Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

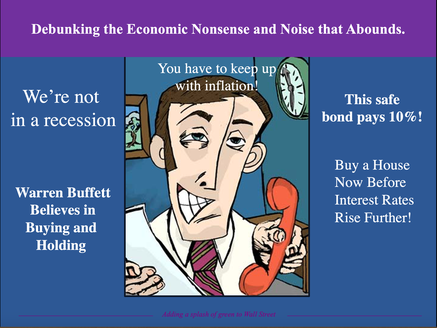

“Lies, Damn Lies and Statistics” Mark Twain. Debunking the economic nonsense and noise that abound. When the markets head south, in the initial days of a bear market, broker/salesmen scramble for their sales-speak playbook. Frantic calls pour in, and many are placated with some of the lines listed below – unless the plunge deepens and the losses become unbearable (which sadly has happened in three of the last three recessions). The pandemic recession was the blink of an eye and came roaring back, so many have forgotten that the stock market dropped almost 40% in just a month. Don’t cling to the hope that the next recession will act the same. In Federal Reserve Chairman Jerome Powell’s words (from a May 2022 interview), “The process of getting inflation down to 2% will include some pain.” So, with the S&P500 officially in a bear market, with losses since the high of -24%, should we be placated or should we get more defensive? Should we rely upon what we’re hearing in the mainstream media and from our financial advisor? What can protect Main Street investors from stock market losses? (There are 21st Century, time-proven solutions. Keep reading.) Below are 10 of the nonsense and noise (lies, damn lies and statistics) that are being bantered about in the media – even as the wealthiest investors continue to send the markets south, as they hunker down for the economic hurricane on the horizon. (Wall Street insiders are always the first to sell, and the first to buy back in at the bottom.) 10 Misleading and Potentially Catastrophic Sound Bites 1. People are being forced to sell low to take their mandatory distributions. 2. The statistics tell us we are not in a recession. 3. The economy is strong and corporations have a lot of cash. 4. We can move you to bonds to get you safer. 5. The Treasury Series I bonds are paying over 9%. 6. If you make changes now, you’ll just be selling low. 7. Turning off the news is a good idea. 8. Buy and Hold is a strategy that Warren Buffett uses. 9. You have to invest to keep up with inflation. 10. You should buy a house now before interest rates go up anymore. Here is a little more color on each one of these time-worn sales pitches, alongside a better, time-proven, 21st-century plan. 1. People are being forced to sell low to take their mandatory distributions. If you have to sell anything right now to take a mandatory distribution, you weren’t properly protected to begin with. Liquidity is an important part of any wealth strategy. 2. The statistics tell us we are not in a recession. Kevin O’Leary, Shark Tank’s Mr. Wonderful, came out with a video today saying that he doesn’t see a recession, even though that’s what a lot of economists and experts are forecasting. The economy contracted in the first quarter. Two consecutive quarters of economic decline marks the start of a recession. So, all eyes are on July 28, 2022, when the 2nd quarter GDP will be announced. If it is negative, we’re in a recession. Jerome Powell revealed that the economy picked up in the 2nd quarter in his press release on June 15, 2022. That could mean that we avert a recession for now, which is often what happens in the early stages of a bear market. However, it is also common for the stock market to start its decline well before the official recession announcement. The last two recessions are prime examples of that. The S&P500 had already dropped almost 40% before most people even knew we were in a pandemic in March of 2020. By the time the White House and Treasury Department admitted that we were in a deep recession in October 2008, the Dow Jones Industrial Average had already dropped about 45%. So, if you wait for the headline that we’re in a recession, it will be too late to protect your wealth. The bottom in the Great Recession was 55% losses. At that point many people thought we were in an Apocalypse because: * Lehman brothers got liquidated, * The entire banking system had to be billed out, * Mortgage banks and brokerages had to be rescued * Insurance companies, like AIG, were bailed out, and, * General Motors and Chrysler declared bankruptcy. Your plan should protect you from the recession before it arrives. Fortunately, that plan is easy-as-a-pie-chart with regular rebalancing. In fact, if your losses to date are more than 10%, that is a red flag that your current plan is not well-designed.  3. The economy is strong and corporations have a lot of cash. There is still a lot of cash in some of the corporations. Interest rates were near zero for a very long time, and corporations could borrow very cheaply, let their own credit score fall to the lowest rung of investment grade and receive no penalty for that kind of behavior. Now, we have over half of the S&P 500 at or near junk-bond status, including a lot of banks, brokerages and insurance companies. Saying that the corporations have a lot of cash, and ignoring the mountains of debt, is a perilously dangerous premise. I’ve mentioned that the U.S. economy contracted in the 1st quarter, and is one quarter away from being declared to be in a recession. 2022 full-year GDP keeps getting revised down, with the most recent estimate being 1.7%. The Feds never predict a recession before it arrives. And, of course, when it finally does arrive, it’s always due to some crazy circumstance like war, runaway inflation or some other uncontrollable event. Few ever admit that persistently low interest rates create asset bubbles and dangerously high leverage. Most just try to enjoy the ride as long as it lasts. 4. We can move you to bonds to get you safer. Bonds are illiquid and negative yielding. They are vulnerable to interest-rate risk, credit risk, duration risk, and they have no term premium. In a normal world, bonds would be a way to get safe because the Federal Reserve Board would be cutting interest rates, not jacking them up at lightning speed. (There is an inverse relationship between interest rates and bond values.) So, in today’s Debt World, you really need to know what’s safe. Otherwise, you could get locked into a long-term investment that borrows your money well beyond your own expiration date (those 30-45 year bonds), pays you very, very little and is impossible to liquidate. Prospective bond investors should receive a much better interest-rate with lower credit risk as early as next year, and certainly by 2024. If you jump in now, particularly into long-term bonds, you could be left holding the bag on an illiquid, negative-yielding, long-term, money-losing investment. 5. The Treasury Series I bonds are paying over 9%. The Series 1 savings bond is currently paying a 9.62% composite rate. That is astonishingly high in today’s world, where junk bonds are only paying 5%. However, that rate is only good for six months. The new composite rate will be announced on November 1. The fixed rate is zero on the bond. The other piece of the equation is attached to inflation, which is currently high. Inflation could still be high in November. However, if the FOMC‘s projections turn out to be accurate, next year inflation is going to drop by almost half. Since the fixed rate is zero on the bond, this could take the interest rate below 5%. If inflation falls further than that the interest-rate will be lower. If deflation occurs, then you could be getting no interest at all, while others are receiving a much higher rate in their savings accounts. You must hold the Series 1 savings bond for one year. If you exit before five years then you’re going to give up three months of your interest. This could still be worth it. However, it is unlikely that this bond will pay 9.62% for longer than the first six month period – unless inflation remains stubbornly high. 6. If you make changes now, you’ll just be selling low. The S&P earned about 27% last year, and is down about -24% already this year. So, we’ve given back most of the 2021 gains. However, we’ve been in a secular bull market since 2009. So, we’re still fairly high up the buy low, sell high continuum, particularly if we were well diversified and leaning into technology and growth over the past decade. If you are being told that you are selling low, it’s a sales tactic that’s intended to manipulate your emotions to keep you from making any changes. This is a hallmark of the last-century Buy & Hope strategy. What’s true? The sooner that we adopt a time-proven 21st Century strategy, the more of our wealth that we can protect. If we wait and the coming recession is as problematic as the Great Recession or the Dot Com Recession, we could be risking more than half of our wealth. This imposes serious financial hardship on our family. It wipes out our credit score. When we ride the Dow Jones Industrial Average all the way to its trough (which was 6547 on March 9, 2009), we then have to spend much of the bull market making up losses. (It took 15 years for the NASDAQ Composite Index to recover from the Dot Com Recession.) Sadly, after steep losses, many people are tempted to sell low and get out of everything altogether. Clinging to a money-losing proposition doesn’t work and neither does market timing. Having blind faith that someone else is protecting your wealth, when a simple 15-year performance chart could reveal that you are at risk of riding a Wall Street roller coaster much lower than it is right now, can be perilous to your fiscal health.

7. Turning off the news is a good idea. Turning off the noise is actually a good idea, but only if you have a time proven 21st-century plan in place. Acting on headlines almost always put you on the wrong side of the trade. If your plan is not properly protected and diversified, and you are not rebalancing it regularly to capture your gains, then whoever is telling you to stop watching the news is motivated to control you into adopting their plan. If things worsen, you’re not going to be able to stop worrying because you’ll quite clearly see the losses in your accounts. It’s much easier to manage your emotions when your plan protects you from extreme losses. 8. Buy and Hold is a strategy that Warren Buffett uses. Warren Buffett quite famously sold all of his General Electric stock just weeks before the company announced that they were cutting their dividend in half. (The stock dropped by half when the announcement was made.) Buffett used to live and die by Wells Fargo Bank stock. This is a holding that he didn’t get out of in time. He also quite famously bought into airlines at the low in the pandemic, only to sell them at a loss just a few weeks later. There’s a Wall Street saying, “Stick to your knitting.” Adopt a strategy that actually works in the 21st-century, and then don’t allow yourself to be distracted by the noise and nonsense that blusters nonstop. Warren Buffett, like other institutional investors, employs a team of analysts and managers who are active in their trading. When there’s a material event that changes the game or if they made the wrong call (as with the airlines), they are the first to get out. Fortunately, Main Street investors don’t have to jump into active trading. We just need to keep enough safe, be properly diversified and rebalance regularly (1-3 times a year). 9. You have to invest to keep up with inflation. This is a very common sales tactic. It’s used to get you to buy something – sometimes so that the broker/salesman makes an outstanding commission (6-7% or more, which equates to $6,000-$7,000 on every $100,000 invested). You’ll almost always be told that that investment is going to be safe, even if it’s not. Many investments today, including the ones that would normally be used for safety, like bonds and money market funds, are vulnerable to loss of your principal and have other risks. Getting safe in a rising-interest rate, high-inflation environment is a two-step process. I spend one full day on this topic at our Investor Empowerment Retreat. I have an entire section devoted to “What’s Safe?” in The ABCs of Money 5th edition. I also have a free podcast and webinar that you can listen to and watch. 10. You should buy a house now before interest rates go up anymore. Buying a house at an all-time high is a risky proposition that could ruin your life for a decade or longer. There are many things you want to consider before buying a house. However, buying high and having the value of the home drop below the mortgage can be one of the worst investments you’ll ever make. Real estate is an illiquid investment, which means that you might have trouble getting yourself unencumbered from it. I have a webinar and podcast on this topic that it’s important to listen to before buying a home in 2022. If you purchased a home or a vacation home within the last few years, it’s a very good idea to make sure that you:

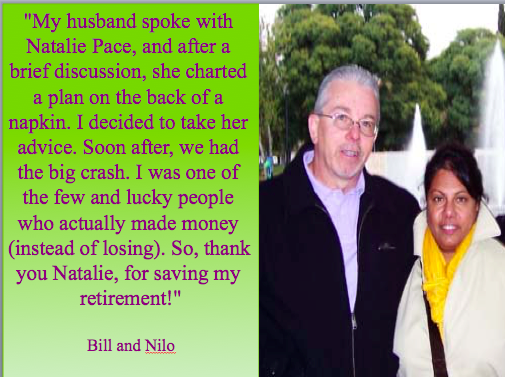

Bottom Line We learned during the Pandemic Recession that there are things we can’t live without no matter what is happening, like technology, toilet paper and hand sanitizer. What will be the industries that remain more buoyant in the next recession? While technology stocks have actually gotten hammered in 2022, we still need WIFI, smart phones and a lot of the AI that has become imbedded in our lives. The world is still committed to healing our planet and promoting cleaner and greener energy, food and companies. Most of us pay our utility bills, even when we tighten our budgetary belts. The U.S. is a country of innovators that produces a lot of what the rest of the world needs for existence. We tend to attract the top talent from around the world. (Many of our breakthroughs come from immigrants, like Sergey Brin, the co-founder of Google, who is Russian.) The stock market has never gone to zero in over a century – through many times of war and even the Great Depression. Market timing doesn’t work. That is one of the market aphorisms being bantered about that is absolutely true. However, having the appropriate amount safe, being properly diversified, knowing what is safe in a world where bonds and money market funds are vulnerable, and rebalancing at least once a year is a time-proven plan that has successfully navigated through each of the 21st century recessions (which are very different than last-century recessions). This might sound complicated, but it is actually easy-as-a-pie-chart – much easier than you might imagine. That’s why we call it the life math that we should have received in high school and college. The sooner you get a 21st-century, time-proven plan, the better off you’re going to be. It’s time to turn off the noise, sales-speak and the nonsense, and trust results. If you're interested in learning stock and 21st Century time-proven investing strategies for protecting your wealth and managing the downturn from a No. 1 stock picker, join us for our Oct. 8-10, 2022 Financial Freedom Retreat. Email [email protected] or call 310-430-2397 to learn more and to register. Click on the banner ad below to discover the 18+ strategies you'll learn and master. Get the best price and a free 4-part Protect Your Wealth Now webinar that will get you started immediately when you register before July 15, 2022.  Join us for our Financial Freedom Retreat. June 10-12, 2022. Email [email protected] to learn more. Register by July 15, 2022 to receive the best price and a free 4-part webinar (which you can access to protect your wealth now). Click for testimonials & details.  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Apple Podcast. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Why are Banks and Dividend Stocks Losing Money? Beyond Meat: Rare or Burnt? Netflix Streaming Wars End in a Bloodbath. Elon Musk Sells $23 Billon in Tesla Stock and Receives $23 Billion in Options. Are You Gambling With Your Future? ESG Investing: Missing the E. Moderna & Biotech Trade at 2-Year Lows. Bitcoin Crashes. Crypto, Bold and Stocks All Crash. The Economy Contracted -1.4% in 1Q 2022. The Dow Dropped 2000 Points. Is Plant-Based Protein Dying? Should You Sell in April? The U.S. House Decriminalizes Cannabis Again. Chinese Electric Vehicle Market Share Hits 20%. The Risk of Recession in 6 Charts. High Gas Prices How Will Russian Boycotts Effect U.S. Multinational Companies? Oil and Gas Trends During Wartime Russia Invades Ukraine. How Have Stocks Responded in Past Wars? Zombie Companies. Rescue, Rehab or Liquidate? Spotify: Music to my Ears. Cannabis Crashes. 2022 Crystal Ball in Stocks, Real Estate, Crypto, Cannabis, Gold, Silver & More. Interview with the Chief Investment Strategist of Charles Schwab & Co., Inc. Stocks Enter a Correction Investor IQ Test Investor IQ Test Answers Real Estate Risks. What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.

Corrie

20/6/2022 12:37:53 pm

"It’s time to turn off the noise, sales-speak and the nonsense, and trust results.". Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed