Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

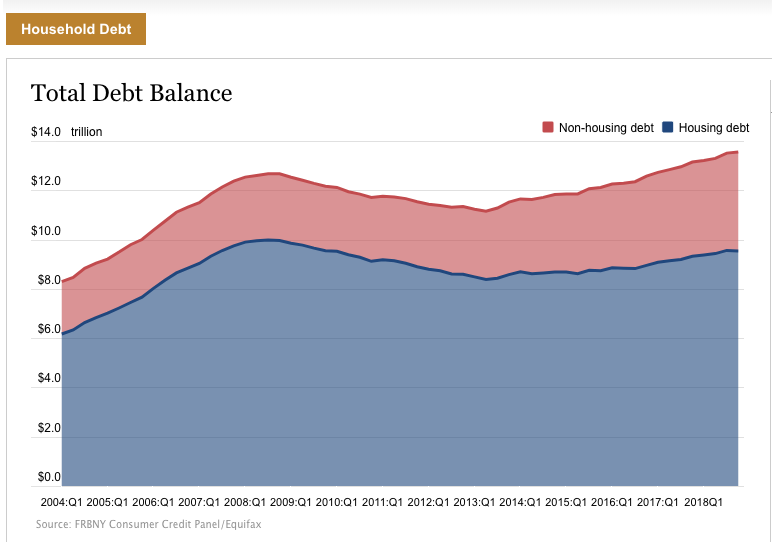

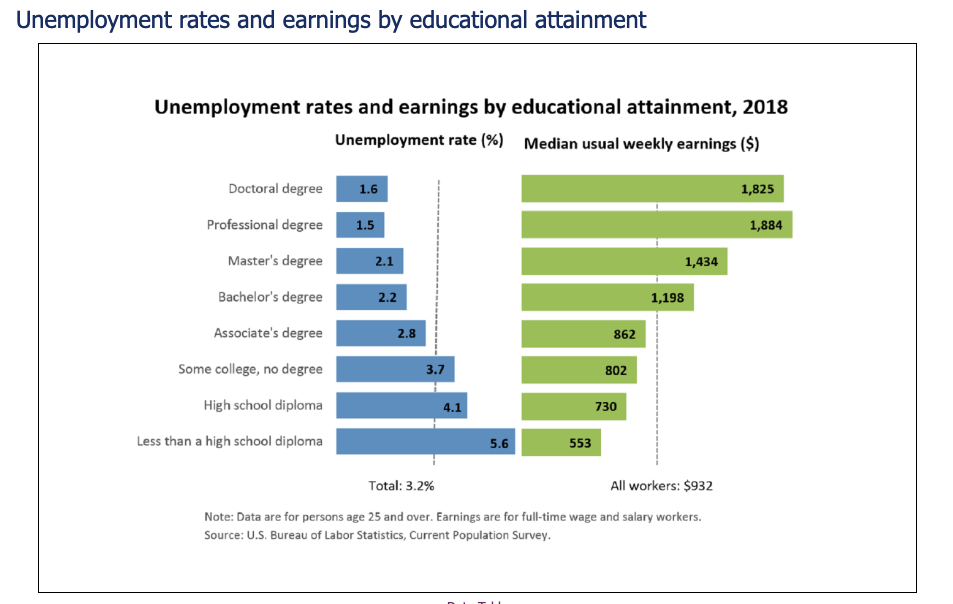

Ask Natalie: Drowning in Debt. I’ve gotten myself into a huge mess of credit card debt. It’s time to do a clean up job, and change poor habits. This isn’t who I am or want to be. I have so much emotion around money failure. The spreadsheets are easy. The emotions. Damn. Signed, Drowning in Debt Dear Swimming in a Sea of Possibilities, Remember that negative emotions only inhibit your ability to see and execute a better plan. So, yes, acknowledge the emotions, but don’t sit in a mud puddle of debt, counting the bills and complaining or crying. It’s time to stand up, shower off, and replace the debt collector’s plan with one of your own. At the point you are at, most people are letting the debt collector design their budget. That won’t help you much. And it might not even help your credit score. Did you know that 1/3 of your credit score is assets to debt? So, if you’re just paying off debt, even if you’re religious about paying on time, your credit score may not be improving, if your net value is much lower than your total debt. I’ll get to a few tips in just a moment, but first I want to clear up the blame game a bit. Consumer debt is at an all-time high. There are a lot of Americans in your shoes. It's a silent epidemic because everyone is too embarrassed to admit it.  The U.S. isn’t drowning in debt because we are a nation of shopaholics. If that were the case, then Sears wouldn’t be bankrupt. There are other macro trends at play. The big-ticket bills – housing, transportation, health care and insurance – have all skyrocketed. Housing is unaffordable in the cities where the best jobs are. Meanwhile, wages have stagnated for over two decades. Millennials have to add college loan debt on top of this toxic debt dump. They exit college making the same wages their parents did, with a debt bill that is much higher than their parent’s housing costs were. So, rather than blame yourself for bad money habits, a better way is to see things as they are, and find solutions for what’s really happening. Getting your budget in alignment, for most people, is not a matter of cutting out café lattes, excessive shoe buying or eating out too much. You can do all of that and still be homeless. What really has to occur is a total reboot of your entire life. I’ll give you a few examples. Millennials are already figuring this out. The majority of people under 30 don’t have a driver’s license or a car. They prefer to live close to work and ride a bike or an e-scooter, or walk. Ride-share apps are there to get you home after a few drinks or for schlepping groceries. The cost savings of not owning a car is about $7,500 annually for most people, when you add up the car payment, the insurance, the gasoline and maintenance. A few months ago, I interviewed the former mayor of Santa Monica, California. Mayor Ted Winterer shared that his family of four adults has only one car and five bikes. In 2017, he and his wife spent about $2000 on ride-shares, as compared to the $7,500 average annual cost of a car. Remember: getting rid of your car actually equates to a better lifestyle. If you’re riding a bike or walking more, you’re promoting personal health! Transportation is not the only big-ticket item that you can slash in half or more with smarter choices. As a young, single mother, I got a bigger home in a better neighborhood for less money because I was willing to share it with another single mother and her kids. It turns out that cooking for 5 is as easy as cooking for 2, and cheaper to boot, when you only have to cook two weeks out of the month. Childcare costs were dramatically reduced as well. The famous attorney Gloria Allred also did this when she was a young mother to get ahead. Richard saved tens of thousands of dollars when he opted for a high-deductible health insurance plan and a family health savings account. Joe Moglia invested in education when he was a young father trying to make ends meet on a college coach’s salary. (Education is the highest correlating factor with income.) He became the CEO of TD AMERITRADE, where he is still the chairman (since retiring in 2008). Joe has now returned to his original passion of coaching football because, as he sees it, “Having an impact on an 18-22 year old boy’s life, helping the boy become a man, it’s tough to find another field of endeavor that gives you greater satisfaction than that.”  Fixing a debt problem requires just two things: increasing your income and decreasing your expenses. However, getting smart and creative about those two things will launch you out of the quagmire faster than just trying to earn your way out by getting a second job or demanding a raise. As a young single mother, I invested well to earn passive income and almost tripled my money. I reduced costs with house-sharing and paid less to the taxman by opening up retirement accounts. The right answers for you are going to be different than they were for me, for Richard, or for Joe. However, when you stop buying into the shame and conventional nonsense – that shaving off dimes from your shopping splurges and getting a raise will fix things – and start embracing brave choices and real solutions, then you’ll start walking up the path to your dream-come true life. Once you stop making the taxman, the debt collector, the health insurance company, the car dealer, the gas station, the insurance salesman, the utility company and more rich at your own expense, and you start earning money while you sleep, you’ve solved the problem. Wisdom is the cure. So, in short, dry up the tears. Find a meditation spot that makes you happy. And start dreaming up solutions for the big-ticket costs in your life, and for lasting increases to your salary and income (including passive income). I had to live my way into answers that weren’t found in the books. That worked so well, that I developed it into a system and wrote three books on budgeting and investing to help folks like you do it, too. Our team calls these books The Life Math Trilogy. They work best together. Again, wisdom and right action are the cures.

Make sure that your financial house is secure enough to withstand the economic storms that are on the horizon. Call 310-430-2397 to learn easy, time-proven strategies that earned gains in the last two recessions and have outperformed the bull markets in between. Join No. 1 stock picker Natalie Pace at a 3-day Investor Educational Retreat. Register for the Colorado Retreat scheduled for April 27-29, 2019 now.  Other Blogs of Interest What Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. 28/11/2019 11:00:59 pm

As you become experienced, you will pick on the hard mode often, while the soft mode will be suitable for beginners still working on their balance and timing on when to get on and off the large 10-inch hoverboard. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed