Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

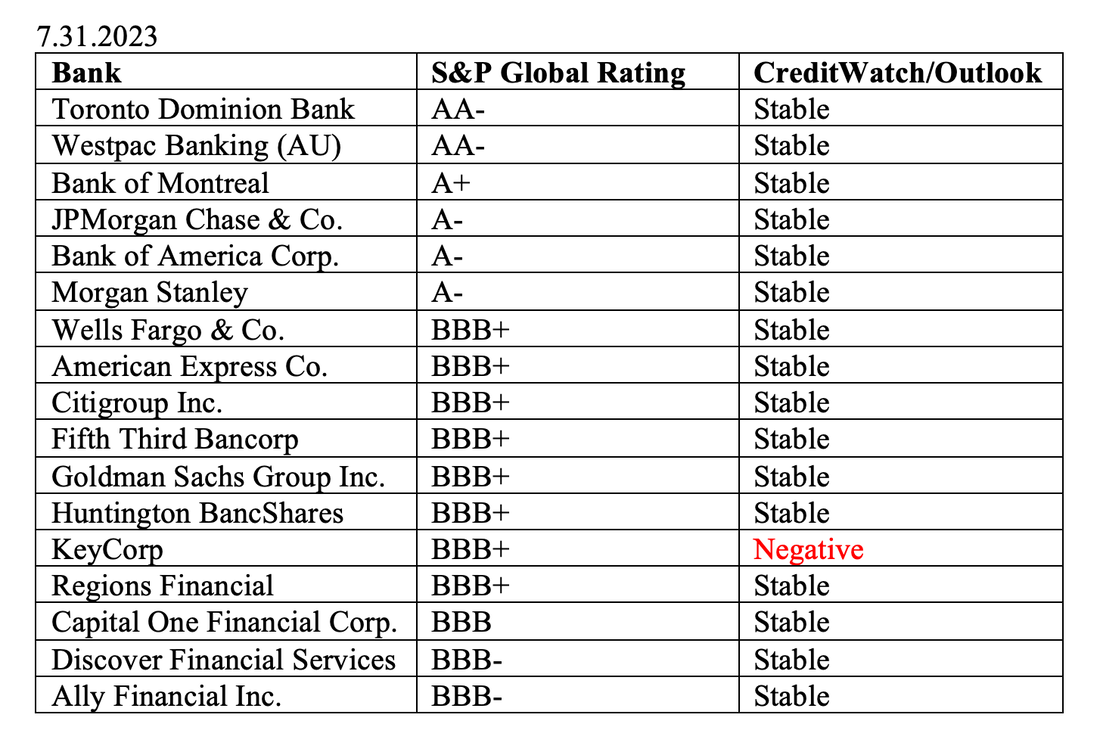

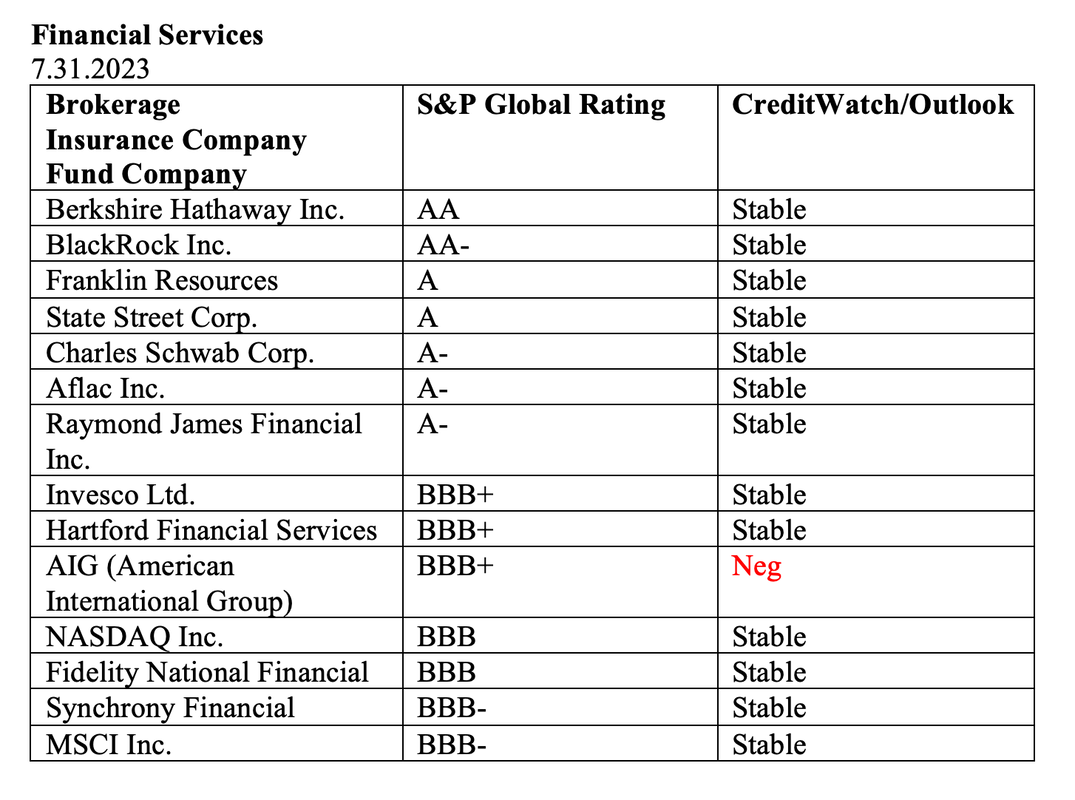

Bank of America Has $100 Billion Paper Loss on Bonds. Upstart Holdings Revenue Drops by 63%. Is the banking crisis really over? (No, the Heartland Tri-State Bank of Kansas failed last Thursday, on July 28, 2023.) Why does this matter to you? What can/should you do about it? Here are the things we’ll cover. Bond Losses Affect All of Us Upstart Holdings PacWest, Heartland Tri-State Bank and Community Banking Faith and Creditworthiness Is Your Bank Close to Becoming a Junk Bond? A Very High-Profile Credit Downgrade Be Careful of Outstanding Earnings Reports in the Financial Industry And here is additional information on each point. Bond Losses Affect All of Us Even if we are not a Bank of America customer or live in another country, the bond losses are important to know about and factor into our own wealth plans. (If you are a Bank of America client, look at the credit scores and leverage of the other banks before switching.) Why? Because most of us have bond losses in our own retirement plan (even those of us who live outside of the U.S.). The safe side of our wealth plan, where bonds traditionally are placed, is not supposed to lose money. That puts all of us at greater risk in the next recession, if we don’t take steps to protect our wealth now.  Our team has been warning for over a decade that we weren’t being paid to take on the risk of long-term bonds. Many of these holdings have terms of 35 years or more, meaning we don’t get our money back until well beyond our own expiry date. That’s why it’s vital to understand exactly what we own and why, not just on the at-risk, stock/equity/fund side, but also on the “safe” side of our wealth plan. (Join us at our Oct. 7-9, 2023 Investor Empowerment Retreat or consider receiving an unbiased 2nd opinion from me personally through our private coaching. Email [email protected] for pricing and information.) Upstart Holdings With regard to the Upstart Holdings challenges, many people are still relying upon Reddit, social media ads, emails, get rich quick schemes and hot tips from friends and family – hoping to “win” some money during the current Wall Street rally. Chasing gains, hot tips, Hail Mary’s and other desperate acts are more likely to lose money than to make us millionaires. Upstart Holdings’ core business model of personal and auto loans isn’t working well in the current interest rate environment. Many people don’t want to borrow at the current interest rates, while others no longer qualify. The company’s revenues are down -63% year over year. The net loss in the most recent quarter was $129 million, and Upstart has been in the red for over a year now. Upstart Holdings was a meme stock whose price soared to $400/share in October of 2021, only to crash to a low of $12 merely a year later. It’s not surprising that someone is bragging about earning some gains on Reddit, perhaps in the hopes of generating another pump-and-dump opportunity. If you have holdings in this or any other meme stock or individual company that has lost so much, you might consider attending our retreat and learning how to invest in a time-proven strategy, rather than relying upon Shoot the Moon hopes that are thin on fundamentals, and are riding high on hot air. YOLOs can be fun when they work, but they shouldn’t be the entire plan. HODL is a last-century strategy that doesn’t work on today’s Wall Street rollercoaster. PacWest, Heartland Tri-State Bank and Community Banking Community banks are in distress. As the National Association of Realtors’ chief economist, Lawrence Yun, wrote on May 3, 2023, “The fast rate hikes by the Fed have upended the balance sheets of many small regional banks. They are becoming zombie-like banks, unable to lend even to good businesses as they are more concerned with balance sheet shuffling for survival.” Bond losses, uninsured deposits, rate hikes and the recent bank failures have anyone with cash feeling a bit jittery. So far, we’ve only seen four banks fail in 2023, with the Heartland Tri-State Bank of Kansas being the most recent (on 7.28.2023). Headlines are so focused on Wall Street gains that you might not have even heard there was another bank failure last week. PacWest took a significant hit in their most recent earnings report, with their revenue down by -84% year over here and a net loss of $207 million. The bank lost $1.2 billion in the 1st quarter of 2023, and has been cash negative for more than a year. They just completed a merger with Banc of California to strengthen their balance sheet, and are trying to reassure depositors that 81% of the money is FDIC-insured. However, that still leaves $5.3 billion uninsured. It’s important for all cash depositors to realize that the fine print is key. There’s a loophole in the coverage for all non-banks, including brokerages that promise FDIC-insurance. (Click to learn more about that.) The special exemption that was made for the Silicon Valley Bank uninsured depositors is unlikely to be repeated. (There was no mention of non-insured depositors being rescued in the two most recent bank failures.) The FDIC fine print hasn’t changed. Faith and Creditworthiness While 2Q earnings reports generally looked pretty good in the big banks, it’s important to understand that a lot of that relies upon financial engineering and government support. There are policies to help banks that have exposure to commercial real estate, a Federal Reserve facility that erases bond losses for a year (the Bank Term Funding Program), and a Homeowners Assistance Fund that saved 318,000 homes from foreclosure (with a price tag of $3.7 billion). In other words, government bailouts, not financial restraint or conservative underwriting practices, are largely responsible for the slowdown of bank failures. The impressive, recent rally in financial stocks has a lot of phantoms in the wings, including a spike in corporate bankruptcies. The banking industry is based upon a presumption of faith. When faith surrenders to fear, you get a run on the banks, which could cause a bank to fold, since banks have a small fraction of depositors’ cash on hand. (Watch It’s a Wonderful Life for a good tutorial on this.) Is Your Bank Close to Becoming a Junk Bond? So how much faith should we have in US banks? And are there banks in other countries that are more creditworthy? In February of this year, before the bank failures (and for years in my books and at our retreats), we warned that we were underweighting the U.S. financial industry. Over half of the S&P500 is at or near junk bond status, including a lot of U.S. banks, insurance companies and brokerages.