Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

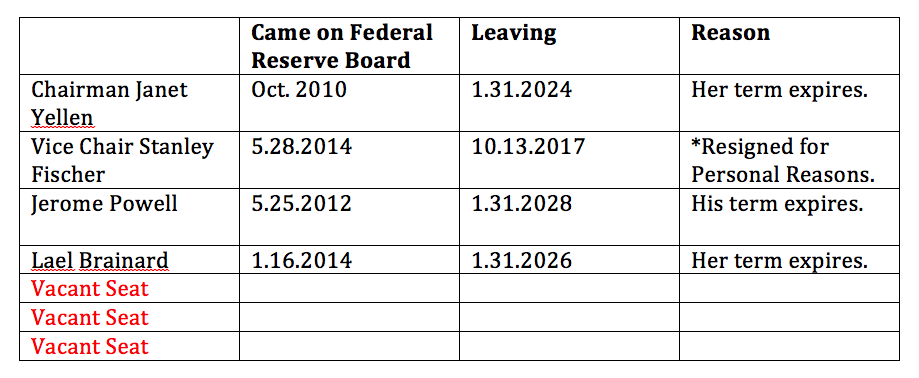

The Feds want to unload trillions of Treasury bills and mortgage-backed securities. However, who is left to pilot and ensure a "soft landing?" Just how much debt does the U.S. really carry, and which countries own it? Congress and the White House raised the debt ceiling for three months on September 8, 2017, and the U.S. public debt immediately soared to $20.2 trillion. Consumer debt is back to an all-time high, at $12.84 trillion. Corporations are borrowing money like there is no tomorrow, even those that already owe multiples more than the value of the company, with a total corporate debt of over $6 trillion. The total U.S. debt and loans surpass $66.7 trillion. Yes, these numbers are astronomical, so high that there has really only been one other time in the last century where this was the case. The U.S. held very high public debt to GDP levels after World War II. However, it was not accompanied by the astronomical consumer debt. There is a general hope, mostly by the people trying to manage this mess, that we’ll get through it now, as we did in the 1940s and 1950s, without an apocalyptic downturn, as occurred in the Great Depression. There are others who claim we are already in a Great Depression, which history will acknowledge in the coming years. A few things are certain. Stocks are higher than they have ever been. Housing prices are higher than they have ever been. And debt is higher than it has ever been. It is a well-known economic certainty that when interest rates are too low for too long, bubbles occur. (Money for Nothing: Inside the Federal Reserve does a good job of explaining this, from the Federal Reserve Board governors themselves.) So, will housing and stock prices “pop” again, as they did in the Great Recession and the Dot Com Recession before that, causing massive losses in their wake? One thing is for sure, “buy low; sell high” works every time. “Buy high, hoping to sell higher” is a risky game that can wipe out everything you own and then some. The U.S. economy was already stuck in slow growth -- before the hurricanes, which are predicted to drag us back beneath 2% GDP growth in the 3rd quarter of 2017. (Click to get more information in my teleconference.)  What is the Smart Money Doing? The smart money always moves first, and they are definitely moving towards the exits. The Federal Reserve Board will being releasing its massive mortgage and Treasury bill holdings back on the open market. The Federal Reserve “normalization” program begins in October of this year. The most immediate effects could be felt in the mortgage market. Corporations have slowed down their corporate buybacks. According to Howard Silverblatt, the senior analyst for S&P Dow Indices, Q2 buybacks were down almost 10% from Q1. Corporations have enough cash to keep buying their own stock, but they’ve put the brakes on that plan. Is it because the CAPE ratio (the retail price of stocks) is as high as it was before the Great Depression and the Dot Com Recession? Berkshire Hathaway's buyback plan allows for purchasing at 120% of book value, which is $146.28 -- almost $40/share lower than today's price. Who Holds the $20 Trillion U.S. Public Debt? For the most part, we do. If your 401K, IRA or savings account is invested in a Treasury mutual fund, ETF or money market, you own part of the U.S. debt. The Treasury has also borrowed from “the trusts for Federal Social Security, Federal Employees, Hospital and Supplemental Medical Insurance (Medicare), Disability and Unemployment, and several other smaller trusts” (according to the World Fact Book). About 31% of the debt is owned by foreigners, with China and Japan holding about $1.1 trillion each, followed by a lot of European nations, a few Middle Eastern nations, Russia and others. Who is Going to Pilot the Landing? There hasn’t been a full slate of board governors at the Federal Reserve since 2006. There are currently three vacancies and three filled seats, with a vice chairman departing mid-October (leaving 4 vacant seats). Federal Reserve Board Governors. September 27, 2017  Janet Yellen is expected to be replaced as the chairman of the Federal Reserve on February 3, 2018, when her first term as the chair expires. Most expect Gary Cohn to be nominated to take her place. If Randal Quarles is approved by Congress, then we could be back to four board governors filling seven spots. The fact that it has become almost impossible to have a full board of governors speaks volumes on how the experts feel about the current amount of leverage and how to fix things.  What does this mean for your nest egg, home and future? Market timing doesn’t work. Neither does buy and forget about it. If you were just hanging on hoping to get ahead, then your nest egg has been on a rollercoaster since 2000, and is very likely below where you started then (excluding any capital contributions). The last two times the U.S. economy went 8 years without a correction, most people lost more than half of their retirement. 7 million people lost their homes in the Great Recession and 5.4 million homes are still seriously underwater on the value (source: RealtyTrac.com). And this economy is far more fragile than it was in 2000 or 2008. In addition to knowing how to get safe, diversify and get hot, you really need to know what is safe in a world of astronomical debt. There are actually a large number of ways to rethink the world, and how your budget and investing fits in, with a vision that is cast out at least 10-years ahead, to be sure that you and your assets will withstand the financial storms that are likely to gust in the months and years ahead. In fact, our team has identified literally thousands of dollars that most people can save annually with smarter energy, budgeting and investing choices. You can get this information in my 3 bestselling books. You can call our office and set up an appointment to get a second opinion on your current budgeting and investing strategy. And you can learn The ABCs of Money that we all should have received in high school in my 3-day Investor Educational Retreat. Call 310-430-2397 to get solutions now! If you wait for the headlines that we are in trouble, it will be too late to protect yourself.

About Natalie Pace:

Natalie Pace is the author of the Amazon bestsellers The Gratitude Game, The ABCs of Money and You Vs. Wall Street (aka Put Your Money Where Your Heart Is in hard cover) and the co-creator of the Earth Gratitude project. Natalie Pace is a repeat guest on national television and radio shows such as Good Morning America, Fox News, CNBC, ABC-TV, Forbes.com, NPR and more. As a strong believer in giving back, she has been instrumental in raising tens of millions for public schools, financial literacy, the arts and underserved women and girls worldwide. Follow her on Twitter.com/NataliePace, and Facebook.com/TheABCsofMoney. For more information please visit NataliePace.com. Click to access a longer bio on Natalie Pace. Important Disclaimers Please note: NataliePace.com does not act or operate like a broker. We report on financial news, and are one of the most trusted independently owned and operated financial news corporations in North America. This article is intended to educate and inform individual investors, and, thus, to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned in this article are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  Dear Natalie, My former employer is offering me a small payout or pension benefits. The payout is around $16,000 and the pension benefits are $178/month ($2,136/year). I am leaning towards the payout and investing in some good stocks. I only have until Oct 2 to decide. Can you offer any advice? Signed, Every Little Bit Helps! Dear Smart to Ask for Help! This is really a two-part question. One is, “Should I take the buyout?” and two is, “Can I make a killing in stocks?” Should I Take the Buyout? If you are willing to learn about investing and be a good steward of your money, then taking a buyout is very likely a great idea. Most companies are underfunded on their pensions, and this is unlikely to improve in the coming years. In 2016, S&P 500 companies were underfunded by $391 billion on their pensions, with plans only 80.75% funded. Other post-employment benefits (like health benefits) were even more severely underfunded. Your company is one of the most severely underfunded in the U.S. So, the next offer you get could be a lot less than what you are currently being offered. Many legacy companies use Chapter 11 to restructure their debt and pension obligations when they get too overloaded. That is a risk going forward as well, if you choose the payment plan. If you want to discover whether or not your company is severely underfunded on pensions and/or other post-employment benefits, this information is often found in the annual earnings report. That is a lengthy, unwieldy report that is quite hard to read, until you learn how to do power-searches. I can usually locate this information in about 5 minutes. If you are not familiar with earning reports then you might not find this data at all! Should I Invest in Stocks? Even great stocks lose money in a bear market. So, it’s important to educate yourself on investing before you dive in to the stock market, or leap into any investment on the advice of a friend, family member of financial professional. There are a few critically important rules that are easy to understand and implement, and can be the difference between growing and enjoying your returns, or watching your investment evanesce in thin air. In short, you can certainly take a buyout and have that capital grow into a rewarding investment, but only if you’re willing to educate yourself and be the boss of your money. If you take the buyout and just hand it over to a “financial professional” without knowing what’s appropriate for you at your age and at this time in your life, you could end up giving the broker-salesman a great payday at your own expense. There are a lot of slick salesmen selling risky investments as “great” because they pay a nice commission (on the backend – you’ll be told that you don’t have to pay anything!). You can read about The ABCs of Money in my 3 bestselling books, or you can learn them firsthand in my 3-day life-transforming Investor Educational Retreats. I also offer second opinions on your current budgeting and investing strategy in my private, prosperity coaching sessions. Call 310-430-2397 or email Heather @ NataliePace.com to learn more. Test your investment skills in my Investor IQ Test.

About Natalie Pace: Natalie Pace is the author of the Amazon bestsellers The Gratitude Game, The ABCs of Money and You Vs. Wall Street (aka Put Your Money Where Your Heart Is in hard cover) and the co-creator of the Earth Gratitude project. Natalie Pace is a repeat guest on national television and radio shows such as Good Morning America, Fox News, CNBC, ABC-TV, Forbes.com, NPR and more. As a strong believer in giving back, she has been instrumental in raising tens of millions for public schools, financial literacy, the arts and underserved women and girls worldwide. Follow her on Twitter.com/NataliePace, and Facebook.com/TheABCsofMoney. For more information please visit NataliePace.com. Click to access a longer bio on Natalie Pace. Important Disclaimers Please note: NataliePace.com does not act or operate like a broker. We report on financial news, and are one of the most trusted independently owned and operated financial news corporations in North America. This article is intended to educate and inform individual investors, and, thus, to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned in this article are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Are you the boss of your money? Or do you place all of your faith in someone else managing your money for you, without any checks and balances to ensure that you are safe, protected and hot? Below are 3 easy questions to ask your financial partner to ensure that your plan is sound, along with 5 tips and 7 considerations on how to weather the next financial storm.  The immortal Isabel Huppert in the film Elle. How can you be the Boss of your Money? The first step is to learn the basics, and the second step is to hold yourself and your financial team accountable, by the books and numbers, not by their word. Top 3 Questions to Ask Your Financial Team to Make Sure That They Are Working For You (and not just getting rich by selling you things)

And it is just as important to know the right answers. Otherwise, you could be seduced by sales-speak. 1. How Much Of My Portfolio Should I Keep Safe? Sales-speak: “If you don’t invest, then your money just earns zero and doesn’t even keep up with inflation.” This sound byte is designed to get you to buy more stocks and take on more risk than might be prudent for you, for your risk tolerance, for the current marketplace and for your time horizon. Sales-speak: “Invest in this so that when the crash comes, you’ll be safe.” There are a lot of scams out there trying to capitalize on your fear, including gold scams, Bitcoin scams, penny pot stock scams, options trading software and more. When people scare the heck out of you and then sell you the cure, it’s often just snake oil. Be cautious and skeptical. The Right Answer: “How old are you? The general standard is to keep a percent equal to your age safe. I would overweight a little more safe right now because we are in the 9th year of the current bull market and the CAPE ratios are quite high.” If you have under a million dollars and are dealing with a broker-salesman who has a large number of clients (typically over 500), then odds are pretty low that you’ll get this answer. That is why it is so important to know the basics yourself, and to be the boss of your money and plan, rather than having blind faith in broker-salesmen. 2. How Much Commission Are You Being Paid to Sell Me This? Sales-speak: “You don’t have to pay me anything!” This is a side-step of the question. Most broker-salesmen are paid on the back-end to sell you things, not by you directly. And the higher the commission they are paid, the higher the risk of the asset that you are being sold. So, don’t settle for this answer. The Right Answer: “This [life insurance plan, annuity, REIT, mutual fund] pays 6% to me.” Remember that higher commissions and dividends = higher risk. So, if you hear if a commission or dividend that is 5% or higher, you then have to place even more forensic focus on question number 3. 3. How Safe is This Investment? Sales-speak: “Your investment will not go down in value.” Or “Owning real estate is better than stocks.” There are many ways that annuities and life insurance goes down in value. Most people who purchase life insurance have the policy lapse before the pay-out, even if they have paid in for decades, because when you retire and are on a fixed income, there will come a time when you have to choose between eating, having a roof over your head, visiting the doctor or paying your life insurance bill. If you miss a payment, or have any of a long list of other issues with the policy, then the insurance company can cut the benefit and dramatically increase the premium, making it unaffordable to continue the policy. With annuities, once you “annuitize” it, you give up the asset for the “guaranteed” annual income. In other words, if you deposited a million, and you die one year after you select “Income for Life,” then you’ve just lost a million dollars that could have gone to your loved ones or charity. Finally, all of the private placement REITs that I have personally looked at, which are in abundance today because they pay 7% commission to the broker-salesmen, are stock investments (not real estate investments) in companies that have been cash-negative for at least three years (in an up real estate market!). These investments are very high-risk and it is an out-and-out lie when they are sold to retirees as “safe” and income-producing. The Right Answer: The safest investment right now is FDIC-insured cash. It pays you nothing, but you have no risk of capital loss (of losing money). That is why we are taking on some risk (appropriately) on the stock side. Other Considerations: FDIC-insured cash is just the first step to getting safe. At my investment educational retreats, I teach attendees how to consider safe, income-producing hard assets that you purchase for a good price because hard assets hold their value better than paper assets when you have too much debt in the world. In addition, our team has identified thousands of dollars in annual savings that most people can save with smarter energy, budgeting and investing choices! These investments pay dividends for life. Learn about 12 Questions to Ask Your Broker in my first book: Put Your Money Where Your Heart Is. Learn what is safe and how to get safe in my second book: The ABCs of Money. Implement these strategies in the chapter-a-day 21-day plan in my third book The Gratitude Game. Keep reading for 5 Tips and More Facts, Market Conditions, Testimonials and Resources.

5 Tips

Facts & Market Conditions

Testimonials "My husband spoke with Natalie Pace, and after a brief discussion, she charted a plan on the back of a napkin. I decided to take her advice. Soon after, we had the big crash. I was one of the few and lucky people who actually made money (instead of losing). So, thank you Natalie, for saving my retirement!" Nilo Bolden. "College students need this information before they get their first credit card. Young adults need it before they buy their first home. Empty nesters can use the information to downsize to a sustainable lifestyle, before they get into trouble." Joe Moglia, Chairman, TD AMERITRADE. "Many people, including educated men and women, often get into trouble when they neglect to follow simple and fundamental rules of the type provided [by Natalie]. This is why I recommend them with enthusiasm." Professor Gary S. Becker. Dr. Becker won the 1992 Nobel Prize in economics for his theories on human capital. Additional Information (Blogs) Stock prices are as high as they were in the Great Depression and the Dot Com Recession. http://www.nataliepace.com/blog/august-21st-2017 What is the Smart Money Doing? http://www.nataliepace.com/blog/what-is-the-smart-money-doing Are You Gambling With Your Future? http://www.nataliepace.com/blog/are-you-gambling-with-your-future Will Congress Raise the Debt Ceiling in Time? http://www.nataliepace.com/blog/will-congress-raise-the-debt-ceiling-before-august Social Security is Cash Negative, at 28% of the Public Debt and Growing http://www.nataliepace.com/blog/social-security-is-cash-negative-at-28-of-the-public-debt Bitcoin and the Crypto Currency Flash Crash. (published on June 25, 2017). |

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed