Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

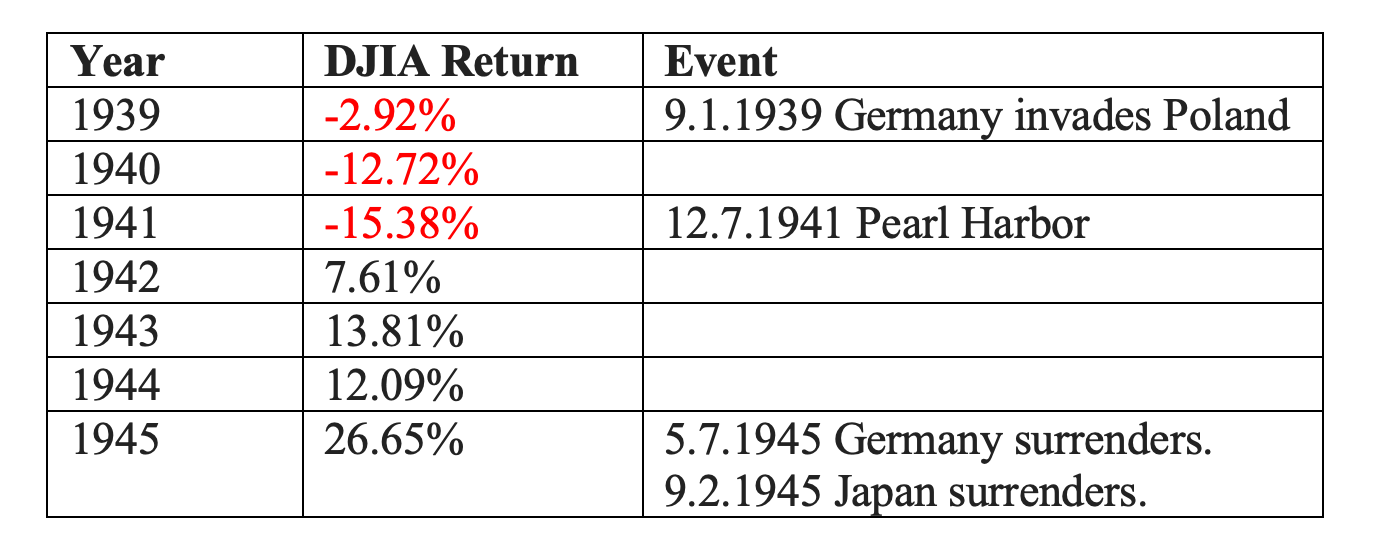

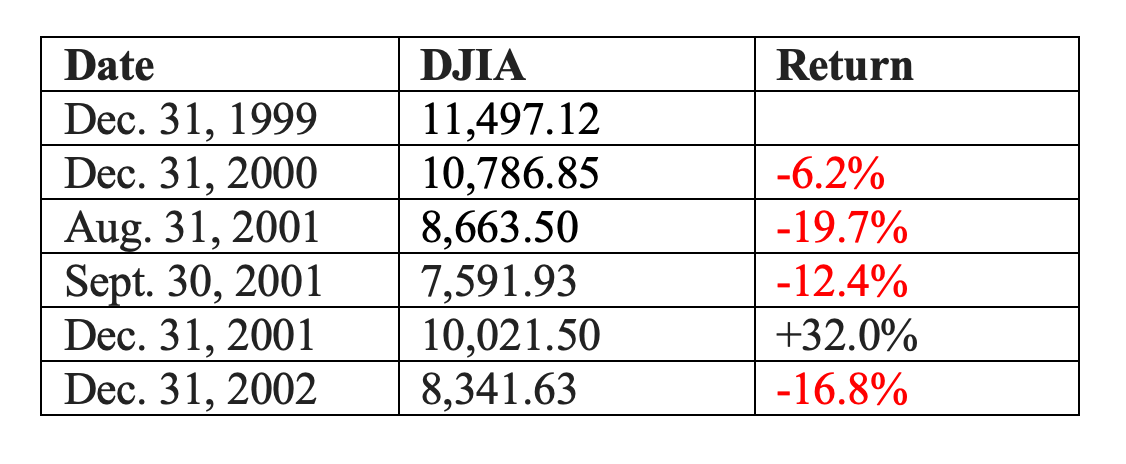

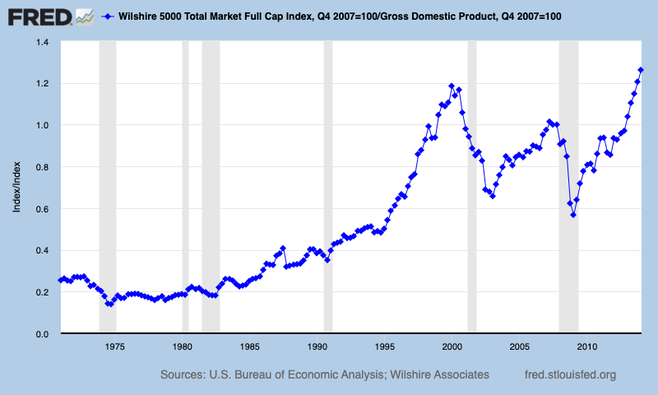

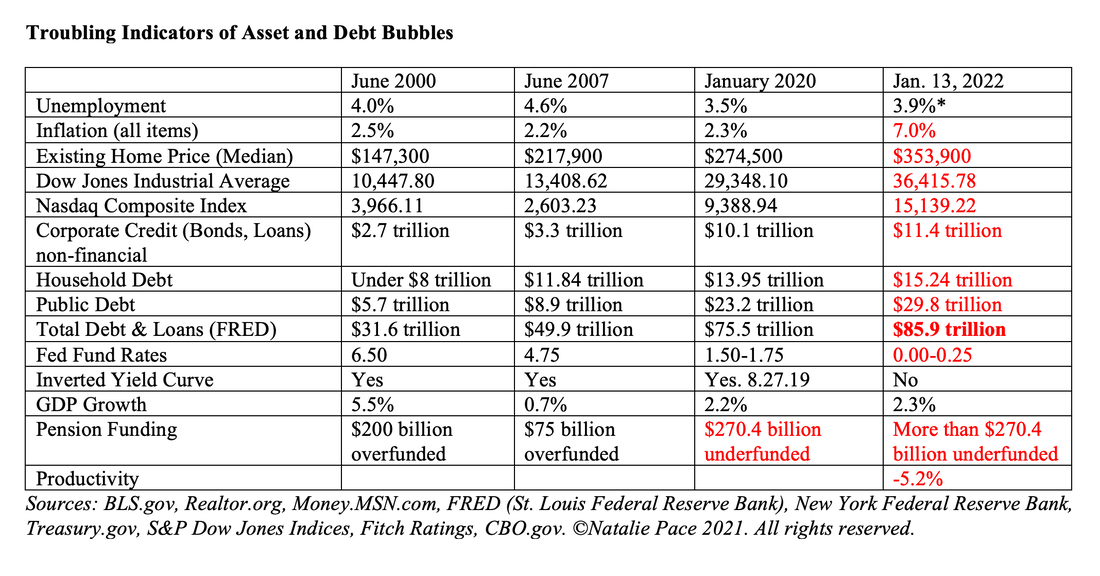

Ukrainian dance duo Oleksandr Ivanov and Ilona Slugovina. Multiple world and European champions in wheelchair dance. Masters of sports of international class. Berezil Sports Club, Kyiv, Ukraine. Photo by Ar4en. Wiki Commons License. Used with permission. Putin made good on his threats and invaded Ukraine last night. The Dow Jones Industrial Average started the day down over -800 points. After the U.S. announced sanctions, the markets recovered. The Dow rose 92 points (0.28%). The NASDAQ Composite Index posted a gain of 3.35% (436 points). However, the market, similar to wars, is not something that is won in a day, but over time. The conflict isn’t going to disappear. So, what’s your best strategy? How did stocks behave in past periods of bloodshed and conflict? Attacks, particularly those that are unexpected, are definitely a market driver, especially in the near-term. Usually there is a drop. (Today there was an unexpected rally; we’ll see how long that lasts.) The stock market was closed for four trading days in an attempt to calm investors after 9/11, and there was still a sell-off on September 17, 2001, when the market opened. (That’s not all there was to the story. Keep reading.) Over the past 24 hours, I’ve seen a flurry of pundits blogging and blabbing about wartime market statistics. Some of the numbers quoted are simply wrong. Others have been shaved to support whatever message they wish to convey. (I’m going to let you see the data for yourself below.) A lot of media and broker-salesmen are going to be pointing to overall market gains in attempt to calm roiled nerves into accepting their premise that you should just Buy & Hold. However, is that really the best strategy today? As one example, Fortune just published an article writing that “from 1939 until the end of the war in late 1945, the Dow saw increases of 50%, more than 7% per year.” The cumulative gains between the beginning of 1939 and the end of 1945 were actually only 36%, for annualized gains of 5.14% (source: FRED). (Not sure where the Fortune writer is getting his data.) To get to that sum, however, you have to overlook pretty steep losses between 1939 and 1941. The simple statement that there were gains over the period doesn’t reflect what people experienced at the time, as the chart below indicates.  Data provided by S&P Dow Jones Indices. If you lose a third of your wealth over a 3-year period, you might lose your home. Your credit score plunges, which increases your cost of borrowing. You might have to take on debt to make ends meet. You can’t buy low at the bottom. You don’t have any money. In fact, when the bull market finally comes, you are hoping and praying that you’ll make up losses, rather than enjoying the gains. As I averred above, the stock market plunge of the Dot Com Recession and the terrorist attack on 9/11 are often misrepresented. Between December 31, 1999 and August 31, 2001, the Dow Jones Industrial Average dropped from 11,497.12 to 8,663.50, for losses of -24.6%. The correction was already quite steep before 9/11. After a bounce up to 10,021.50 at the end of 2001, the DJIA slid again in 2002, ending the year at 8,341.63 – just -3.7% lower than the low in August of 2001 (before the terrorist attacks on the Twin Towers).  Data provided by S&P Dow Jones Indices. The losses of the NASDAQ Composite Index between the highs of March 9, 2000 (5,046.86) and Oct. 10, 2002 (1,150), were even more severe, at -77.2%. Why did the stock market correction happen before 9/11? Was there another factor at play? Can it help us to understand where we are today? In 2000, stock prices were very bubblicious. If we refer to the Buffett Indicator, which measures the total value of all publicly traded stocks against GDP, Dot Com stocks were the most expensive in history, outside of one other time – today. Stocks were very pricey in 2007, too, a time of real estate and stock investor euphoria that ushered in the Great Recession.  Recessions are indicated by a gray bar. There are a few key differences between the Dot Com Recession, the Great Recession and today, which were all periods of elevated asset prices. Before the Dot Com and Great Recessions, there was room for the Federal Reserve Board to cut interest rates to spark borrowing and economic growth to try and lift us out of the market troughs. Today, interest rates are at rock-bottom, and have to rise to combat inflation. The Federal Reserve Board will try to negotiate a “soft landing,” to raise rates without sparking a recession. However, elevated asset prices and the invasion of Ukraine present complications that could make that difficult. Market returns are typically lower when the tightening cycle begins, and can be negative if interest rates rise too rapidly. In short, 2022 was unlikely to experience anything close to 2021’s 27% market rally in the U.S. before Russia invaded Ukraine. Debt was high before the Great Recession. Today it is astronomical. Debt and leverage were already elevated before the pandemic, and then shot into the Nethersphere when trillions were printed up to help states, cities, consumers and businesses survive the lockdowns. Now, while GDP growth is still strong enough, is when we want to start reducing the debt load. The Federal Reserve unloaded all of the bonds they had purchased in early 2020 by 2021, and announced that they will start reducing their Treasury and asset-backed security holdings this year. The Beltway has had difficulty agreeing on how to balance the budget and put the U.S. on a more fiscally responsible path.  Another way of looking at today’s world, while also factoring in the harsh and heartbreaking backdrop of the Ukraine Crisis, is that the 21st Century has been marked by asset bubbles that present a different type of economy than existed in the last century. Most wartime events get folded into an average annualized gain over XYZ period, but are actually a rollercoaster, often with a severe two years or more of losses close to the inception of the war or attack. The elevated stock prices of the Dot Com Era ushered in sharper declines than were experienced during Pearl Harbor, World War II and even the Vietnam War. That’s one of the reasons why Buy & Hope worked better in the 20th Century and has been a Wall Street rollercoaster in the 21st. During wartime and periods of elevated stock prices, Modern Portfolio Theory with regular rebalancing works better than Buy & Hold. Our easy-as-a-pie-chart investing, with regular rebalancing, earned gains in the Dot Com and the Great Recessions and has outperformed the bull markets in between. So, if you are a Buy & Hope investor, it’s important to read between the lines of rhetoric, understand the true trends, and consider adopting a strategy that works in a 21st Century world marked by overvalued equities, unprecedented leverage and deep downturns. If you’d like to see the charts of past war-time shocks to the stock market, lined up with the average P/E of the day, just email [email protected]. You can watch my videoconference on the Ukrainian Crisis, which features 5 things every Buy & Hold investor must do now and 3 essential strategies for Pie Chart Investors, at YouTube.com/NataliePace. (If you don't know the difference, you'll learn in the free videoconference.)  Join us for our St. Patrick's Weekend Financial Empowerment Retreat. March 18-20, 2022. Email [email protected] to learn more. Register by Monday, February 28, 2022, to receive the best price. Click for testimonials & details. Other Blogs of Interest Zombie Companies. Rescue, Rehab or Liquidate? Spotify: Music to my Ears. Cannabis Crashes. 2022 Crystal Ball in Stocks, Real Estate, Crypto, Cannabis, Gold, Silver & More. Interview with the Chief Investment Strategist of Charles Schwab & Co., Inc. Stocks Enter a Correction Investor IQ Test Investor IQ Test Answers Real Estate Risks. What Happened to Ark, Cloudflare, Bitcoin and the Meme Stocks? Omicron is Not the Only Problem From FAANNG to ZANA MAD MAAX Ted Lasso vs. Squid Game. Who Will Win the Streaming Wars? Starbucks. McDonald's. The Real Cost of Disposable Fast Food. The Plant-Based Protein Fire-Sale What's Safe in a Debt World? Inflation, Gasoline Prices & Recessions China: GDP Soars. Share Prices Sink. The Competition Heats Up for Tesla & Nio. How Green in Your Love for the Planet? S&P500 Hits a New High. GDP Should be 7% in 2021! Will Work-From-Home and EVs Destroy the Oil Industry? Insurance and Hedge Funds are at Risk and Over-Leveraged. Office Buildings are Still Ghost Towns. Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. 2021 Company of the Year Almost 5 Million Americans are Behind on Rent & Mortgage. Real Estate Hits All-Time High. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Videoconferencing in a Post-Pandemic World (featuring Zoom & Teladoc). Sanctuary Sandwich Home. Multigenerational Housing. Interview with Lawrence Yun, the chief economist of the National Association of Realtors. 10 Budget Leaks That Cost $10,000 or More Each Year. The Stimulus Check. Party Like It's 1999. Would You Pay $50 for a Cafe Latte? Is Your Tesla Stock Overpriced? 10 Questions for College Success. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. Why Are My Bonds Losing Money? The Bank Bail-in Plan on Your Dime. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors.  About Natalie Pace

Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed