Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

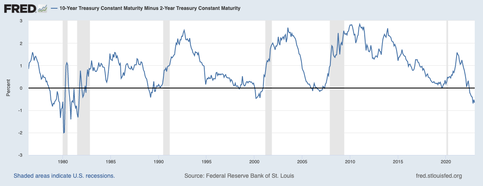

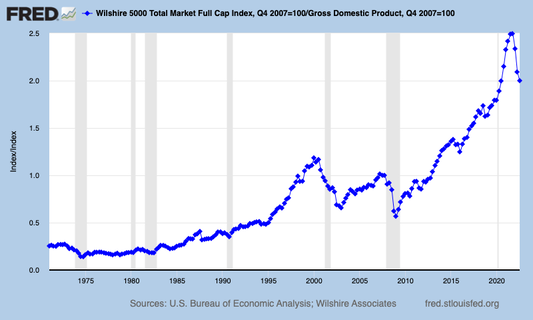

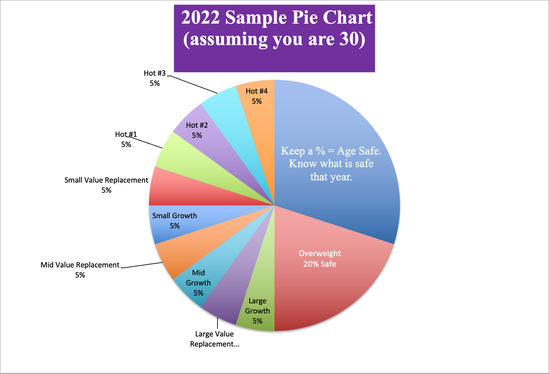

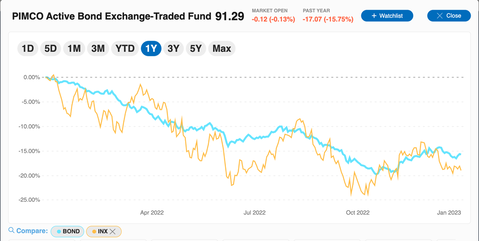

Natalie Pace photo by Sunil Rampersad. Crystal Ball 2023 Do you have too much exposure to stocks? Crypto? Gold/silver? Bonds? What is likely to happen in 2023, and what's your best plan? In 2022: · The S&P500 dropped -19.44% · The NASDAQ Composite Index sank -33% · Tesla is down -72% over the high set in Nov. 2021 · Bitcoin’s Crypto Winter is frozen with -76% losses from its Nov. 2021 high of $69,000 · Long-term bonds are losing value, negative-yielding and becoming less liquid as interest rates rise. The yield curve is negative again, which is 100% correlated with recessions.  Is there any bright spot or area of safety? What's the best strategy for 2023? Will it be as bad as 2022, or will the recovery begin? See below for our analysis of stocks, bonds, crypto, gold, silver, copper and real estate, and your best strategy for each. Stocks 2022 was not a very good year for stocks. 2023 is not predicted to be any better. Even with the pullback of 2022, many stocks are still overvalued.  With high valuations and weak expectations, I would take a defensive strategy with stocks this year. As you can see in the sample pie chart below, we are overweighting an additional 20% safe.  Sample Nest Egg Pie Chart using the Natalie Pace time-proven 21st Century system. Visit NataliePace.com to learn more. Email [email protected]. 2023 could start off better than it ends. According to the FOMC minutes from Dec. 15, 2022, the 4th quarter 2022 GDP was increasing at a “modest pace,” after posting “strong” 3.2% growth in the 3rd quarter. Some analysts believe that the growth could be even higher than the 3rd quarter. At any rate, the advance results will be released by the Bureau of Economic Analysis on Jan. 26, 2023 at 8:30 am ET. Any positive results might be greeted with a rally, and a strong showing could light stocks on fire, at least temporarily. There are a few flies in the ointment, including the Debt Ceiling, which will have to be addressed with a divided House of Representatives and White House, likely in February or March. That hasn’t gone smoothly in the past. In 2011, when the raise was put off to the last second before a default on U.S. debt (the first ever), S&P Global downgraded the U.S. credit from AAA to AA+. Stocks dropped. Gold and silver soared to an all-time high. Bonds The mantra for bonds is to keep the terms short and the creditworthiness high. The Fed Fund rate is predicted to rise at least another 70 basis points in 2023, without any pullbacks. That is good for fixed income investors who have been on the sidelines and very bad for those who have been sold into long-term bonds of questionable quality. As interest rates rise, bond values go down. As you can see from the chart below, bonds declined in value almost as much as stocks last year.  Source: MSN.com. (c) Microsoft. Used with permission. We’re still in a sweet spot where there is more liquidity in the bond market. So, getting rid of a long-term low-yield, high-risk bond might still be possible. It’s a good idea to understand whether or not you can sell it at par, or if you’ll have to take a haircut in the offloading before you decide the course of action that’s right for you. You might start by evaluating your current bond to see if they meet the terms of the bond mantra. (Most bond funds do not.) What kind of short-term creditworthy bonds are available? The Treasury I savings bond is still offering a 6.89% interest rate (through April 30, 2023). The interest rate resets on May 1, 2023. If inflation is still high, the new rate will still be in the high-yield range, with fairly low risk. Of course, you are limited to $10,000 per person per year on the series I savings bond. So, this is not something that’s going to be the strategy for most of your safe side. (Although don’t underestimate the value of slow, steady, compounding. Peter Thiel reportedly has over $4 billion in a Roth IRA.) Short-term Treasury bills and FRNs are offering a higher interest rate than long-term. The 1-year Treasury Bill is at 4.71, while the 30-year is offering about 3.81. Due to leverage, risk and rising interest rates, again, the mantra is: keep the terms short and the creditworthiness high. Having a laddering approach is a great idea too – something I explain in further detail below. Opportunities for other types of income-producing hard assets might start presenting themselves in the next 1 to 2 years. So having access to liquidity remains important. Crypto Crypto Winters are harsh and long. After the boom in Dec. 2017, when Bitcoin jumped to $20,000, Bitcoin plunged and spent most of the next three years stuck in the $3,000 to $8000 price range. Because of the number of bankruptcies that we have seen with crypto coins, exchanges and companies, there is still likely to be further fallout and contagion – as the ripple effect takes more companies down. Additionally, those crypto exchanges and brokerages that promise FDIC insurance on the cash portion of your account are much higher risk than most people realize. FDIC insurance does not come in to play if a non-bank (like a brokerage or exchange) declares bankruptcy. Learn more in my blog on FDIC-Insured Brokerage Accounts. . Gold and Silver Gold and silver have been suffering from the popularity of cryptocurrency as the preferred safe haven for the younger generation. Millennials and Gen Z who are worried that their dollars will become worthless generally prefer digital exchange over bullion. However, now that the Stimmy checks savings have been burned up, and many cryptocoins are trading at 1/3 or less of the value they held in November 2021, crypto is unlikely to put up much of a fight in 2023. Therefore, investors who are seeking a safe haven will likely turn to gold and silver. We’ve already seen a quiet rally in silver, which is up about 32% off of its low in 2022. Because silver is still trading at half of its high, whereas gold is only down about 12% from its $2089 high, silver has a great deal more upside potential than gold. Learn more in my Silver’s Quiet Rally blog. Copper Copper has been called the “new oil” by Goldman Sachs. It is in high demand due to the commitment of the world to implement cleaner energy strategies. Everything from electric cars and solar panels to smart grids require a lot of copper. Copper is hot, even though prices have slipped a bit from their very elevated prices in 2021.  Source: Kitco Solid copper prices will benefit countries like Australia, Peru and Chile, which are rich in natural resources. Chile is the #1 supplier of copper to the world, while Peru is the 2nd. These countries are also paying a good dividend, and are worth looking at adding to your portfolio. Although we hear a lot about developing world countries being in trouble with rising interest rates, Chile and Peru are not included in the swath. In the above chart, you’ll see that copper prices plunged in the early days of the pandemic. Even hot industries can get dragged down in a bear market. For that reason, this year’s mantra for equities is the stock layaway plan, which is outlined below. Stock Layaway Plan This is an old-school term that’s becoming more popular today as people need to put their big ticket spending on a monthly payment plan. So how does a stock layaway plan work? First of all, as I detail directly below, we want to overweight 20% safe before we decide how much we want to invest. Once we determine how much should be in each of our 10 slices, think about getting to that goal over the next year. In other words, if our slice should have another $24,000 to be full, just put in $2000 each month. Using the Stock Layaway plan, we will be buying more at a lower price, if stocks go down. If the share prices go up, then they will be filling up our slices for us. Of course, if we get to our goal before the end of the year because stocks have increased in value, then just stop buying. Overweight up to 20% Safe If you are not sure of what you owe now is the time to absolutely know what you have at risk, what you have safe, and what isn’t as safe as you might realize. (Be sure to watch my 2023 Crystal Ball videoconference for details on this.) We should always keep a percent equal to our age safe, i.e. not in stocks, mutual funds, equities, etc. Because of the risk of a recession, which many economists are predicting for the U.S. and many countries in Europe in 2023, we are overweighting an additional 20% safe in our sample pie charts. (When the U.S. sneezes, Canada catches a cold.) You can personalize your own pie chart using our free Web app. Simply email [email protected] with the subject line Free Web Apps to receive the link. As I mentioned above, even bonds can be tricky, negative-yielding and losing value in today’s world of rising interest rates. Diversify and Rebalance Rebalancing is a very important part of a successful investing strategy. When stocks go down, you want to buy more at a lower price. When stocks go up, you want to capture your gains, so that they don’t evanesce in the next recession. You might think this sounds like a lot of work. However, it’s actually easy as a pie chart. You should rebalance once, twice or three times a year. If you’re not doing this, you are riding a Wall Street rollercoaster, and are at risk of losing up to half of your wealth. It then takes quite a while to crawl back to even – 8 to 15 years. That’s a wealth roller coaster with severe consequences for your FICO score and future, which can be prevented by properly protecting and diversifying your retirement plan and assets now. Email [email protected] if you’d like to know exactly what you own, and how to get better protected and diversified. Bond Laddering Strategy A bond laddering strategy is similar to the stock layaway plan. Rather than putting all of your “safe” money in a bond or CD, have a plan that cuts up what you want to invest in quarterly chunks. If you want to invest $100,000 in short-term Treasury bills, think about doing $25,000 every 3 months. That way as interest rates rise, you are benefiting from the higher yield. You are also keeping liquidity, so that if opportunities to deploy your capital into other safe, income-producing assets present themselves, you have the cash on hand to take advantage of the opportunity. Adhere to the mantra: keep the terms short and the creditworthiness high. Banks with the lowest credit scores are offering the highest interest rates – which are still about 1.5% below what Treasury Bills are offering. Real Estate If we are a cash buyer and are willing to shop in the shadow inventory, there may be more opportunities for real estate in 2023 than we might realize. Prices have already fallen an average 11% since June of 2022. The areas that went up the highest are the ones that are falling the fastest. As Mortgage Bankers Association President and CEO Bob Broeksmit commented on Jan. 5, 2023, “We project lower rates and rising inventory levels as two positives for households wanting to buy a home in 2023.” There just aren’t that many qualified buyers who can afford to pay 6.4% mortgage interest rates, while real estate prices are so high. So, most people who really need to sell are going to have to discount their asking price. Now is a good time to do our research and to pull together our liquidity. Banks are not the only way to finance a purchase. The banks are going to charge us a lot more in interest than our parents might. (Prince William didn’t purchase Kensington Palace.) It might be a good idea for elderly investors to purchase a hard asset, like a home, that helps to keep the money in the family (and stops making the landlord rich), rather than having too much at risk in stocks or in long-term bonds. I will be hosting a Real Estate Master class on January 28, 2023 to outline the 8+ strategies to consider when purchasing a long-term, illiquid asset like a home or income-producing property. Whether we are ready to purchase our first home, ready to downsize, looking to move abroad, considering buying a 2nd home as an Airbnb rental or interested in purchasing your first apartment building, it is very important to adopt essential time-proven strategies to put us on the right side of the trade and to position us for a safe, cash-positive, stress-free experience. Register now for the lowest price. Anybody can attend. Email [email protected] with Real Estate Master Class in the subject line for additional information. Bottom Line There are finally opportunities to earn a little yield on the safe side. However, it is tricky. So it is important to check out my videoconference on the topic. Also, money market funds, long-term bonds, and even FDIC-insured cash at brokerages and exchanges can be tricky. I have a blog and videoconference on that topic as well. On the at risk side, while anything is possible, most economists are predicting a recession. Recessions drag the stock market down. Our best protection against a bear market is always just overweighting safe (and knowing what is truly safe in a Debt World). Market timing doesn’t work. Be sure to watch my Crystal Ball 2023 videoconference to get even more details than are presented in this blog. New Year, New You Financial Freedom Retreat If you're interested in learning 21st Century time-proven investing strategies for building and protecting your wealth, investing in renewable energy, saving thousands in your budget with smarter energy choices, and managing challenging economic times (from a No. 1 stock picker,) join us for our Jan. 20-22, 2023 Financial Freedom Retreat. Email [email protected] to learn more and to register. Click on the banner ad below to discover the 18+ strategies you'll learn and master, to get pricing information and to read testimonials Get the best price when you register with family and friends. Register now to access your free 4-part Protect Your Wealth Now webinar that will get you started immediately.  Join us for our New Year, New You Financial Freedom Retreat. Jan. 20-22, 2023. Email [email protected] to learn more. Register now to receive a free 4-part webinar (which you can access to protect your wealth now). Click for testimonials & details.  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Apple Podcast. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Tilray: The Constellation Brands of Cannabis New Year, New Healthier You Tesla's $644 Billion Fall From Mars Silver's Quiet Rally. Free Holiday Gift. Stocking Stuffers Under $10. Cash Burn & Inflation Toasted the Plant-Based Protein Companies Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Giving Tuesday Tips to Make Your Charitable Contribution a Triple Win. Is Your Pension Plan Stealing From You? The FTX Crypto Fall of a Billionaire (SBF). Crypto, Gold, Silver: Not So Safe Havens. Will Ted Lasso Save Christmas? 3Q will be Released This Thursday. Apple and the R Word. Yield is Back. But It's Tricky. The Real Reason Why OPEC Cut Oil Production. The Inflation Buster Budgeting and Investing Plan. No. Elon Musk Doesn't Live in a Boxabl. IRAs Offer More Freedom and Protection Than 401ks. Will There Be a Santa Rally 2022? What's Safe in a Debt World? Not Bonds. Will Your Favorite Chinese Company be Delisted? 75% of New Homeowners Have Buyer's Remorse Clean Energy Gets a Green Light from Congress. Fix Money Issues. Improve Your Relationships. 24% of House Sales Cancelled in the 2nd Quarter. 3 Things to Do Before July 28th. Recession Risks Rise + a Fairly Safe High-Yield Bond DAQO Doubles. Solar Shines. Which Company is Next in Line? Tesla Sales Disappoint. Asian EV Competition Heats Up. 10 Wealth Strategies of the Rich Copper Prices Plunge Colombia and Indonesia: Should You Invest? 10 Misleading Broker/Salesman Pitches. Why are Banks and Dividend Stocks Losing Money? ESG Investing: Missing the E. Bitcoin Crashes. Crypto, Gold and Stocks All Crash. The U.S. House Decriminalizes Cannabis Again. The Risk of Recession in 6 Charts. High Gas Prices How Will Russian Boycotts Effect U.S. Multinational Companies? Oil and Gas Trends During Wartime Russia Invades Ukraine. How Have Stocks Responded in Past Wars? 2022 Crystal Ball in Stocks, Real Estate, Crypto, Cannabis, Gold, Silver & More. Interview with the Chief Investment Strategist of Charles Schwab & Co., Inc. Stocks Enter a Correction Investor IQ Test Investor IQ Test Answers What's Safe in a Debt World? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed