Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

Are you alarmed by the reports of global warming, of sea levels rising, of islands disappearing, of an island of plastic floating in the ocean, of the predictions that, at the current rate, there will be more plastic in the ocean than fish in just a few short decades? Did you know that: * We already have our first climate refugees (from Louisiana). * On sunny days during high tides, fish and seawater flood the streets in Miami. * The mighty Colorado River has dried up 50 miles short of the ocean? * 62% of the U.S. electric grid is still powered with fossil fuels? Global warming isn't something we have to worry about tomorrow. It's here now.  What can you do? There are quite a lot of things that everyday folks can do to breathe cleaner air, preserve their fresh water, reduce their plastic usage and promote a healthy planet. I was so impressed with the 4-9 year olds at Damers First School in Poundbury, England, and their outstanding teacher Edd Moore, that I proclaimed them to be England's most powerful green lobby, on my ThriveGlobal blog. (See the picture of Queen Elizabeth visiting with the children below.) The Damers School students are showing how bad habits can be replaced overnight, so that each one of us can "be the change we wish to see."

On Wednesday, April 3, 2019, at noon ET (9 am PT), I will interview Edd Moore and a few of the Damers School children for their tips on how we as individuals can inspire our town, county and even country to eliminate plastic, reduce our fossil fuel usage and eat healthier. The following day, on Thursday April 4, 2019 at noon ET, Governor Bill Ritter, Colorado’s 41st governor and a director at the Colorado State University Center for a New Energy Economy, will enlighten us on technological developments in clean energy and steps each one of us can take toward a fossil-free future. You can call into both teleconferences at: 347.215.7305. Listen back links for both teleconferences are at BlogTalkRadio.com/NataliePace.  Bill Ritter, the 41st governor of Colorado. (c) 2016. Marie Commiskey. Avalon Photography. Used with permission. The Put Your Money Where Your Heart Is Conference in Loveland, CO on April 18, 2019 If you are in Colorado for Easter, join me in Loveland on April 18, 2019 for a Put Your Money Where Your Heart Is conference, hosted by the New Thought Northern Colorado Center for Spiritual Living. There we will play the Billionaire Game and learn how to put your money where your heart is and profit, while creating the world of tomorrow, for our children. Call 310-430-2397 or email [email protected] to learn more. Host Your Own Earth Gratitude Celebration On April 22nd, Earth Day, we're encouraging everyone to power up the gratitude and power down the pollution, getting as close to personal net zero as possible for at least one hour. What kind of celebration can you create that is both fun and life-transformational? Be epic. Observe the fresh insights that flood our awareness and the world consciousness. Challenge your friends. Organize an awesome community net zero event. Include the hash tag #EarthGratitude when you share your pictures and video, so that we can like and reshare. Contributors to the Earth Gratitude project include: HH The Dalai Lama, H.R.H. The Prince of Wales (the heir to England's throne), Elon Musk, Deepak Chopra, Arianna Huffington, Kathleen Rogers (the president of the Earth Day Network), Life is Good, WildlifeDirect, Global Green, the NRDC, Green Our Planet and many more. Some of their tips for a memorable Earth Gratitude celebration include:

Get additional information about the Earth Gratitude project at http://earthgratitude.org/. There you can download two free picturesque ebooks full of important information on sustainability, Clean Living and Future Earth. Share freely with your friends. http://earthgratitude.org/ Additional Information about my work in financial literacy, sustainability and personal empowerment can be found on my bio. https://www.nataliepace.com/about-natalie-pace.html

I'm very interested in learning what you are doing to celebrate and honor Mother Earth this April 22nd. Please use the #EarthGratitude, so that I can find your video & photos easily. Thanks!

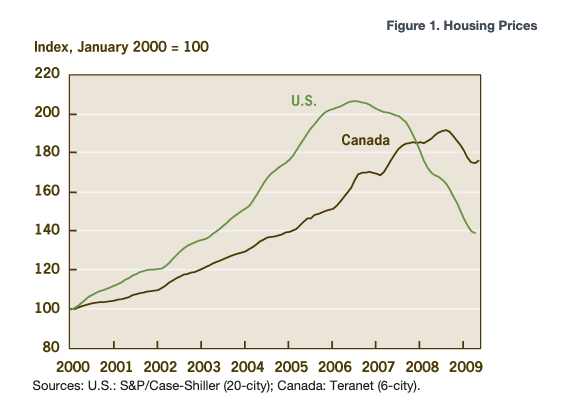

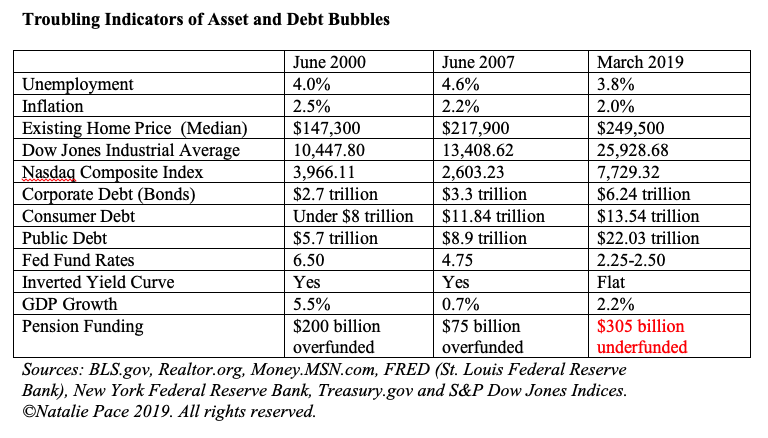

Buying real estate between 2005 and 2007 was a nightmare. Over 10 million homes were lost in the wake of the Great Recession. If you purchased a home in the years preceding 2008, or refinanced at or above the value of your home, the last decade was a living nightmare. Conversely, the low for real estate was in 2011. If you purchased a home then, you’re up at least by 53% (nationwide). Cities like Las Vegas, Denver, San Francisco and even Detroit have seen home values double or more. Seattle prices have skyrocketed by 76%. You’re riding high and living the Life of Riley! There is no denying that when you purchase an investment can be the most formidable foe, or your best ally. Dreams Do Come True! In February of 2011, a young entrepreneur in his mid-30s attended my Investor Educational Retreat. At that time, real estate was a bargain. He was earning a good, steady income, and had a young family. He lived in Las Vegas, where real estate prices had plummeted. AT could purchase a home and live in it for much less than he was spending on rent. Plus he could write off the mortgage interest to reduce his taxable income and save a boatload on taxes each year. AT was just starting out with his nest egg, and wanted tips to diversify it and get it going. He wasn’t even thinking of purchasing a home. However, I said that the lowest-hanging fruit for him was to purchase a home first, and then start building up the nest egg. He did. His home value doubled by 2017, at which time he sold, took his profits and made a dramatic move to British Columbia, where he built his own off-grid sustainable home, where he lives with his wife and young son. He has traded in the stress of commuting in Vegas for the challenges of living in the wilderness. However, having the funds to create his new life began by making an outstanding home purchase in 2011. The Canadian market tends to shadow the U.S., as you can see in the chart below. This has a lot to do with the fact that low interest rates create asset bubbles. (More on that to come.)  Subprime Hell In May of 2005, I began screaming from the rooftops that real estate was in a bubble. One friend refused to be warned about the real estate bubble, however. Her “mentor” kept encouraging her to load up on properties in Las Vegas as late as even 2007. She pooh-poohed my warnings about bubbles with a rather supercilious hubris, as she put down payments on credit cards and relied upon no-interest loans where she didn’t have to show gainful employment or income. When her actions caught up with her in 2009, and she could no longer afford to float things on credit cards, she lost 5 properties, was buried in lawsuits and was financially and emotionally bankrupt. (We offered her husband and her a scholarship to a retreat to put them on the road to recovery.) Another example of subprime hell came in the form of a successful young woman, BB, who was at her wit’s end when she came to my Investor Educational Retreat in January of 2008. Her boyfriend’s friend had suckered her into buying a condo in Florida in 2007. This realtor “friend” promised to flip it within a few short months and give her back a quick and easy $20,000-$40,000. After months of paying high mortgage and Homeowner Association fees, while watching the value of her purchase plummet, she reached out to me in desperation for some private coaching. I found a legal colleague who was able to assist her in getting a deed in lieu (giving the keys back to the bank). When you make a grave investment mistake that is likely to decrease dramatically in value, the sooner you accept this and get out of it, the better off you’ll be. BB’s credit score recovered rather quickly (before most people even got out of their subprime hell). She also saved herself several years of hell and hundreds of thousands of dollars by getting out early. She’s now a proud homeowner and the mother of a young son (rather than the desperate servant of an underwater condo) and in a loving relationship (with a different life partner). Real Estate Education ala Trump University Most real estate seminars offer you very basic tips on how to secure a loan. They tout up the value of owning income-property (which is real) – without having a time-proven system on how to make sure your investment is a rewarding, dream-come-true “money while you sleep” experience, instead of a nightmare that can dog you for decades (which is always a potential reality with a big purchase like real estate). Trump University wasn’t the only ruse that suckered people into investing tens of thousands of dollars for inexperienced mentors offering unsound strategies. This space is still full of marketers who pose as good investors, with enticing language and exciting offers (even free seminars!), who whitewash over the Great Recession as if it never existed. If you take the bait, you’ll then be sold into expensive mentoring and software. However, that’s not the only cost of that free real estate seminar. If you buy high in real estate, you don’t just lose your investment. You could be on the hook for hundreds of thousands of dollars of lost equity, if the value of your property falls beneath the amount of your loan. You’ll be stuck with it, unable to sell it. And if you are able to short sell it, then you could be stuck with a very high tax bill on the “phantom income” of the difference between the sale price and your loan. The Most Important Key to a Great Real Estate Investment Again, one of the most important considerations for buying real estate is the price itself. Real estate prices are back to an all-time high. So, now is the time when most of these real estate mentors will be revealed as self-serving marketers rather than masters. It’s important you learn that lesson in the wings, rather than on your own dime. Low Interest Rates Create Asset Bubbles Low interest rates create asset bubbles. As you can see in the chart below, asset prices (stocks and real estate) are back to all-time highs. Debt is now astronomical. The statistics that politicians use to claim a strong economy, low unemployment and inflation, are not indicators of where the economy is headed. In fact, since 2000, asset bubbles have been the reliable harbingers of recessions.  Real estate prices plummeted during the Great Recession, with many markets dropping to less than half their value at the high. It’s a warning worth heading today. With real estate prices back to an all-time high, what’s your best game plan? 1. Learn how to implement the 3-Ingredient Recipe for Cooking Up Profits for your real estate investment. Do your research and planning now, so that you’ll be ready to make a purchase when prices become more favorable. There are many events that create buying opportunities, including bubbles popping, deflation, unaffordability, the labor market slackening, natural disasters, terrorist events, the 4 D’s (death, depression, divorce and disaster) and more. The 3-Ingredient Recipe for Cooking Up Profits 1. Start With What You Know and Love. 2. Pick the Leader. 3. Buy Low; Sell High. 2. There is also more shadow inventory than most professionals are aware of. So, it will really pay to know the market you wish to buy into, and understanding how many people are hanging onto property they cannot afford by a thread. Any local market with a judicial foreclosure process is likely to have a lot more shadow inventory. Did you know that there are still more than five million U.S. homes that are severely underwater – owing at least 25% more than their value (source: AttomData.com)? 3. You will also do well with thinking bigger, and considering innovative solutions to pervasive problems, such as affordable housing, which is needed in most major cities in the developed world. Real estate prices are downright unaffordable in many major cities. As Lawrence Yun, the chief economist of the National Association of Realtors said in our recent conversation, “Unaffordability is making home sales plunge in California, even though the job market is great. Unless California can address the unaffordability of housing, you may see people leaving the area.” Any “guru” who tells you today is different than 2007 is not giving you the complete picture. (Take another look at the Asset Bubble chart above.) You can listen to my complete interview with Lawrence Yun on my BlogTalkRadio.com/NataliePace pod cast. Today, many asset bubbles are at an all-time high. You can’t afford to get bad advice. That is why I’m offering the Real Estate Master Class this April 26, 2019 in Denver, Colorado. Call 310-430-2397 or email info @ NataliePace.com to learn more and register now.

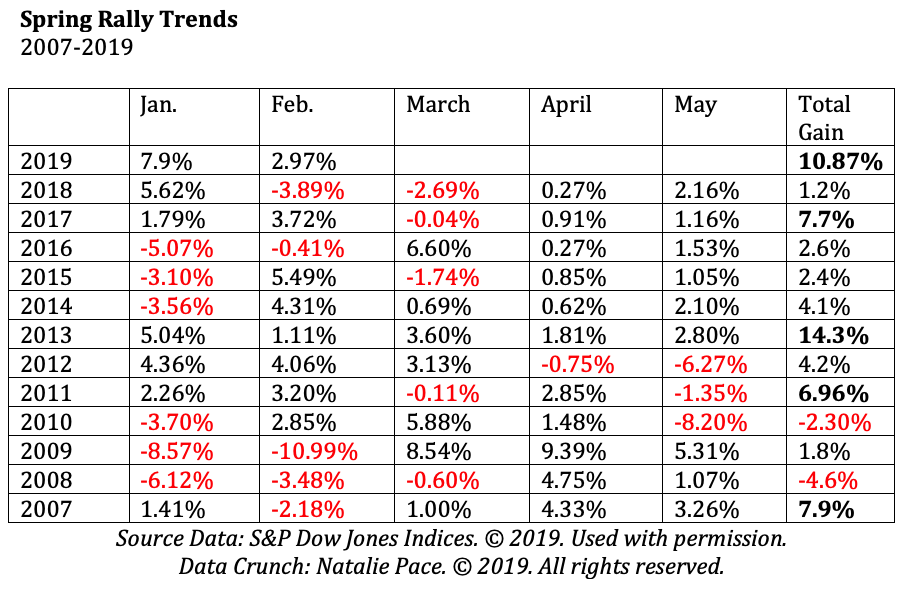

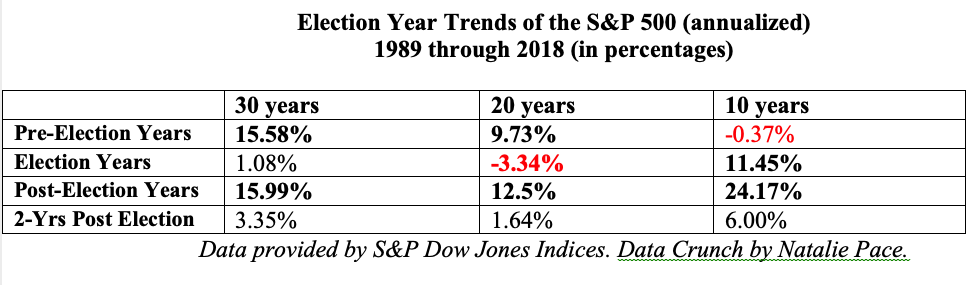

Other Blogs of Interest Is the Spring Rally Over? The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  Today, the Dow Jones Industrial Average dropped 460 points, marking the worst day-drop since the 660-point drop on January 3, 2019. And both of these plummets were preceded by the worst December since the Great Depression. Is the Spring Rally over? The good news is that the recent tax cuts sparked 2018 to the fastest economic growth the U.S. has seen since 2006, at 2.9% and 3.3%, respectively. The bad news is that wasn’t matched with spending cuts, so the public debt is higher than its ever been – at $22 trillion. On Wednesday, the Federal Reserve Board indicated there will be no interest rate hikes this year, and that they will stop deleveraging their own balance sheet at the end of this September. That seems like good news on the surface, particularly for interest-rate sensitive industries, like housing, and leveraged corporations that need to borrow money. However, since two of the primary economic concerns are overleverage (too much debt) and pricey valuations (bubbles), and since low interest rates contribute to bubbles and borrowing, continuing an accommodative stance risks exacerbating those two problems. Alan Greenspan, Warren Buffett, Robert Shiller and many other economists have all gone on record saying that stocks and bonds are in a bubble. Click to read through 12 Economic Concerns outlined in the Financial Stability Report that was released on November 28, 2018. Also, having the Fed Fund Rate at just 2.25-2.50% doesn’t give the Federal Reserve much room to lower rates, and goose the economy, when things head south. The most recent GDP growth projections are for 2.1% growth in 2019 and 1.9% in 2020 – much lower than 2018’s 2.9% – which is why the Federal Reserve is pausing on their interest rate hikes. The 1st quarter 2019 GDP growth is predicted to be downright dismal – at 1.2-1.3%. What Does All of This Mean for the Spring Rally 2019? After the worst December (2018) on Wall Street since the Great Depression (1931) -9.13 and -14.53% in the S&P500 respectively, Wall Street came roaring back. The Dow Jones Industrial Average is up 10.5% since the beginning of the year. Can the rally continue? Should you lean into the returns assuming there will be more wind at your back? Or is it time to take cover into a defensive position, and do a full assessment of the level of risk in your current plan? To answer these questions, I did a big data crunch to determine… * How well do March, April and May perform, when January and February are strong? * Do they continue the trend or give back some of the gains? * Is the pre-election year a rocket booster or a headwind on the Spring Rally? And here’s what the 10-Year Data revealed. * Most of the time when January and February are strong, the Spring Rally (including May) is weak. * The average gains for the first five months of the year are 4.3%. * The years with the strongest starts had the weakest growth, while the years with the stronger growth had negative (2010) or low performance (2015) in the first five months. * The pre-election year is usually great for the Spring Rally. 2007 gained 7.9% in the 1st five months of the year, while 2011 saw a solid 7% jump over that same period. In 2015, however, returns were tepid, at 2.4%.  10.5% gains (January 1, 2019 – March 21, 2019) is much higher than the average performance. There was only one year, in 2013 with 14.3% gains during the first five months of the year. So, historical performance trends would suggest a weak Spring Rally, giving back some of the gains of January and February. Pre-election trends are not as reliable today as they were in the past. The 10-year average is a loss of -0.37%, while the 20-year average is 15.58% gains.  Another interesting point is that two of the strongest 5-month starts on Wall Street, in 2013 and 2011, came with forward projections of an improving economy. The recent projections were revised downward to a very slow growth of 2.1% growth in 2019. Wall Street veterans are always forward-thinking. So, today’s sell-off isn’t surprising. April 26, 2019 is a Big Day for Bad News On April 26, 2019, we’ll get the advance numbers for GDP growth in the first quarter of this year. Economists are projecting growth between 0.4% and 1.4%. That is significantly lower than the 4th quarter 2018 growth of 2.6%. Investors typically don’t respond well to such a sharp slowdown. The Most Predictable Recession Indicator Just Flashed Red The yield curve just inverted today, with the 10-year treasury falling .03 percentage points below the 3-month treasury yield of 2.46%. An inverted yield curve is 100% correlated with recessions over the past half a century. Buybacks Dry Up During the Quiet Period Bloomberg reported on March 20, 2019 that corporations had ceased buying back their own stock – a key driver of this entire bull market – and would stay on the sidelines throughout the 5-week quiet period before earnings announcements – through mid-April. As you can see from the below chart of buybacks, corporations purchasing their own stock is a perfect mirror of Wall Street performance. Purchases were at a high when Wall Street spiked in October. Both hit the pits at the end of December, only to rally strong through the first two months of 2019. Corporate buybacks are clearly driving Wall Street’s performance. In short, there are far more red flags than green lights on Wall Street for the Spring Rally. December 2018 reminds us that when the winds change, losses can cut like a falling knife. The right answer is never all in or all out, but is, rather, a diversified plan that keeps enough safe, underweights the overleveraged companies and adds in performance. A well-diversified plan that is annually rebalanced forces you to do what you must do for successful investing in today’s world – buy low and sell high on auto-pilot in your nest egg. The days of Buy and Hope paying off ended in 1999. 2018 was a year when stocks and bonds lost money, which means that 2019 is the year that you need to know what you own, know what a healthier plan looks like and take charge – being the boss of your money. Below is a list of the Economic Red Flags present in today’s economy… Economic Red Flags Prices are too high. Debt is too high. Growth is too slow. Productivity is too sluggish. There is an $879 billion U.S. trade deficit (2018 FY). $22 trillion U.S. public debt (as of 3.22.19). The Debt Ceiling was hit 3.1.19. X date should land in Aug/Sept/Oct. 1Q 2019 GDP will be released on April 26, 2019. It is predicted to be 0.4% - 1.5%. The Feds have paused on rate hikes, and will stop balance sheet deleveraging at the end of September. Consumer and fixed income spending are softening. U.S. GDP is $20.9 trillion, while Debt is $22 trillion. If you wait for the headlines on these red flags, it will be too late to protect yourself. You don’t have to understand economics to employ a time-proven easy-as-a-pie chart nest egg strategy that earned gains in the last two recessions (when most people lost more than half) and outperformed the bull markets in between. Blind faith that someone else is doing this for you can be very expensive. (It’s a good idea to get a second and third qualified, unbiased opinion on your current plan, rather than just trusting that your money manager has protected you.) Wisdom is the cure. (Click to read more about the High Cost of Free Advice.) As the landscape changes rapidly, time proven systems will be your ally. Join me at my Colorado Investor Edu Retreat, where we’ll examine how to protect your assets, learn what's safe in a world where stocks and bonds are in a bubble and invest profitably in high growth opportunities (like cannabis). Call 310-430-2397 or email info @ NataliePace.com to learn more about the retreat, or to request an unbiased second opinion on your current budgeting and investing plan!

Other Blogs of Interest

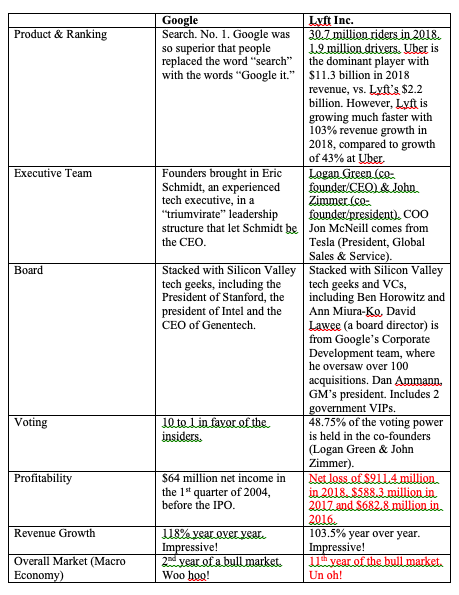

The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  The long-anticipated Lyft IPO is ready to drive onto the NASDAQ stock exchange, (with the symbol LYFT). Should you catch a ride? To put the LYFT IPO into better perspective, I lined up some of the key metrics alongside another highly anticipated IPO of yesteryear, Google. Google went on to become an $826 billion company (now called Alphabet Inc.). Can Lyft support a market value of $18.5 billion? Should you invest once it hits the big boards, which is expected to be as early as next week?  As you can see in the above chart, Lyft comes with an impressive line-up. Growth is astounding. The leadership is top-tier. Perhaps my favorite fact about Logan Green and John Zimmer is that their passion for the company was born in statistical data that there were too many single-occupant vehicles on the road. Lyft’s vision is to “improve people’s lives with the best transportation.” They were early in the e-scooter space, and are investing heavily in autonomous vehicles. The problems with the IPO relate solely to profitability and the macro economy. Lyft has been cash negative for three years now, with losses of almost a billion in 2018 ($911.4 million). We’ve gotten accustomed to companies losing a lot of money or carrying a very high price-to-earnings ratio. This is largely because it is very cheap for businesses to borrow money. Banks are willing to take on a lot of risk to keeping loaning companies money, so that they can rack up the fees for their own quarterly earnings. However, with an economy that is expected to slow down to 0.4-1.4% in the 1st quarter of 2019, pricey valuations can be very risky. When investors get skittish about valuation, even companies that are experiencing great growth and enormous market share can lose a lot of value very rapidly.  It’s possible that the hype and potential of Lyft could lift the share price up next week when it begins trading. However, a tepid 1st quarter GDP report on April 26, 2019, which many fund managers are expecting now, could also make any lift short-term. The macro economy sobered up the valuations of other rock star companies like Netflix and Nvidia in December 2018, and it is very possible that it could do the same with Lyft in late April. Lyft is a great company that is disrupting old-school transportation. The trends, revenue growth and leadership team are all in the company’s favor. However, the macro economy winds are in the company’s face. As the landscape changes rapidly, time proven systems will be your ally. Join me at my Colorado Investor Edu Retreat, where we’ll examine how to invest profitably in Lyft, cannabis, and many more high growth opportunities in far greater detail. Call 310-430-2397 or email info @ NataliePace.com to learn more!

Other Blogs of Interest Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  Since I added cannabis as a Hot slice of my nest egg pie chart at the end of September 2018, companies like Cronos and Aurora have doubled off of their lows earlier this year. Is this the beginning of a rocket ship to the moon, or is the party over for cannabis? Not since the end of Prohibition has something that the majority of citizens do anyway leaped the red tape fence to become legal faster. Now that the War on Drugs is over (and stoners won), cannabis is hitting the main stream in dozens of ways. Fitness buffs tout it at as a panacea for most dis-ease. Suffers of pain swear by CBD Oil. And you don’t have to get high to enjoy a relaxing cannabinoid bubble bath these days. Check out MedMen’s film The New Normal, by Spike Jonze, to see a history of cannabis and hemp pre and post prohibition. The investment opportunities are abundant. However, there are still a few penny pot stock scams out there that will take you into the back alley and strip you of your dough. So, it’s a good idea to stick to cannabis companies that are publicly traded on the big boards, and are helmed by talented, experienced C-level executives. Beware of email and social media marketing campaigns as many are pump-and-dump schemes. Cronos is now 45% owned by Altria (Philip Morris Tobacco). MedMen’s executive team includes leaders from Apple Retail, with former Los Angeles Mayor Anthony Villaraigosa on the board. Tilray’s international advisory board includes Vermont Governor Howard Dean, and senior government officials from Australia, New Zealand, Germany and Portugal. Constellation Brands invested $4 billion in Canopy Growth. The founder and former CEO of Hain Celestial is the chairman and interim CEO at Aphria. The newcomers, Green Growth Brands, features the executive team of Victoria’s Secret. Green Growth Brands has launched a hostile takeover of Aphria, which Aphria is fighting. The future is green for cannabis, now that it no longer lurks in the shadows. However, the share prices have experienced extreme volatility. Last year, Tilray soared to $300/share, and then sank to $73 within a few short months. MedMen (CSE: MMEN or OTC: MMNFF) was at $7.58/share in late October. It’s now at $2.87. Cronos has doubled since October and Aurora Cannabis has done the same since December. Clearly this has nothing to do with the growth in the industry, and has everything to do with trading. Tens of millions of cannabis stock shares are traded daily. Once you’ve picked a winning stock that you want to invest in, you still need to purchase it for a good price. Otherwise, you could be on the wrong side of a Tilray or Medmen trade. My personal strategy has been one of taking profits early and often, but never clearing the entire table. So when Cronos and Aurora doubled, I took a large bit of gains off the table, and left some invested. That way if the rocket ship continues, I continue to experience more gains. If the share price implodes, then I can buy more low again. A company like MedMen, which is trading near their 52-week low while experiencing astronomical sales growth year over year of 873% (far above the competition), might experience some swing in share price, even though all signs point to up up up. And that’s because navigating when to buy and when to sell requires, at minimum, three major considerations. Number one: what is the company capable of doing? (There seems to be no stopping any of these companies, most of which are growing in triple digits.) Number two: what’s going on with the industry? (Cannabis is exploding in growth. In addition to the legacy base of loyal enthusiasts, CBD oil has gone mainstream with consumers.) Number three: what’s going on in the macro economy? This is a huge consideration as we enter the 11th year of the current bull market. A rising tide certainly lifts all ships. But a sinking tide can ground them. On April 26, 2019, a GDP report of 0.4-1.4% growth (what is projected for 1Q 2019) could sink a few share prices. High growth cannabis stocks like Cronos and Aurora Cannabis were drug down in October and December, when stocks had the worst December since the Great Depression. That is why I rushed to put cannabis as a hot slice on the pie chart on September 30, 2018. It was easy money because you were buying low. Today, when a lot of the cannabis stocks have doubled, the calculation is more complicated. In addition to having cannabis as a hot in my pie chart, I’ve added Latin America. The cannabis companies are all based out of Canada these days (the second country, behind Uruguay, to legalize recreational marijuana). However, the expert pot and hemp growers are in Latin America – all of the former drug lords… As the landscape changes rapidly, time proven systems will be your ally. Join me at my Colorado Investor Edu Retreat, where we’ll examine these, and many more, opportunities in far greater detail. Full Disclosure: As of the printing of this blog, I own positions in Aurora, Cronos and MedMen and a Colombian ETF.

Other Blogs of Interest 12 Investing Mistakes Drowning in Debt? Get Solutions. What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  The Fearless Girl statue was commissioned by State Street Global Advisors to honor International Women's Day in 2017. Top 12 Investing Mistakes There are many Wall Street sayings that can help you to navigate successful investing. Below are 12 common mistakes that you want to avoid, and beneath them 12 Better Ideas. 1. Blind Faith. What’s a better idea: Be the boss of your money. 2. Fear, or Trusting Your Gut. What’s a better idea: Wisdom. 3. Never Confuse a Bull Market With Wisdom. What’s a better idea: Employ a time-proven strategy that works in bull and bear markets. 4. Following Analyst Recommendations. What’s a better idea: If contrarianism was a great long-term plan, then you could just do the opposite of what the analysts say to enjoy superior returns. However, the better idea is to employ a time-proven strategy. 5. Trading on Headlines. What’s a better idea: Silence the nonstop noise and stick to your knitting (another Wall Street saying that means to stick to your strategy and not be led astray). 6. Hot Tips. What’s a better idea: Diversification and annual rebalancing. 7. Holding Too Much Company Stock. What’s a better idea: Limiting the amount you hold of company stock to 10%. (Enron.) 8. Listening to the Advice of Family, Friends and Bloggers. What’s a better idea: Grade your guru before you listen to anything she says. 9. Considering Your Broker to Be Your Friend. What’s a better idea: Consider your broker to be your employee. 10. Market Timing. What’s a better idea: Proper diversification, underweighting risk, overweighting hot industries and annual rebalancing. 11. Unreasonable Expectations What’s a better idea: Employing a system that doesn’t require you to bat 1000. 12. Reaching for Yield. What’s a better idea: Know what’s safe when there is too much credit risk. And here’s a little more color on each point. 1. Blind Faith. So many people want to just “turn it over to someone else” to handle for them, so that they can enjoy their life and worry about earning more money. That’s not how rich people think, and the results of blind faith are not good. Since 2000, if you’ve abdicated your responsibility to be the boss of your money, you’ve been riding a Wall Street rollercoaster, losing more than half every 8-10 years. It wasn’t a New Economy in 2000. (Dot Com stocks lost more than 78%). It wasn’t true that real estate prices were on a rocket ship to the moon in 2007. (Banks, brokerages and insurance companies wouldn’t be in business today if the U.S. taxpayer hadn’t bailed them out.) Today, the risk is leverage and too much debt. A lot of informed investors have moved to fee-based management. However, when stocks and bonds are in a bubble and money market fund have liquidity fees and redemption gates, even the fee-based advisor has a conflict of interest in trying to get you safe. What’s a better idea: Be the boss of your money. Know what a healthy nest egg strategy looks like, how to adopt a Thrive Budget and time-proven tips that have worked over the last 19 years, at a time when most people are losing more than half of their nest egg every 8-10 years, and over 15 million homes went to auction. 2. Fear, or Trusting Your Gut. Using any emotion to invest is a recipe for disaster. When you are afraid, you’ll be prompted to buy low. When you are excited, you’ll be tempted to buy high. What’s a better idea: Wisdom. There are time-proven investment strategies (that you will not receive from a broker/salesman). There are reliable business cycles. And there are economic realities that spark inevitable macro trend movements. When things are bubblicious, you have to be more conservative. When things look like the Apocalypse, it’s probably time to start buying. This is completely counter to your intuition, which is why you need to use wisdom rather than your gut. 3. Never Confuse a Bull Market With Wisdom. If your home value or nest egg has earned gains since 2009, great! That’s not because you or your financial planner are great investors. It’s because real estate, stocks and bonds have been in a bull market, which is largely fueled by free, easy, borrowed money (which is why debt and credit risk are at all-time highs). As Warren Buffett has noted many times, corrections show who has been swimming naked. All investments can flip from green to red at any moment, zooming right past yellow before you can protect yourself. What’s a better idea: Employ a time-proven strategy that works in bull and bear markets. Complacency is not your friend in 2019. Call 310-430-2397 to learn more about my easy-as-a-nest egg pie charts that earned gains in the last two recessions and have outperformed the bull markets in between. If you’re interested in real estate, join me for my Real Estate Master Class on April 26, 2019, and stay for the 3-day Investor Educational Retreat.

4. Following Analyst Recommendations. Researchers at the University of California and Stanford University found that, in the year 2000, the stocks most highly rated by analysts lost 31 percent for the year. Even more incredible is this finding from the study: The stocks least favored by the major analysts soared 49 percent. This study examined 40,000 stock recommendations from 213 brokerages. Now, in all fairness, this is mostly just a case of supply and demand. When analysts say, “Buy,” the brokers all buy (for their clients), and the share price goes up. When the analysts say, “Sell,” the brokers all sell, and the price drops faster than soufflé. That’s why trading on headlines is the 5th Investing Mistake. (See below.) What’s a better idea: If contrarianism was a great long-term plan, then you could just do the opposite of what the analysts say. However, again, the better idea is to employ a time-proven strategy of keeping enough safe, of knowing what is safe when stock, bonds and real estate are in bubbles, proper diversification, avoiding the bailouts, adding in hots and annual rebalancing. 5. Trading on Headlines. If you wait for the headline, you’re late. The Feds didn’t admit we were embroiled in an economic meltdown until October of 2008, when stocks had already lost almost 40%. The same was true before 911. The NASDAQ had already lost 64% before 911 occurred. What’s a better idea: Silence the nonstop noise and stick to your knitting (another Wall Street saying that means to stick to your strategy and not be led astray). If your plan only works if the value of your investment keeps rising, it’s a plan that’s being sold to you by a salesman with a conflict of interest. 6. Hot Tips. The most common way that people lose money is through a hot tip from a friend, a family member or their “investment advisor.” What’s a better idea: Diversification and annual rebalancing. If you want to invest in something hot, then there is a slice of your pie for that. Never bet the farm. 7. Holding Too Much Company Stock. Many companies increase the value of their own stock by giving it out to employees. That’s free money for you, but only if you are able to turn paper stock into real cash. Enron employees held almost 60% of their retirement in Enron stock, and were unable to trade out of it before the company surprised everyone and declared bankruptcy. Enron declared bankruptcy on December 2, 2001 – the same year that Fortune named it the Most Innovative Company (for the 6th time in a row). What’s a better idea: Limit the amount you hold of company stock to 10%. That’s part of your annual rebalancing strategy. 8. Listening to the Advice of Family, Friends and Bloggers. You wouldn’t let your gardener cut your hair. Letting unqualified novices give you financial guidance can result in an unwanted haircut of your assets. What’s a better idea: Grade your guru before you listen to anything she says. 9. Considering Your Broker to Be Your Friend. What’s a better idea: Consider your broker to be your employee. There should be regular meetings about strategy, reports about performance and a sober discussion about the current opportunities and challenges. You should have any questions you have answered in plain, easy to understand language and backed up with paperwork. 10. Market Timing. Jumping all in or all out is a terrible strategy. Most people are tempted to sell everything at a market bottom, selling low and buying in when the party is raging – buying high. Even if you are a contrarian, this is the wrong plan, because there is always opportunity in every stage of the business cycle. Also, if you’re hot of the market, then it’s difficult to know the exact time to get back in. And if you’re all in, you’re praying for a Hail Mary, which succeeds only some of the time, but more often results in a turnover. What’s a better idea: Proper diversification, underweighting risk, overweighting hot industries and annual rebalancing. A better plan for a home purchase is to understand the right neighborhood for you, to purchase something that is within your budget, to be patient about getting your home for a good price and to plan on living there for at least seven years. The days of rapid gains in real estate and the ability to buy and flip are likely behind us. 11. Unreasonable Expectations. The higher the dividend, the higher the risk, and the higher the commission paid to the broker/salesman. Many people are lured into investments that pay a dividend, with the sales pitch that the asset is safe. Some people have an unreasonable expectation that reading a book will transform their lives. What’s a better idea: Employing a system that doesn’t require you to bat 1000. There’s a lot of nonsense and bad information in even bestselling financial books. So, you first have to grade your guru. And then, once you know you’re dealing with a shaman instead of a showman, you’ll need to immerse yourself in training in order to start up the path to wisdom. You wouldn’t expect to learn how to play the guitar, or even fishing, in one weekend or by reading one book. Your results in investing will be in direct proportion to your commitment, real-world practice, right action and ability to be the boss of your money and know exactly where you are invested and why. Making a few mistakes is part of learning and mastering anything. Those “errors” will not be devastating if you have a good system and are part of the learning curve. Incidentally, this is why I developed The Gratitude Game: 21 days to a healthier, wealthier, more beautiful you – so that you can take things day by day, a chapter a day to be exact, and start implementing the time-proven Easy-as-a-Pie-Chart Nest Egg Strategies ® and Thrive Budget ® that I teach at my retreats and have written about in my books. 12. Reaching for Yield. What’s a better idea: Know what’s safe when there is too much credit risk. The saying is, “Don’t reach for yield.” Or as Roy Rogers said, “I’m more concerned with the return of my money than the return on my money.” Even a 4-5% yield takes you into or very close to junk bond territory. Over 50% of investment grade companies are just one rung above junk status. GE was keeping investors interested with a high dividend. However, those who bought in lost their dividends and half of their investment. CDs are offering a very low yield. Many are not FDIC-insured. Many have penalties for early withdrawal (creating an opportunity cost). Some are tied to an index and might lose money. Wisdom and time-proven systems are more essential now than ever. Complacency is not your friend. Real estate, stocks, debt, risk and bonds are higher than they have ever been. If you wait for the headlines on this, it will be too late to protect yourself. If you’re serious about adopting the better ideas, your journey starts with learning The ABCs of Money that we all should have received in high school. Call 310-430-2397 to learn more about transforming your life with my time-proven, easy system. I have 3 bestselling books, life-transformational Investor Educational retreats and I’m happy to offer an unbiased second opinion on your current budgeting and investing strategy. If you’re interested in receiving a personalized, sample Thrive Budget and nest egg strategy, call 310-430-2397 or email info @ NataliePace.com.

Other Blogs of Interest Drowning in Debt? Get Solutions. What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.   Ask Natalie: Drowning in Debt. I’ve gotten myself into a huge mess of credit card debt. It’s time to do a clean up job, and change poor habits. This isn’t who I am or want to be. I have so much emotion around money failure. The spreadsheets are easy. The emotions. Damn. Signed, Drowning in Debt Dear Swimming in a Sea of Possibilities, Remember that negative emotions only inhibit your ability to see and execute a better plan. So, yes, acknowledge the emotions, but don’t sit in a mud puddle of debt, counting the bills and complaining or crying. It’s time to stand up, shower off, and replace the debt collector’s plan with one of your own. At the point you are at, most people are letting the debt collector design their budget. That won’t help you much. And it might not even help your credit score. Did you know that 1/3 of your credit score is assets to debt? So, if you’re just paying off debt, even if you’re religious about paying on time, your credit score may not be improving, if your net value is much lower than your total debt. I’ll get to a few tips in just a moment, but first I want to clear up the blame game a bit. Consumer debt is at an all-time high. There are a lot of Americans in your shoes. It's a silent epidemic because everyone is too embarrassed to admit it.  The U.S. isn’t drowning in debt because we are a nation of shopaholics. If that were the case, then Sears wouldn’t be bankrupt. There are other macro trends at play. The big-ticket bills – housing, transportation, health care and insurance – have all skyrocketed. Housing is unaffordable in the cities where the best jobs are. Meanwhile, wages have stagnated for over two decades. Millennials have to add college loan debt on top of this toxic debt dump. They exit college making the same wages their parents did, with a debt bill that is much higher than their parent’s housing costs were. So, rather than blame yourself for bad money habits, a better way is to see things as they are, and find solutions for what’s really happening. Getting your budget in alignment, for most people, is not a matter of cutting out café lattes, excessive shoe buying or eating out too much. You can do all of that and still be homeless. What really has to occur is a total reboot of your entire life. I’ll give you a few examples. Millennials are already figuring this out. The majority of people under 30 don’t have a driver’s license or a car. They prefer to live close to work and ride a bike or an e-scooter, or walk. Ride-share apps are there to get you home after a few drinks or for schlepping groceries. The cost savings of not owning a car is about $7,500 annually for most people, when you add up the car payment, the insurance, the gasoline and maintenance. A few months ago, I interviewed the former mayor of Santa Monica, California. Mayor Ted Winterer shared that his family of four adults has only one car and five bikes. In 2017, he and his wife spent about $2000 on ride-shares, as compared to the $7,500 average annual cost of a car. Remember: getting rid of your car actually equates to a better lifestyle. If you’re riding a bike or walking more, you’re promoting personal health! Transportation is not the only big-ticket item that you can slash in half or more with smarter choices. As a young, single mother, I got a bigger home in a better neighborhood for less money because I was willing to share it with another single mother and her kids. It turns out that cooking for 5 is as easy as cooking for 2, and cheaper to boot, when you only have to cook two weeks out of the month. Childcare costs were dramatically reduced as well. The famous attorney Gloria Allred also did this when she was a young mother to get ahead. Richard saved tens of thousands of dollars when he opted for a high-deductible health insurance plan and a family health savings account. Joe Moglia invested in education when he was a young father trying to make ends meet on a college coach’s salary. (Education is the highest correlating factor with income.) He became the CEO of TD AMERITRADE, where he is still the chairman (since retiring in 2008). Joe has now returned to his original passion of coaching football because, as he sees it, “Having an impact on an 18-22 year old boy’s life, helping the boy become a man, it’s tough to find another field of endeavor that gives you greater satisfaction than that.”  Fixing a debt problem requires just two things: increasing your income and decreasing your expenses. However, getting smart and creative about those two things will launch you out of the quagmire faster than just trying to earn your way out by getting a second job or demanding a raise. As a young single mother, I invested well to earn passive income and almost tripled my money. I reduced costs with house-sharing and paid less to the taxman by opening up retirement accounts. The right answers for you are going to be different than they were for me, for Richard, or for Joe. However, when you stop buying into the shame and conventional nonsense – that shaving off dimes from your shopping splurges and getting a raise will fix things – and start embracing brave choices and real solutions, then you’ll start walking up the path to your dream-come true life. Once you stop making the taxman, the debt collector, the health insurance company, the car dealer, the gas station, the insurance salesman, the utility company and more rich at your own expense, and you start earning money while you sleep, you’ve solved the problem. Wisdom is the cure. So, in short, dry up the tears. Find a meditation spot that makes you happy. And start dreaming up solutions for the big-ticket costs in your life, and for lasting increases to your salary and income (including passive income). I had to live my way into answers that weren’t found in the books. That worked so well, that I developed it into a system and wrote three books on budgeting and investing to help folks like you do it, too. Our team calls these books The Life Math Trilogy. They work best together. Again, wisdom and right action are the cures.

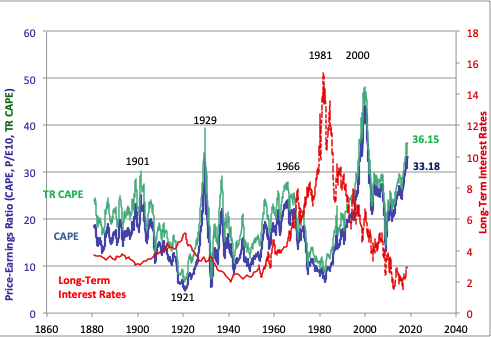

Make sure that your financial house is secure enough to withstand the economic storms that are on the horizon. Call 310-430-2397 to learn easy, time-proven strategies that earned gains in the last two recessions and have outperformed the bull markets in between. Join No. 1 stock picker Natalie Pace at a 3-day Investor Educational Retreat. Register for the Colorado Retreat scheduled for April 27-29, 2019 now.  Other Blogs of Interest What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  Real estate was the “lowest hanging fruit” to invest in, back in 2009. Since then, prices are up 47% nationwide. Detroit real estate has quadrupled in some areas. Here’s a segment of me discussing the upside of real estate a few years ago on Fox News. After that segment, areas like Denver and Idaho popped by another 45%-52%. Last year, the nest egg pie charts featured a hot newcomer – publicly traded cannabis stocks. There were a few tricks that were important to consider, such as avoiding penny pot stock scams and newly formed ETFs. However, those who learned how to evaluate the opportunity have seen their investment in companies like Cronos double. What’s hot and what’s safe changes every year, which is why it is important to rebalance your nest egg annually, and get updated on the latest trends. There is a lot of noise in financial media from people with very little experience and, frankly, terrible results. So, grade your guru before you listen to anything she has to say. Otherwise, your hot tips might be nothing more than paid promotional pump-and-dump schemes, a loser product that pays high commissions to salesmen or just plain, old-fashioned bad advice. So, what’ hot for 2019? Real estate prices are astronomical and unaffordable in many cities. We’re starting to see weakness in sales. Stocks valuations are higher than ever, and lost money in 2018. Bonds have more credit risk than most people realize, and have been losing value for over a year. Many respected economists have been quite frank about saying that stocks and bonds are in a bubble, including Alan Greenspan and Warren Buffett. According to Robert Shiller, Nobel Prize winning economist and Yale professor of economics, “The only time in history going back to 1881 when [CAPE] has been higher are, A: 1929 and B: 2000. We are at a high level, and its concerning. People should be cautious now.”  Robert Shiller's CAPE ratio. (c) 2019. Used with permission. In 2000, when NASDAQ began a descent into losses of 78%, the hottest asset was cash, and 2019 may well be another year where that is the case. Keeping your money can be a great investment when everyone around you loses more than half, which is what happened in the last two recessions. (See the charts below.) Since the economic data today is even more troubling that it was in 2000 or 2008, it’s important to keep this top of mind. As Warren Buffett reminded his shareholders in 2017, “There is simply no telling how far stocks can fall in a short period... No one can tell you when [market reverses] will happen. The light can at any time go from green to red without pausing at yellow." Below are charts of the Dow Jones Industrial Average dropping 55% in the Great Recession (2007-2009), and the NASDAQ Composite Index dropping 78% in the Dot Com Recession (2000-2002).