stress was one of the things that deteriorated her health. (They paid $700,000 over a 35-year period from age 65 to 90 to keep that $250,000 policy alive.) Another 80-year old couple was paying $40,000/annually for life insurance. They were sold into life insurance as a strategy for their kids to be able to pay the taxes on their millions in real estate and art assets. Last year, the couple went into bankruptcy. They lost their real estate and art assets, and are living with their kids on the small amount of money (less than $150,000 each) that they were able to salvage in the restructuring. When you are diligent about putting 10% of your income into tax-protected retirement accounts, and investing it, you can have millions built up by the time you retire.  Chart by Natalie Pace. (c) 2006. All rights reserved. 4. Real Estate. (REITs). Private placement real estate investment trusts have become popular products for broker/salesmen because they pay very high commissions. One retiree had her entire retirement of $350,000 put into REITs that were very high risk, as all of them had been cash negative for years. As interest rates rise, the risk of these products becomes astronomical. The retiree thinks she owns real estate. She doesn’t realize that she owns stock in distressed companies that are borrowing from her at 7% because they can no longer borrow from a bank at any price. The broker/salesman made 7% commission, or almost $25,000, on the transaction. The client has all of her $350,000 at risk, with provisions that limit her ability to get her money back. 5. Annuities. Annuities are one of the few investment products where your principal decreases the moment you buy in. They call it a surrender fee. Many times the annuity is linked to an index, which means that if stocks go down, you could actually lose money. It is also a product with no backstop. If the company you purchase the annuity from gets into trouble, you’re likely to receive pennies on the dollar back. This is key because if the U.S. had not bailed out AIG in 2008, more than 50 million insurance plans and annuities would have evanesced. AIG is back to being the biggest annuity provider. (Multiple companies with different names are owned by AIG). Losses are not a thing of the past for AIG. Last year, AIG lost another $6 billion. In the most recent quarter, the losses were $1.3 billion. If your company is privately held, it may be difficult to access their financials. However, fiscal health is an important factor to consider, if you are placing your future in the company’s hands. 6. The Apocalypse Portfolio. Sometimes the financial advisor will try to get fancy, particularly when they have a fearful client, selling their client into a high-risk strategy and calling it safe. This strategy might be overweighting into bonds (which are vulnerable today) or into oil and gold. Keeping a percentage equal to your age safe, and overweighting safe this late in the business cycle, is a good idea. However, you need to know what’s safe at a time when bonds are highly leveraged and vulnerable to capital loss. The right strategy for your at-risk side isn’t all-in on gold or oil either. If you believe those industries will soar going forward (or any other industry for that matter), then you can have up to 4 hot slices in your diversified plan. It’s never a good idea to go all in (or all out) on a strategy. Market timing is almost always a money loser, because most people are selling low and buying high when they are investing on fear or blind faith. 7. Recessions. The last two recessions have looked more like depressions. Most people lost more than half in the Great Recession and more than 3/4ths in the Dot Com Recession. As I indicated above with the math, when you lose more than half it takes a decade or more to crawl back to even. With these catastrophic recessions occurring every 8-10 years, most people are still underwater.

Buy and Hope worked before 2000. Since 2000, however, Modern Portfolio Theory with annual rebalancing has been the only plan to save the day. Today is a different world, with very high debt, an aging demographic and very low GDP growth. The economy has been fueled by low interest rates, which create bubbles. When bubbles pop, they are devastating, which is why the last two recessions, and likely the next one, have wiped out investors. Many brokers say they use Modern Portfolio Theory, and then sell you into whatever plan their brokerage offers, or pays the highest back-end commissions. As the Rand Corporation noted in their study, and yes it bears repeating, “We find empirical evidence suggesting that financial advisors act opportunistically to the detriment of their clients.” That is why you have to be the Boss of your Money, particularly this late in the business cycle (10 years), when economists have now pegged the likelihood of a recession in 2019 at 25%. Wisdom is the cure. What Should You Do to Protect Yourself From More Wall Street Weakness? A diversified, hot plan that is annually rebalanced and underweights the over-leveraged companies and municipalities is your best defense against a market downturn. Sadly, most people are not diversified, are heavily invested in companies that are drowning in debt, and are still using Buy and Hope, instead of Annual Rebalancing and Modern Portfolio Theory. (Many broker-salesmen say they are using MPT; few are, however.) That’s why your first and best step is to Know What You Own. If you’re interested in an unbiased 2nd opinion, which includes a report of what you own, outlining areas of strength and weakness in your current plan, alongside a personalized sample nest egg pie chart, email [email protected]. Happy New Year! Making sure that your financial house is secure enough to withstand the economic storms that are on the horizon will help your 2019 and beyond to be more enjoyable. You can learn the ABCs of Money that we all should have received in high school at one of my Investor Educational Retreats. Only 2 seats remain available at the Valentine’s Retreat in Santa Monica. Receive a discount on your private coaching package (and 2nd opinion), when you register for a retreat. Clients have already saved hundreds of thousands of dollars with the second opinion!

Other Blogs of Interest

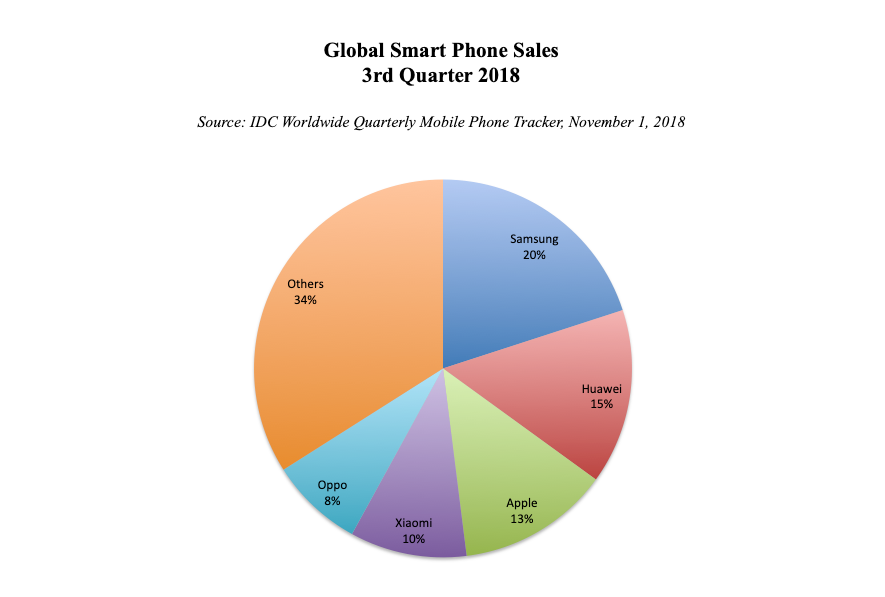

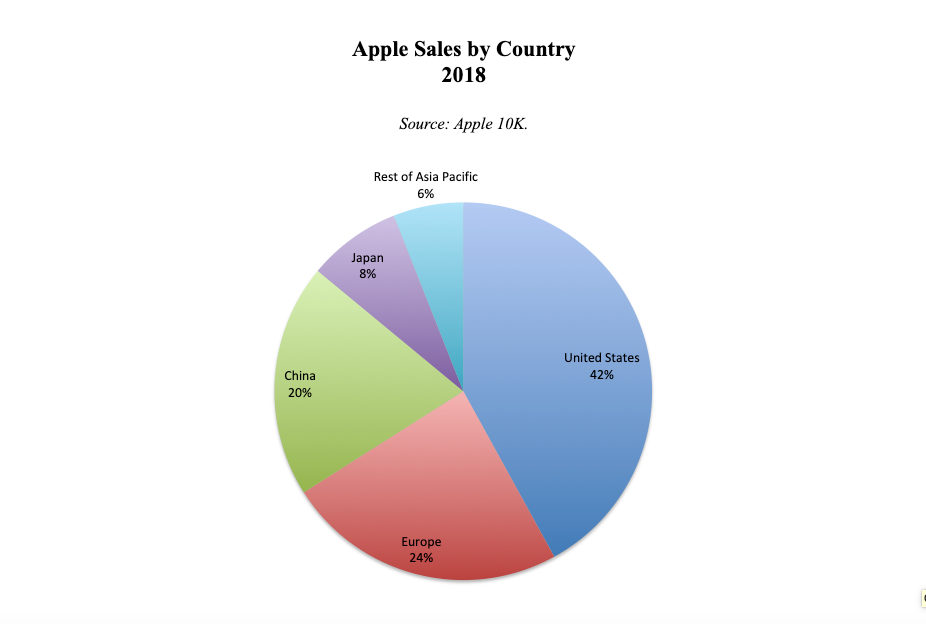

Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. Thanksgiving 2018 Stocks Losses. Black Friday Sales. Get a 2nd Opinion on Your Current Investing Strategy. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  President Donald J. Trump and CEO of Apple Tim Cook in the Oval Office at the White House. April 25, 2018. In the background: John Bolton, the National Security Advisor. Official White House photo. Public domain. Wiki Commons. Used with permission. This blog was amended on January 19, 2019. See the end of the blog for details. Yesterday, Apple revised its sales outlook for the 4th quarter (fiscal 1st quarter), claiming revenue will drop in at $84 billion, down from its previous estimate of $89-$93 billion. That caused a fright among investors, and Dow futures are down over 300 points as I write this blog (from Rome, Italy). Put into context, that would represent a drop in sales of 5% year over year. Investors aren't accustomed to weakness in the 1st company to attain trillion dollar value. (The current market value of Apple is $741.73 billion. Share price has been sliding since Oct. 2, 2018.) Tim Cook said that the reason sales will be down by $5-9 billion is basically disappointing iPhone sales in China. He blamed the economic slowdown in China for lower sales, stating on CNBC that “It’s clear that the economy began to slow [in China] during the 2nd half… Trade tensions put additional pressure on their economy.” Traffic in Chinese Apple stores and their channel stores is down as well. While Tim Cook is right about a slowdown in China’s economic growth (to 6.1% predicted in 2019 by Fitch Ratings), that’s not the real reason that Apple sales are down in the world’s largest economy (China). According to IDC, the slowdown in smart phone sales has been going on since the 4th quarter of 2017. The reasons? “Market saturation, increased smartphone penetration rates, and climbing Average Selling Prices,” according to Anthony Scarsella, the research manager with IDC’s Worldwide Quarterly Smart Phone Tracker. The slow down is concentrated in Samsung and Apple, the chief contributors to the pricing problem. The lower-cost Chinese manufacturers Huawei and Xiaomi saw outstanding sales growth year over year. In fact, the 2nd quarter of 2018 welcomed a new leader to the Top 2 in global Smart Phone sales, knocking Apple down to #3. Samsung and Apple have dominated the #1 and #2 position in smart phone sales for a decade. However, Huawei outsold Apple to become the #2 smart phone seller worldwide, with sales of 54.2 million units and 15.8% market share in the 2nd quarter (source: IDC). There are reports that Huawei’s smart phone sales topped 200 million units in 2018. (The final 2018 report from IDC should be available at the end of January.) Here are the most recent numbers from Q3 2018.   So, why is Huawei more important than ASP, market saturation and China’s slowing economic growth? Cook is not publicly acknowledging the elephant in the room, although he is smart enough to consider this privately. Huawei is beating Apple in global smart phone sales. The arrest of the Huawei CFO and vice chairwoman Meng Wanzhou is viewed in a negative light – not just by China. Chinese media, other Asian media and many Weibo updates, called the arrest “kidnapping,” referring to the U.S. as a rogue nation. Imagine if Tim Cook were in jail awaiting extradition to China for aiding Tibet in some way. Trade wars don’t just slow economic growth. (The tariffs have actually resulted in a much larger trade deficit with China.) They also tarnish brands. While many Chinese consumers might love their Apple iPhones enough to stay loyal, that becomes increasingly problematic as the U.S. trade policy and the arrest of Huawei’s CFO make headlines in the country. When citizens have to choose between patriotism and a product, it is likely to be the product that suffers. 20% of Apple’s sales come from China, with over 1/3 from Asia Pacific.  Tim Cook has his work cut out for him. What can he do to compete with the harsh headlines of a U.S./China trade war and the arrest of a major Chinese competitor’s heir apparent? He must find a way to keep Apple beloved and separate from the actions of the current Administration, while also innovating and reconsidering his aggressive pricing. Will he cut a deal with an Asian carrier, to make his smart phone products more affordable (as he did with AT&T when iPhone first launched). Watch for those headlines to understand how Apple will fare in 2019, which may not be featured as predominantly, or covered as widely, as yesterday’s earnings miss was. *The original blog stated in error that sales growth year over year would be positive. What Should You Do to Protect Yourself From More Wall Street Weakness? A diversified, hot plan that is annually rebalanced and underweights the over-leveraged companies and municipalities is your best defense against a market downturn. Sadly, most people are not diversified, are heavily invested in companies that are drowning in debt, and are still using Buy and Hope, instead of Annual Rebalancing and Modern Portfolio Theory. (Many broker-salesmen say they are using MPT; few are, however.) That’s why your first and best step is to Know What You Own. If you’re interested in an unbiased 2nd opinion, which includes a report of what you own, outlining areas of strength and weakness in your current plan, email [email protected]. Happy New Year! Making sure that your financial house is secure enough to withstand the economic storms that are raging will help your 2019 to be more enjoyable. You can learn the ABCs of Money that we all should have received in high school at one of my Investor Educational Retreats. Only 2 seats remain available at the Valentine’s Retreat in Santa Monica. Receive a discount on your private coaching package (and 2nd opinion), when you register for a retreat.

Other Blogs of Interest

2019 Crystal Ball 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. Thanksgiving 2018 Stocks Losses. Black Friday Sales. Get a 2nd Opinion on Your Current Investing Strategy. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. |

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed