Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

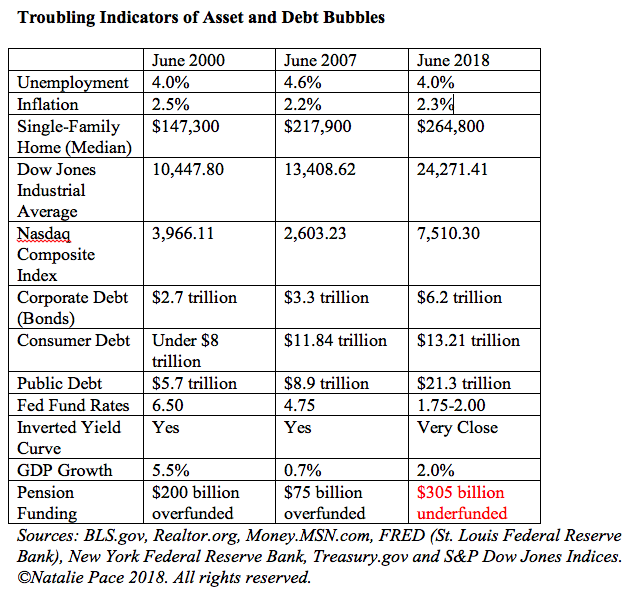

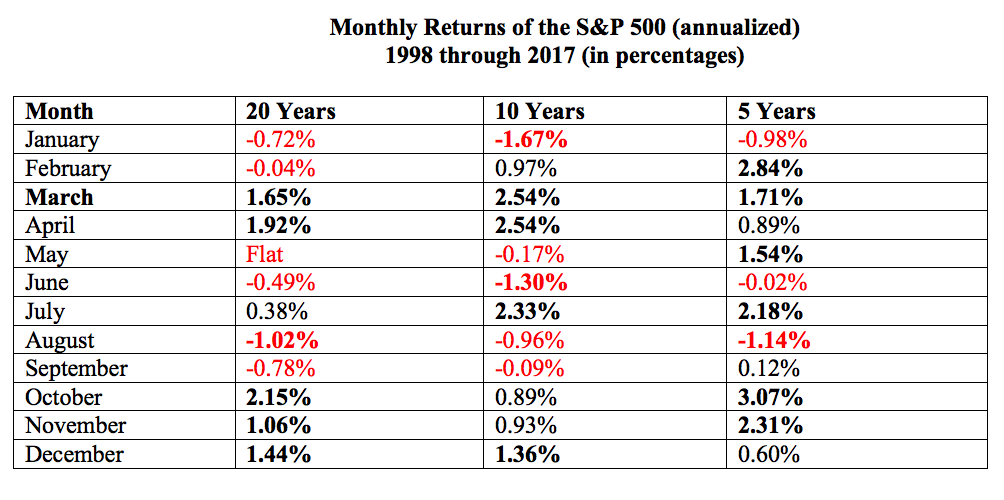

FLOTUS & I are honored to welcome the President of the People's Republic of China, Xi Jinping, & Madame Peng Liyuan to the United States." This image was taken at Mar-a-Lago. April 7, 2017. (c) The White House. Wiki Commons License. Used with permission.  G20 Argentina 2018 group photo. Wiki Commons license. Used with permission. Tariffs + Trade + + Interest Rates + Quiet Periods + Leverage + Valuation Issues + The Financial Stability Report = the Wall Street Rollercoaster and Losses to Your Nest Egg. Already. So far the 2018 Santa Rally has been coal in the stocking for Wall Street, with losses of 4% since October (including Wednesday’s rally). January looks more vulnerable. That’s why it’s important to get safe, diversified and rebalanced before January 2019. On Wednesday, November 28, 2018, Wall Street rallied on two key words, "Just below." The jump happened right after Federal Reserve Board chairman Jerome Powell’s speech to the Economic Club of New York. Powell said, “Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy‑‑that is, neither speeding up nor slowing down growth.” The Dow Jones Industrial Average jumped 618 points, while the NASDAQ Composite Index (with lots of technology FANG* stocks) rallied almost 3%. Investors were thrilled because they believed this indicated that interest rates might get a pause after December’s expected increase of another 25 basis points. However, even with yesterday’s rally, the DJIA is only up 2.5% on the year. So, unless December is a rip-roaring rally, 2018 marks a year where investors lost money their nest egg. Stocks are not performing well enough to keep up with fees, and bonds (the safe side of your nest egg) lost money. The issue with stocks is valuation. Prices are still too high. The issue with bonds is leverage. There’s just too much debt. All of that was revealed (and more) in the Federal Reserve’s Financial Stability Report, which was also released on Wednesday. The pressure on stocks and bonds is expected to get worse in 2019, which is why it’s important to protect yourself now, before January. Here’s a chart on the asset bubbles, compared to where the economy looked prior to the last two downturns (which cost investors more than half of their retirement).  Here’s a chart on monthly performance. As you can see, January has been a loser over the last 5-20 years.  Data provided by S&P Dow Indices. Data crunch by Natalie Pace. (c) 2018 Natalie Pace. All rights reserved. That is why it’s very important that everyone gets safe, diversified, hot and protected now, and knows what is safe in a world where stocks are vulnerable and bonds are already losing money. And that is why I now offer a second opinion on your nest egg, so that you can know exactly what you own, how diversified (or not) you are and the areas of strength and weakness in your current plan. You have to be the boss of your money, and having the right information is key to that. Blind faith that someone else is doing this for you, or hope that everything will be okay, is not a strategy. In fact, it has cost investors all over the developed world more than half of the assets every 8-10 years on average since the new Millennium began.

through December 23, 2018, if you bundle a second opinion with a retreat registration, you receive up to 50% off. Call for details. Here are the highlights of the Federal Reserve Board’s Financial Stability Report from November 28, 2018. 1. Banks. Money Market Funds. What They Said. “Banking institutions have built stronger capital and liquidity buffers that, together with reforms to the rules governing money market funds, strengthen the ability of institutions to withstand adverse shocks and reduce their susceptibility to destabilizing runs. Money market fund reforms implemented in 2016 have reduced “run risk” in that industry… Across the entire banking sector, the credit quality of bank loans appears strong, although there are some signs of more aggressive risk-taking by banks. The leverage of borrowers who are receiving C&I loans from the largest banks has been trending up in recent years, reflecting the overall upward trend in business leverage.” What That Means. Money market funds now have liquidity fees and redemption gates, which will stave off any run on the banks. In other words, you might have to pay to get your money, or you might have to wait to get access to your money. Banks should be in good shape. However, they are taking on more risk than might be prudent in lending to overleverage businesses. 2. Debt. What They Said. “Overall, vulnerabilities arising from total private-sector credit appear moderate. Among businesses, debt levels are high, and there are signs of deteriorating credit standards. In addition, recently, debt has been growing fastest at firms with weaker earnings and higher leverage. By contrast, household borrowing has advanced more slowly than economic activity and is largely concentrated among low-credit-risk borrowers.” What That Means. Debt is Too High, particularly in debt-laden businesses. It’s high on the consumer side, too. In fact, higher than ever. However, the debt is more concentrated in people with good credit scores. (People who need money can’t borrow to get it.) 3. Business Leverage Has Become Risky. What They Said. “Credit standards for new leveraged loans appear to have deteriorated over the past six months. The share of newly issued large loans to corporations with high leverage—defined as those with ratios of debt to EBITDA (earnings before interest, taxes, depreciation, and amortization) above 6—has increased in recent quarters and now exceeds previous peak levels observed in 2007 and 2014 when underwriting quality was notably poor (figure 2-5). Moreover, there has been a recent rise in “EBITDA add backs,” which add back nonrecurring expenses and future cost savings to historical earnings and could inflate the projected capacity of the borrowers to repay their loans…” What That Means. Beware of junk bonds and companies with high dividends, as those companies are more high-risk than you might be aware of. 4. Corporate Bonds. What They Said. “The share of bonds rated at the lowest investment-grade level (for example, an S&P rating of triple-B) has reached near-record levels. As of the second quarter of 2018, around 35 percent of corporate bonds outstanding were at the lowest end of the investment-grade segment, amounting to about $2¼ trillion. In an economic downturn, widespread downgrades of these bonds to speculative-grade ratings could induce some investors to sell them rapidly, because, for example, they face restrictions on holding bonds with ratings below investment grade. Such sales could increase the liquidity and price pressures in this segment of the corporate bond market.” What That Means Beware of bond funds. You need to do a credit analysis of any investment-grade bond that you own. Even your investment grade bonds and bond funds are vulnerable to capital loss and illiquidity. If you need the money back before the term, it might not be possible. And even though you are now investing in what you believed was low-risk, it could become high-risk virtually overnight. 5. Rich People are Borrowing a Lot of Money. What They Said. “Loan balances for borrowers with a prime credit score, who account for about one-half of all borrowers and about two-thirds of all balances, continued to grow in the first half of 2018, reaching their pre-crisis levels (after an adjustment for general price inflation)… The ratio of outstanding mortgage debt to home values is at the moderate level seen in the relatively calm housing markets of the late 1990s, suggesting that home mortgages are backed by sufficient collateral… Half of borrowers with near-prime and subprime credit scores were essentially unchanged from 2014 to the middle of 2018.” What That Means If you need money, you still can’t get it. If you don’t need money, You’re okay now as long as home prices remain high. Since home prices are expected to fall with rising interest rates, that could be a vulnerable strategy. Don’t use debt as an ATM machine to sustain a potentially unsustainable lifestyle. Just because you can borrow doesn’t mean that you should. 6. Student Loans. What They Said. “Student loans had aggregate balances of about $1.5 trillion at the end of the second quarter of 2018. Over 90 percent of these loans are guaranteed by the U.S. Department of Education and were extended through programs that did not involve traditional loan underwriting. Through the first half of 2018, student loan delinquency rates continued to improve gradually but remain elevated by longer-run standards.” What That Means Student loan debt is a problem and delinquencies are high. 7. Auto Loans and Credit Cards. What They Said. Payment delinquency rates for subprime credit cards and auto loans, which were on the rise for the past few years, also seem to be stabilizing, although, in the latter case, they remain relatively high. In addition, early payment delinquencies (delinquencies occurring on relatively new credit accounts) remain high for credit cards and have continued to rise for auto loans in the first half of 2018, suggesting that underwriting standards might continue to be looser than usual in these two segments and underscoring the need for ongoing monitoring of associated vulnerabilities. What That Means Delinquencies and defaults are very high for autos and credit cards issued to Main Street Americans with a low credit score. More than half of Americans under the age of 50 have a low credit score. 8. Hedge Funds. What They Said. “Average hedge fund leverage has risen by about one-third over the course of 2016 and 2017… as well as some easing in credit extended to hedge funds. The increased use of leverage by hedge funds exposes their counterparties to risks and raises the possibility that adverse shocks would result in forced asset sales by hedge funds that could exacerbate price declines.” What That Means With $7.3 trillion in total assets, and a large amount of leverage, hedge funds are vulnerable. Their need to sell to cover leverage and margin could result in very rapid movements that would harm, but not devastate, the U.S. economy. If prices decline, the hedge funds could cause those declines to be faster and deeper than normal. 9. Bond Funds. What They Said. “Total assets under management in corporate bond mutual funds and loan mutual funds have more than doubled in the past decade to over $2 trillion (figure 4-5). Corporate bond mutual funds are estimated to hold about one-tenth of outstanding corporate bonds, and loan funds purchase about one-fifth of newly originated leveraged loans. The mismatch between the ability of investors in open-end bond or loan mutual funds to redeem shares daily and the longer time often required to sell corporate bonds or loans creates, in principle, conditions that can lead to runs, although widespread runs on mutual funds other than money market funds have not materialized during past episodes of stress. If corporate debt prices were to move sharply lower, a rush to redeem shares by investors in open-end mutual funds could lead to large sales of relatively illiquid corporate bond or loan holdings, further exacerbating price declines and run incentives. Moreover, as noted in earlier sections, business borrowing is at historically high levels, and valuations of high-yield bonds and leveraged loans appear high. Such valuation pressures may make large price adjustments more likely, potentially motivating investors to quickly redeem their shares.” What That Means Beware of bond funds. 10. Insurance Companies. What They Said. Life insurers have been shifting their portfolios toward less liquid assets, somewhat weakening their liquidity positions. What That Means. Are you aware that insurance companies are not FDIC-insured and that if the U.S. had not bailed out AIG in 2008 over 50 million policyholders would have been without much of a backstop? Just how safe and protected is your annuity? 11. Risks. Brexit. China. Rising Interest Rates. What They Said. “An escalation in trade tensions, geopolitical uncertainty, or other adverse shocks could lead to a decline in investor appetite for risks in general. The resulting drop in asset prices might be particularly large, given that valuations appear elevated relative to historical levels. In addition to generating losses for asset holders, a significant fall in asset prices would make it more costly for nonfinancial businesses to obtain funding, putting pressure on a sector where leverage is already high. Markets and institutions that may have become accustomed to the very low interest rate environment of the post-crisis period will also need to continue to adjust to monetary policy normalization by the Federal Reserve and other central banks. Even if central bank policies are fully anticipated by the public, some adjustments could occur abruptly, contributing to volatility in domestic and international financial markets and strains in institutions.” What That Means. All eyes and ears will be on the dinner tonight with the American and Chinese Presidents. More tariffs are problematic. A deal would be a step in the right direction for investors. The fallout has a trickle-down affect that might be more of a waterfall, largely because asset prices are too high to begin with. 12. Vulnerabilities. What They Said. “Valuation pressures are generally elevated, with investors appearing to exhibit a high tolerance for risk-taking, particularly with respect to assets linked to business debt… Debt owed by businesses relative to gross domestic product (GDP) is historically high, and there are signs of deteriorating credit standards.” What That Means. Your dividend-paying stocks are pricier and riskier than you might realize. Values are very high. Be careful of having too much at risk. Santa Rally 2018? So far this Santa Rally has been coal in the stocking for Wall Street, with losses of 4% (including Wednesday’s rally). If there is a truce on the trade war between the U.S. and China that is announced this week, the market could react favorably. However, it would just be making up lost group, with a vulnerable January on the horizon. It’s a good idea to get protect yourself now. Call 310-430-2397 or email [email protected] to learn what you own and easy, time-proven, critically-acclaimed strategies that earned gains in the last two recessions and have outperformed the bull markets in between. If you are interested in receiving an unbiased second opinion on your current investing strategy, email [email protected] or call 310-430-2397. You can learn the ABCs of Money that we all should have received in high school at one of my Investor Educational Retreats. Only 3 seats remain available at the Valentine’s Retreat in Santa Monica. Receive a complimentary private, prosperity coaching session (value $300) when you register for the Colorado Retreat by November 30, 2018.

Other Blogs of Interest The Best Investment Decision I Ever Made. Thanksgiving 2018 Stocks Losses. Black Friday Sales. Get a 2nd Opinion on Your Current Investing Strategy. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed