Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

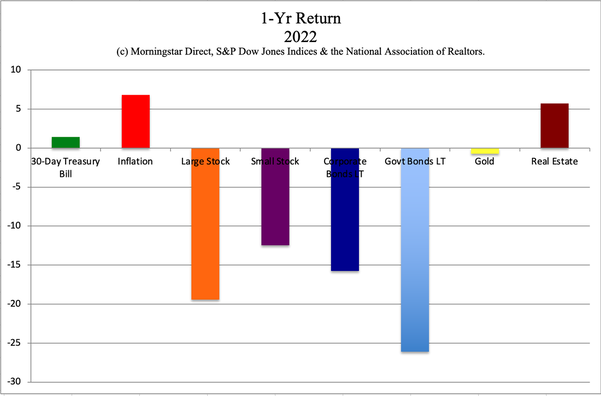

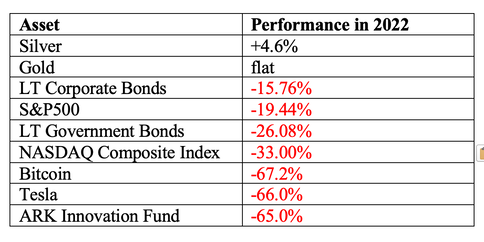

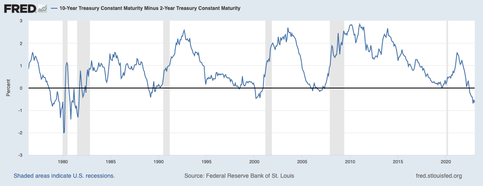

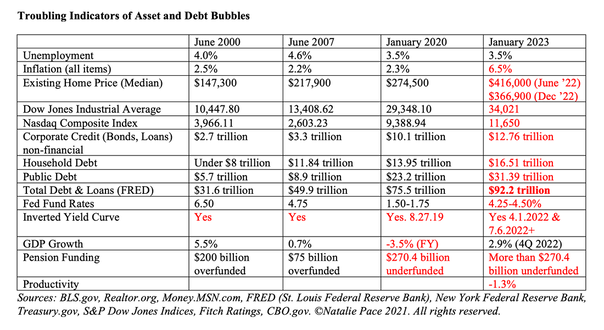

2023 Bond Strategy. Bonds are losing money. Countries face heightened exposure to corporate defaults. Sri Lanka and Pakistan are already seeking IMF bailouts. Risks include: Interest rate risk. Credit risk. Duration risk. Opportunity Costs. How can fixed income investors protect themselves? Includes a 5-Part 2023 Bond Strategy. Rising interest rates create opportunities for savers and fixed-income investors to finally earn a yield. However, there’s an overhang of legacy debt that resulted in U.S. long-term government bonds losing more than the S&P500 last year, at -26.08% and -19.44% respectively. Corporate bonds posted a miserable performance of -15.76%.  Sources: Morningstar Direct and MSN.com. copyright by Morningstar Direct and Microsoft. Used with permission. This makes investing in bonds and other fixed income assets very tricky. If you were in bonds or bond funds prior to 2022, it’s time to do a forensic audit of your holdings to weed out the losers. Particularly as we’re seeing signs of potential corporate debt distress. (We’ve been warning to steer clear of bonds since 2012. Investors weren’t being paid to take on the risk, plus bonds have been illiquid and negative-yielding for years now.) Corporate Distress The IMF warned yesterday that the rapid rise in worldwide corporate debt, combined with the soaring costs of borrowing money, has made countries vulnerable. According to the IMF, the risks of corporate defaults spilling over into the banking sector and creating financial instability is heightened in 2023 – to levels almost as concerning as we saw during the pandemic, when most banks suspended their corporate buybacks and some stopped paying dividends. In the blog entitled “Countries Should Act Now to Limit Rising Risks from Corporate Distress,” IMF researchers used AI to predict that “This build-up of risk in the corporate sector and a doubling of funding costs for even the safest issuers could pose serious problems for many economies and their financial systems.” Thirty-eight of the economies tracked by the IMF are at medium risk, and seven economies, mostly from Europe and Asia, are at high risk of systemic corporate distress. The high-risk countries are not all small developing world countries like Sri Lanka and Pakistan. Collectively they account for 21% of worldwide GDP. Unlike the pandemic, we won’t be printing up another $12 trillion to rescue everything. Instead, countries are being encouraged to find a way for failing companies to restructure, to decide which firms and industries need to be rescued, to “improve transparency of lenders’ assets and liabilities, refrain from further lending to firms that cannot pay existing debts, strengthen capital buffers, and conduct comprehensive stress tests.” Which countries are the most vulnerable? According to the IMF (in a February 2022 white paper), the developed world countries that are the most vulnerable to corporate debt are: Portugal, Norway, Greece, Spain, Iceland, New Zealand, Austria, Italy and the United States. The developing world countries with the most vulnerability are: Argentina, Vietnam, India, Kuwait, Pakistan, Oman, Sri Lanka, Nigeria, Tunisia, Indonesia, South Africa and Chile. (We took Chile off our Hot Country List in June of 2022. Click to access that blog.) After the IMF report, in summer of last year, Sri Lanka defaulted on its debt and has been in negotiations for a bailout since. Creditors have been asked (forced) to take a write-down. Pakistan asked the IMF for a bailout yesterday. The U.K. Gilt Crisis Great Britain was listed as having moderate risk to corporate debt. However, there was a Gilt Crisis in September of 2022. 10-year Gilt yields soared from 1% to 4%. The pound plunged below the U.S. dollar (for the first time in history). Things were quickly resolved by the Bank of England, and by giving Prime Minister Truss the boot. However, it is a reminder that crises can flare up without warning, even with large countries that are supposed to be better prepared for them. For this reason, it’s a good idea to diversify our “safe” holdings, and to understand the underlying credit risk and rating of any bank, corporation or country we are doing business with. (Again, we took Chile off our Hot Country List in June of 2022. Click to access that blog.) Additional Risks in the 2023 Bond Market Inflation Inflation has forced central banks to tighten up the money supply and slow down the economy in order to prevent sky-high prices from becoming entrenched. In 2022, the U.S. Fed Funds rate went from 0% to 4.5% in just one year. The FOMC is expected to raise rates by another 25 basis points today (Feb. 1, 2023), with a total rise of 50 basis points in 2023. While there are some signs of inflation abating, few are expecting any interest rate cuts in the U.S. this year. Companies will not be able to live on borrowed time and money to make ends meet in 2023. Inverted yield curve As you can see in the attached chart below, inverted yield curves are 100% correlated with recessions over the past half century. The gray lines are the recessions. Recessions tend to make everything more challenging.  Money Market Funds When corporate distress spills over into the banking industry (the lenders), it can become a crisis, such as happened in the Global Financial Crisis of 2008. During the Great Recession, banks were bailed out by the taxpayers to prevent a catastrophic economic disaster. This time around, banks and financial services companies are protecting their liquidity through redemption gates and liquidity fees in their money market funds. However, will that be adequate if corporate defaults start to pick up? Also, money market funds can lose value (as any fund can). So, is this where you want your safe money to reside? (Better double-check your retirement and brokerage accounts.) By the time redemption gates, liquidity fees and breaking the buck make headlines, the tools might already be in use. While we’re all hoping for the elusive “soft landing,” this is not guaranteed, which is why the IMF is encouraging countries to do even more to protect their banks. You can get more information on FDIC, SPIC, Money Market Funds and More in my blog (click to access). Credit Risk Over half of the S&P 500 is at or near junk-bond status. Ford is classified as a junk bond. Many corporations borrow money from investors for a very long term, sometimes even longer than we’ll live. Because interest rates jumped so high in 2022, those long-term holdings that are paying less than short-term Treasury bills lost a great deal of value. There is a lot more credit risk in long-term bonds than most fixed income investors are aware of. It’s important to know the credit rating, the revenue growth or decline rate, the debt-to-equity ratio, and the prognosis of how the company, state or country can fare in a recession, before committing to lending our money. If the entity already has our money, it might be worth it to consider selling out of the position, while there is still enough liquidity to do so. Each holding will have a different risk/reward rating and should be examined separately. (I offer an unbiased 2nd opinion. If you’re interested, email [email protected] for pricing and information.) Interest Rate Risk There is an inverse relationship between interest rates and bond values. When interest rates rise, the value of the bond goes down. The faster the rise, the more severe the plunge. That is why we saw such losses in long-term debt last year and why the U.K. had a gilt crisis. Interest rates are predicted to rise again in 2023, albeit at a slower pace. So, interest rate risk remains a headwind for bonds in 2023, particularly for the most vulnerable corporations, with the slowest revenue growth and the highest debt load. Duration Risk. Mid-term and long-term bonds carry heightened risk in a Debt World, particularly as the world braces for a potential recession in 2023. It’s important to keep the terms short and the creditworthiness high. Asset Bubbles Here is a chart that indicates all of the debt levels in the United States, where the total debt and loans exceeds $92 trillion. As you can see, debt is extremely elevated in every corner.  2023 Bond Strategy So what is a good strategy for bonds in 2023? 1. Keep the Terms Short 2. Keep the Creditworthiness High 3. Ladder Maturities 4. Consider Safe, Income-Producing Hard Assets That You Purchase for a Good Price 5. Diversify. Don’t Put All of Your Money in Any One Bank, Corporation or Country The devil is in the details. What’s safe (including your bond strategy) is examined extensively on day three of our Investor Empowerment retreats. There are many opportunities that are outside the mainstream where we can get a great return on investment, without taking on much risk. The next online retreat is April 22-24, 2023. If you register by Feb. 8, 2023, you receive the lowest price. These strategies were also covered in our Bond Master Class (held last Saturday). If you would like access to the recording, email [email protected] for pricing and information. Bottom Line The “safe” side of our investment strategy is not supposed to lose money. Long-term government bonds lost more value than the S&P 500 in 2022. Corporate bonds lost a lot, too, and are putting some countries at risk of financial instability. So if we’re trusting that someone else is protecting our wealth, without knowing the details of what we own and why, chances are very high that we lost money in 2022 and remain at risk of further capital loss in 2023. Any broker/salesman who promises us a 7-10% annualized return on our money is not being forthright with us about the risk of capital loss (or the losses incurred in 2022). In a recession or bear market, it’s important to limit our losses. (Almost every investment lost money in 2022. 2023 isn’t predicted to be any better.) In a Debt World, we must adhere to Will Roger’s advice. He once said, “I’m more concerned with the return of my money than the return on my money.” (Keep the terms short and the creditworthiness high.) Again, I offer an unbiased second opinion on your wealth plan and bond strategy. It’s unbiased because I did not sell financial products. My only incentive is to provide you with the information you need to be the boss of your money. If you are interested in an unbiased, second opinion, email [email protected] for pricing and information. Email info @ NataliePace.com or call 310-430-2397 if you are interested in learning time-proven investing, budgeting, debt reduction, college prep and home buying solutions that will transform your life at our next Financial Freedom Retreat.  Join us for our Online Financial Freedom Retreat. April 22-24, 2023. Email [email protected] to learn more. Register by Feb. 8, 2023 to receive the best price (value $200). Click for testimonials, pricing, hours & details.  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Apple Podcast. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Emotions are Not Your Friend in Investing Investor IQ Test Investor IQ Test Answers Bonds Lost -26%, Silver Held Strong. 2023 Crystal Ball for Stocks, Bonds, Real Estate, Cannabis, Gold, Silver. Tilray: The Constellation Brands of Cannabis New Year, New Healthier You Tesla's $644 Billion Fall From Mars Silver's Quiet Rally. Free Holiday Gift. Stocking Stuffers Under $10. Cash Burn & Inflation Toasted the Plant-Based Protein Companies Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Giving Tuesday Tips to Make Your Charitable Contribution a Triple Win. Is Your Pension Plan Stealing From You? The FTX Crypto Fall of a Billionaire (SBF). Crypto, Gold, Silver: Not So Safe Havens. Will Ted Lasso Save Christmas? 3Q will be Released This Thursday. Apple and the R Word. Yield is Back. But It's Tricky. The Real Reason Why OPEC Cut Oil Production. The Inflation Buster Budgeting and Investing Plan. No. Elon Musk Doesn't Live in a Boxabl. IRAs Offer More Freedom and Protection Than 401ks. Will There Be a Santa Rally 2022? What's Safe in a Debt World? Not Bonds. Will Your Favorite Chinese Company be Delisted? 75% of New Homeowners Have Buyer's Remorse Clean Energy Gets a Green Light from Congress. Fix Money Issues. Improve Your Relationships. 24% of House Sales Cancelled in the 2nd Quarter. 3 Things to Do Before July 28th. Recession Risks Rise + a Fairly Safe High-Yield Bond DAQO Doubles. Solar Shines. Which Company is Next in Line? Tesla Sales Disappoint. Asian EV Competition Heats Up. 10 Wealth Strategies of the Rich Copper Prices Plunge Colombia and Indonesia: Should You Invest? 10 Misleading Broker/Salesman Pitches. Why are Banks and Dividend Stocks Losing Money? ESG Investing: Missing the E. Bitcoin Crashes. Crypto, Gold and Stocks All Crash. The U.S. House Decriminalizes Cannabis Again. The Risk of Recession in 6 Charts. High Gas Prices How Will Russian Boycotts Effect U.S. Multinational Companies? Oil and Gas Trends During Wartime Russia Invades Ukraine. How Have Stocks Responded in Past Wars? 2022 Crystal Ball in Stocks, Real Estate, Crypto, Cannabis, Gold, Silver & More. Interview with the Chief Investment Strategist of Charles Schwab & Co., Inc. Stocks Enter a Correction Investor IQ Test Investor IQ Test Answers What's Safe in a Debt World? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed