Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

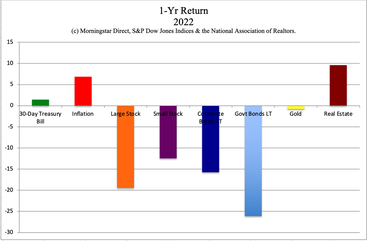

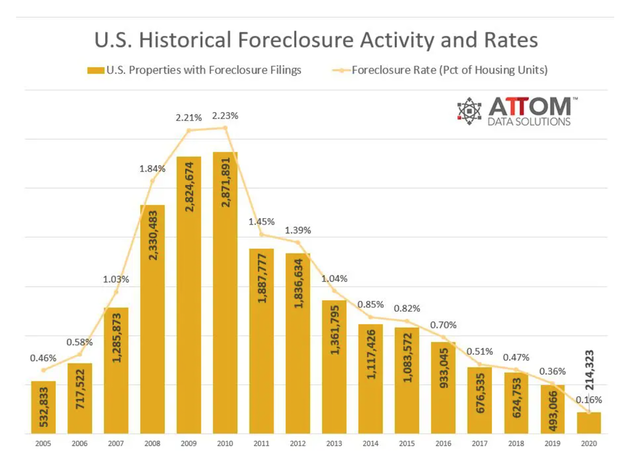

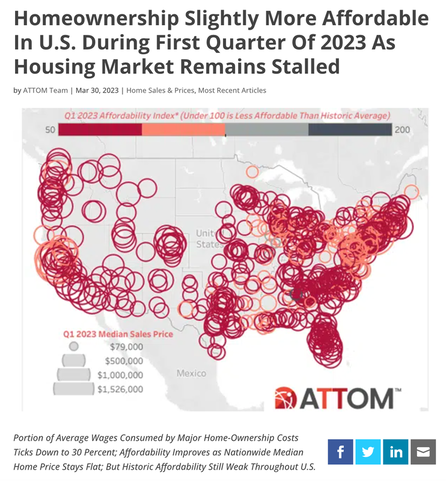

The Debt Ceiling Crisis: What is at Stake? According to Treasury Secretary Janet Yellen, the Debt Ceiling must be suspended or raised by June 1, 2023 to avoid a default. Given that Memorial Day weekend is at the end of this month, that means that Congress must resolve the matter by Thursday, May 25, 2023, if members want to go home for the holiday. Wall Street believes they will, though a bipartisan deal has yet to materialize. Congress has become infamous for last-minute deals, so there will be no nail biting. Tuesday, May 30, 2023, will either bring a sigh of relief, or, as JP Morgan CEO Jamie Dimon puts it, a “catastrophic” panic in stock and Treasury markets. (A Relief Rally is not expected with stocks trading fairly high and a recession on the horizon.) Since Main Street has little say in the matter, it’s easy to want to just “wait and see.” However, there are steps we can all take to protect our wealth from any crisis that might come in 2023, whether it is a Debt Ceiling debacle, a recession or more bank failures. Below are ways to protect our: · Retirement Plan · Cash · Budget · Home, and · Future And here is additional information on each front. Our Retirement Plan: 401(k) or RSP The financial chaos that would ensue if the United States defaults on its financial obligations for the first time in U.S. history would be alarming, and the contagion could easily spread worldwide. Stocks are still very strong in the U.S. because investors are anticipating that the debt ceiling crisis will be resolved with a suspension or a raise that is sufficient enough to get us through the next election.  Source: MSN.com. copyright 2023 Microsoft. Used with permission. If that is not the case, investors are likely to sell stocks and the Treasury market could freeze up. (This happened in the Great Recession.) 21st Century recessions and bear markets tend to be terrible. The S&P500 dropped 34% in just four weeks during the pandemic. The Dow Jones Industrial Average sank 55% in the Great Recession, and took years to earn back the losses. The NASDAQ Composite Index plunged 78% in the Dot Com Recession, and took 15 years to crawl back to even. That’s quite a rollercoaster, where investors spend most or all of the bull market earning back losses – with the exception of the pandemic, which is an anomaly. As we get closer to retirement, we simply can’t afford to suffer those kinds of losses. We don’t have the time to make them up again. However, even if we are just now entering the workforce, it’s important to protect at least a portion of our wealth from losses. A general rule of thumb is to always keep a percentage equal to our age safe, not invested in stocks, stock funds or equities, and to overweight an additional amount safe in times of economic turmoil (such as is happening today). In 2023, we are overweighting 20% additional safe in our sample nest egg pie charts. The problem today, however, is that it is difficult to get safe in any paper asset. Typically, you’d be safe by investing in investment grade bonds. However, long-term government bonds lost more than the S&P500 in 2022.  So, we must know what is safe in a Debt World. (We spend one full day on how to get safe in our Investor Empowerment Retreats. The next one is June 10-12, 2023.) While tricky, there are a few things that we can do (which are explained in greater detail at the retreat). 2023 Bond Strategy Here are a few tips that will assist us in protecting the safe side of our nest egg. 1. Terms short 2. Creditworthiness high 3. Ladder 4. FDIC-insured cash 5. No concentration in any one bank, brokerage or account (including 401k or RSP) 6. Don’t put all of your eggs in any one basket (#5 emphasized) Most employer retirement plans have only a few options on the safe side to choose from. Selecting the safest option requires a forensic analysis. However, there is another tool that can help. Setting up individual, self-directed retirement accounts, in addition to our employer-based one, offers greater freedom and control over our money. If you would like to personalize your own pie chart, email [email protected] with “free web apps” in the subject line. We are happy to send you these free tools to assist you on your journey to greater financial freedom. Our Cash Investors and bondholders have lost money on the banks that have failed so far. The shares of Silicon Valley Bank, Signature Bank and First Republic Bank are worthless. However, depositors have been protected – even uninsured depositors – under a special exclusion, called the Systemic Risk Exclusion. In the case of First Republic Bank, JPMorgan assumed responsibility for all of the depositors, rather than having the FDIC impose the systemic risk exclusion. It is not guaranteed that that exclusion will be used going forward because a special assessment on banks is required to cover the costs when it is imposed. It is also not guaranteed that the banking crisis is over yet. Therefore, the best protection is still FDIC-insured cash levels, rather than relying upon exemptions to safeguard our uninsured deposits. Of course, for big businesses this gets quite tricky. Mega multinational corporations stash cash all around the world, in various types of fixed-income vehicles. Canadian and Australian banks have a higher credit rating than the U.S. banks. Ireland has become a capital hub for U.S. multinational corporations. Anyone who is worth a few million or less can protect the “safe” side of their wealth through a carefully designed plan that includes short-term, creditworthy bonds and FDIC-insured cash. (If you’re interested in a forensic analysis of your wealth plan through my private coaching, email [email protected] for pricing and information.) It’s important to be the boss of our money and to know exactly what assurances and risks are spelled out in the fine print of all of our cash and investment products. Our Budget Financial chaos and recessions are huge problems for our personal budgets. Prices fall, which would be a welcome end to inflation. However, what is good for consumers is a problem for businesses, which results in layoffs. In the Great Recession, unemployment soared to 15% for some cohorts.  So, our budget is at risk because our employment stability is at risk, which can be further exacerbated if our retirement plan loses a great deal, and the value of our home drops. Home prices and stock prices plunged in the Dot Com and the Great Recession. This can also put our home at risk. Our Home As you can see in the chart below, over 20 million homes were foreclosed on during the Great Recession.  If you purchased a home that you can afford at a price that was reasonable, and have a low-interest fixed rate, then you’re in a good seat, particularly if your job is stable. However, with consumer debt at all-time high, and a lot of folks with buyer’s remorse, especially those who purchased more recently, and more than 30% of a lot of folks’ income going towards housing, this does not bode well for the real estate market in the next recession. Real estate prices are very high, according to various measures, from the May 2023 Financial Stability Report to unaffordability measures and price histories. Since prices tend to plunge in bubbles, now is the time to make sure that you do a full analysis of your shelter costs, your home affordability, and your resilience to withstand weakness. It’s a very good idea to think outside the box and to have a recession-proof plan in place before trouble hits.  Real estate prices are already down 10% nationwide. However, that is much better than the performance of stocks and bonds. Hard assets tend to hold their value better when there is too much paper money floating around. So, even if it’s time to downsize, selling is just one option of many that we should consider. If we purchased recently at a very high price, or if we’re not happy with our real estate purchase for another reason, then, the sooner we identify the best plan, the better. As credit conditions become tighter, the options to extricate ourselves from a bad situation become scarcer. The real estate section of The ABCs of Money presents case studies and tips to help us to think creatively for solutions that could protect our wealth, provide shelter and keep more of our money in the family. Our Future The best protection against an uncertain tomorrow is to adapt our entire financial life for the challenges of the 21st century. The following tools will help. · The Thrive Budget® · Easy-as-pie-chart nest egg strategies® · Regular rebalancing, once, twice or three times a year · Knowing what is safe in a debt world · Knowing how to protect our cash at a time when banks are failing You can read about these strategies in my bestselling books. You can learn and implement them by attending our Financial Empowerment Retreat. The next one is June 10-12, 2023. This is very likely to be the last opportunity to attend our 3-day money makeover before October. Since September can be the worst performing month of the year, now is the perfect time to protect our wealth before we go on our summer vacation. If you would like more personalized attention, email [email protected] for pricing and information on my unbiased 2nd opinion and private coaching. Bottom Line Everyone is counting on a Debt Ceiling deal happening in time. If it doesn’t, the results are likely to be so dire that it is difficult to imagine, as it will impact stocks, Treasuries and markets around the world. However, even if a deal does materialize, with all of the debt and financial storms on the horizon, it’s a good idea to do a complete money makeover now, to ensure that our retirement plan, cash, budget, home and future are as secure as they can be. It’s always a great idea to fix the roof while the sun is still shining. Email [email protected] or call 310-430-2397 if you are interested in learning time-proven investing, budgeting, debt reduction, college prep, ESG and home buying solutions that will transform your life and heal our planet at our next Financial Freedom Retreat. We spend one full day on what's safe, helping you to protect your wealth and reduce money stress.  Join us for our Online Financial Freedom Retreat. June 10-12, 2023. Email [email protected] to learn more. Register by May 15, 2023 to receive the best price. Click for testimonials, pricing, hours & details.  Join us for our Restormel Royal Immersive Adventure Retreat. March 8-15, 2024. Email [email protected] to learn more. Register with friends and family to receive the best price. Click for testimonials, pricing, hours & details. Early Bird pricing ends May 30, 2023. There is very limited availability.  Natalie Pace. Photo by Marie Commiskey. Natalie Pace. Photo by Marie Commiskey. Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Apple Podcast. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Fiat. Crypto. Gold. BRICS. Real Estate. Alternative Investments. BRICS Currency. Will the Dollar Become Extinct? Empty Office Buildings & Malls. Frozen Housing Market. The Online Global Earth Gratitude Celebration 7 Green Life Hacks The Debt Ceiling. Will the U.S. Stop Paying Bills in June? Fossil Fuels Touch Every Part of Our Lives Are There Any Safe, Green Banks? 8 Fires the Federal Reserve Board Needs to Put Out. 7 Ways to Stash Your Cash Now. Lessons from the Silicon Valley Bank Failure. The 2 Best Solar Stocks Which Countries Offer the Highest Yield for the Lowest Risk? Rebalance By the End of March Solar, EVs, Housing, HSAs -- the Highest-Yield in 2023? Are You Anxious or Depressed over Money? Why We Are Underweighting Banks and the Financial Industry. You Stream all the Channels. Should You Invest, Too? NASDAQ is Still Down -26%. Are Meta & Snap a Buy? 2023 Bond Strategy Emotions are Not Your Friend in Investing Investor IQ Test Investor IQ Test Answers Bonds Lost -26%, Silver Held Strong. 2023 Crystal Ball for Stocks, Bonds, Real Estate, Cannabis, Gold, Silver. Tilray: The Constellation Brands of Cannabis New Year, New Healthier You Tesla's $644 Billion Fall From Mars Silver's Quiet Rally. Free Holiday Gift. Stocking Stuffers Under $10. Cash Burn & Inflation Toasted the Plant-Based Protein Companies Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Giving Tuesday Tips to Make Your Charitable Contribution a Triple Win. Is Your Pension Plan Stealing From You? The FTX Crypto Fall of a Billionaire (SBF). Crypto, Gold, Silver: Not So Safe Havens. Will Ted Lasso Save Christmas? 3Q will be Released This Thursday. Apple and the R Word. Yield is Back. But It's Tricky. The Real Reason Why OPEC Cut Oil Production. The Inflation Buster Budgeting and Investing Plan. No. Elon Musk Doesn't Live in a Boxabl. IRAs Offer More Freedom and Protection Than 401ks. Will There Be a Santa Rally 2022? What's Safe in a Debt World? Not Bonds. Will Your Favorite Chinese Company be Delisted? 75% of New Homeowners Have Buyer's Remorse Clean Energy Gets a Green Light from Congress. Fix Money Issues. Improve Your Relationships. 24% of House Sales Cancelled in the 2nd Quarter. 3 Things to Do Before July 28th. Recession Risks Rise + a Fairly Safe High-Yield Bond DAQO Doubles. Solar Shines. Which Company is Next in Line? Tesla Sales Disappoint. Asian EV Competition Heats Up. 10 Wealth Strategies of the Rich Copper Prices Plunge Colombia and Indonesia: Should You Invest? 10 Misleading Broker/Salesman Pitches. Why are Banks and Dividend Stocks Losing Money? ESG Investing: Missing the E. Bitcoin Crashes. Crypto, Gold and Stocks All Crash. The U.S. House Decriminalizes Cannabis Again. The Risk of Recession in 6 Charts. High Gas Prices How Will Russian Boycotts Effect U.S. Multinational Companies? Oil and Gas Trends During Wartime Russia Invades Ukraine. How Have Stocks Responded in Past Wars? 2022 Crystal Ball in Stocks, Real Estate, Crypto, Cannabis, Gold, Silver & More. Interview with the Chief Investment Strategist of Charles Schwab & Co., Inc. Stocks Enter a Correction What's Safe in a Debt World? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed