Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

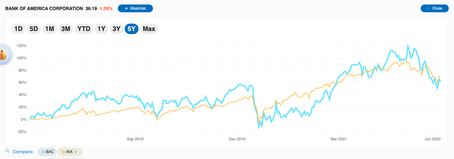

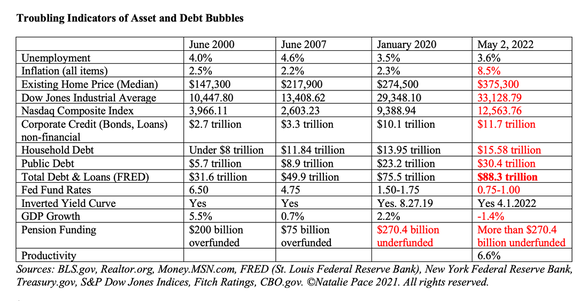

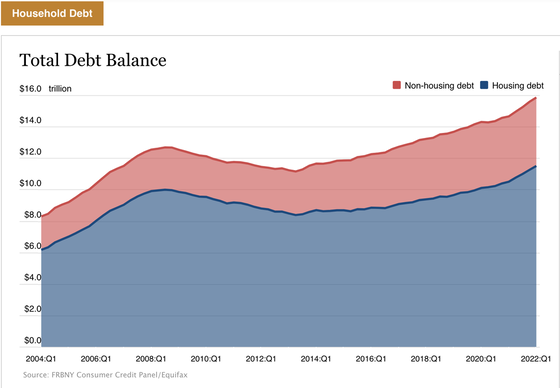

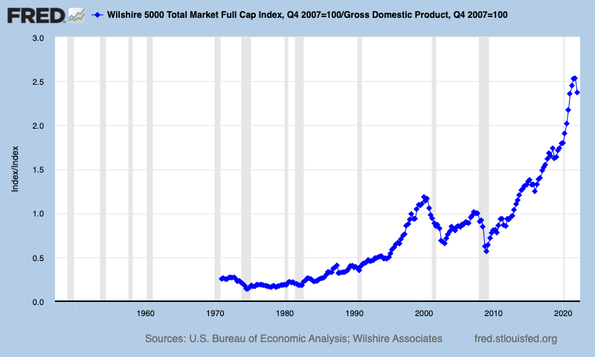

Investors Ask Natalie: Why Are Bank Stocks Going Down? Shouldn’t They Rise With Interest Rates? While you might think it’s logical that when interest rates rise, banks make “bank,” there’s actually a high correlation with rate hikes and recessions, especially when the rate hikes are unexpected and aggressive. Last week, Jamie Dimon warned that there is an economic “hurricane” on the horizon. We just don’t know how devastating it will be yet. Share price plunges typically precede the actual recession, and bank stocks are no exception to the rout. If you do a chart comparison of major banks compared to the S&P500, they look like shadows.  Bank of America stock compared to the S&P500. Source: MSN.com. (c) Microsoft 2022. Used with permission. It’s important to remember that stocks dropped 55% in The Great Recession and took almost 6 years to crawl back to even. The NASDAQ drop was even more dramatic (-78%) and prolonged (15 years) during the Dot Com Recession. Since asset valuations were even higher in 2022 than they were in the Dot Com Bubble, comforting ourselves with the false hope that “it always comes back,” isn’t a great plan. As researchers Pascal Paul and Simon W. Zhu noted in their report for the Federal Reserve Bank of San Francisco, “What matters for banks is not the level per se but the margin between different interest rates.” When short-term (bank borrowing rates) rise too rapidly, the banks are exposed to interest-rate risk without the buffer of a term premium. The profit margins are just too slim. Combine slim margins with having so many mortgages locked into fixed interest rates at historic lows – about 95% of new and refinanced mortgages have been fixed over the past two years (source: Mortgage Bankers Association) – and a predicted loss of mortgage origination revenue to the tune of a -37% decline from last year, and you’ve got a recipe for a great deal of stress in the financial services industry. In the Great Recession, if the Treasury and Federal Reserve Board hadn’t bailed out the banks, few would still be in business. Many brokerages (Bear Stearns, Merrill Lynch, Smith Barney, etc.) were absorbed into the banks to prevent them from going belly-up. Investors still lost the majority of their equity investment, and if they were invested in Lehman Bros., they lost all of it. A complete meltdown is not expected to happen this time because analysts point out that credit quality is good and unemployment is at historic lows. However, “pain” can be very broadly spread in a declining market. Losing money in a retirement plan takes down your assets to debt ratio, and your credit score along with it. I’ll give you a brief tutorial below on some of the issues happening today that are putting bank stocks under pressure. If you’d like to receive our Bank or Brokerage Stock Report Card, simply email [email protected] with the name of the Stock Report Card that you are interested in. Here are some of the stress points in the economy and banking sector Inverted Yield Curve Massive Debt & Leverage High Valuations Money Market Fund Risk Russian Exposure And here is additional Information on Each Point.. Inverted Yield Curve The yield curve inverted again on April 4, 2022. Inverted yield curves are almost 100% associated with recessions. It indicates that the bank’s net interest margin is squeezed or negative. In 2020, Paul and Zhu wrote, “Banks’ net interest margins have been falling at the same time as compensation for taking on duration risk has declined over the past three decades.” That scenario is negative for banking revenue and net income. Massive Debt & Leverage Low or negative-yielding, high-risk, long-term bonds are a much bigger issue than many fixed-income investors are aware of. Banks have means for managing a lot of this risk, through CLOs and by selling bonds to investors. However, it doesn’t wipe the slate clean, particularly when over half of the S&P500 is at or near junk bond status (including a lot of banks and brokerages). A peak at the Asset Bubble chart below gives you the stark reality of debt and leverage in the U.S. today.  Consumer debt is higher than it has ever been, as are corporate and public debt and loans. Additionally, 25-40-year-olds are spending between 35-50% of their income on housing. The Feds are attempting to contain inflation while keeping the job market strong. However, if layoffs start occurring, consumer debt and leverage could become a big problem for people, products and anyone who loaned money to them.  High Valuations: Low Interest Rates Create Asset Bubbles The S&P500 is down -15% from its January 2022 high of 4818. However, as you can see from the chart below, stock prices are still very expensive – even higher than they were in the Dot Com Recession, when the NASDAQ Composite Index dropped 78%. Banks are vulnerable to equity losses.  According to the Federal Reserve Financial Stability Report released in May of 2022, “With valuations at high levels, house prices could be particularly sensitive to shocks.” No one is predicting a Great Recession type calamity. However, if you purchased your home recently, it’s worth it to make sure that you haven’t stretched the budget too thinly. It’s equally important to be aware that there are still 1.3 million homes that are severely underwater – even with home prices at all-time highs. Even if everyone pays their mortgage on time, the slowdown in mortgage originations will have a negative impact on mortgage revenues. Money Market Fund Risk Money Market Funds have seen their assets decline since 2020. Since these funds are “runnable,” they are a “structural vulnerability.” This is something that the Federal Reserve Board has been watching closely. They have a Repo Facility in place to help, which is getting tapped at unprecedented levels (click to see). Many investors are not aware that money market funds can lose money, and that they have redemption gates and liquidity fees. MMFs were a pretty big problem in the Great Recession, and could be a major issue if the current equity downtrend continues. If you’d like to know more about the risks in money market funds, be sure to read the “What’s Safe” section of The ABCs of Money. Russian Exposure JP Morgan Chase was often thought of as the bank that raised capital for Russian companies. JPMorgan and Goldman Sachs stated in March 2022 that they were going to exit the country. That means that the 2nd quarter earnings could start reflecting the exit. Citigroup has a bank in Russia. Citi warned that their exposure to Russia amounted to about $10 billion (source: Reuters). Citi’s stock is down 36% -- having plunged more than twice as far as the general market and the company’s banking competitors. Insurance Companies, Mortgage Banks and Hedge Funds Most of the issues discussed for the mega, multinational banks are even more problematic for the independent mortgage banks, insurance companies and hedge funds. Mortgage banks are losing revenue and having their profit margins squeezed. Insurance companies (do you have an annuity?) and hedge funds have a high amount of leverage and are very vulnerable to stock market plunges. Bottom Line In bear markets, bank stocks are as vulnerable as other equities, as is their dividend. If they don’t pass the Federal Reserve Stress Tests, they are required to cut dividends and suspend share buybacks. (Wells Fargo had this happen in the Pandemic Recession.) When dividends are cut, share prices plunge. Also, the higher the dividend, the higher the risk. Wells Fargo and Citigroup pay the highest dividends in the banking industry right now, and that’s a mere 2.0% and 3.77%, respectively. Now that you know bank stocks can lose as much as other stocks, what’s your best game plan? Proper diversification with regular rebalancing (something we teach at our Financial Freedom Retreats). You can read about it in The ABCs of Money. You can join us for the June 10-12, 2022 Online Retreat. Or you can email [email protected], if you’d like help understanding exactly what you own, how much you are at risk of losing, and what a better plan looks like. If you're interested in learning stock and 21st Century time-proven investing strategies for protecting your wealth and managing the downturn from a No. 1 stock picker, join us for our June 10-12, 2022 Financial Freedom Retreat. Email [email protected] or call 310-430-2397 to learn more and to register. Click on the banner ad below to discover the 18+ strategies you'll learn and master.  Join us for our Financial Freedom Retreat. June 10-12, 2022. Email [email protected] to learn more. Register with friends and family to receive the best price. Click for testimonials & details.  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Apple Podcast. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Beyond Meat: Rare or Burnt? Netflix Streaming Wars End in a Bloodbath. Elon Musk Sells $23 Billon in Tesla Stock and Receives $23 Billion in Options. Are You Gambling With Your Future? ESG Investing: Missing the E. Moderna & Biotech Trade at 2-Year Lows. Bitcoin Crashes. Crypto, Bold and Stocks All Crash. The Economy Contracted -1.4% in 1Q 2022. The Dow Dropped 2000 Points. Is Plant-Based Protein Dying? Should You Sell in April? The U.S. House Decriminalizes Cannabis Again. Chinese Electric Vehicle Market Share Hits 20%. The Risk of Recession in 6 Charts. High Gas Prices How Will Russian Boycotts Effect U.S. Multinational Companies? Oil and Gas Trends During Wartime Russia Invades Ukraine. How Have Stocks Responded in Past Wars? Zombie Companies. Rescue, Rehab or Liquidate? Spotify: Music to my Ears. Cannabis Crashes. 2022 Crystal Ball in Stocks, Real Estate, Crypto, Cannabis, Gold, Silver & More. Interview with the Chief Investment Strategist of Charles Schwab & Co., Inc. Stocks Enter a Correction Investor IQ Test Investor IQ Test Answers Real Estate Risks. What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed