Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

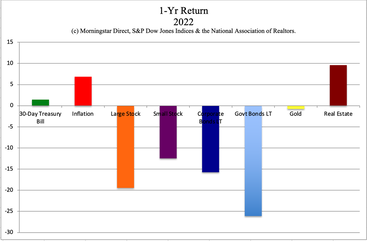

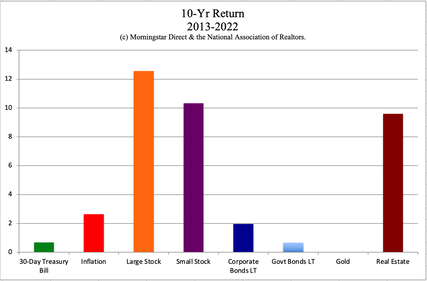

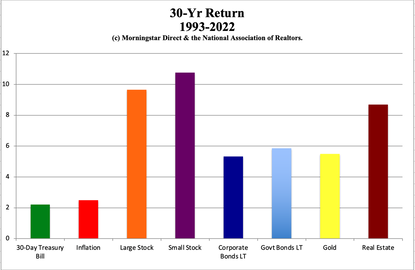

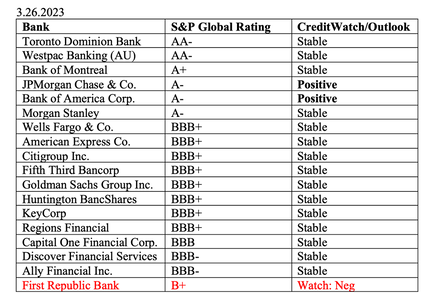

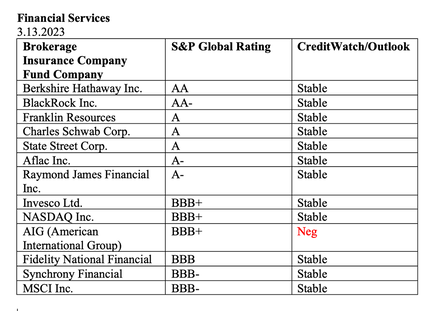

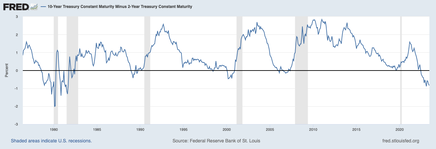

Bonds Lost More Than Stocks Last Year Long-term government bonds lost more than the S&P500® last year. This is important for us to know for many reasons, many of which are outlined below. Bond losses are central to the recent bank failures. The big banks have hedged their losses. However, regional and smaller banks could continue to experience challenges. As Lawrence Yun, the chief economist of the National Association of Realtors, wrote in a press release on May 3, 2023, the “fast rate hikes by the Fed have upended the balance sheets of many small regional banks. They are becoming zombie-like banks, unable to lend even to good businesses, as they are more concerned with balance sheet shuffling for survival.” Additionally, while banks can hedge themselves against losses and operate with nominal reserves and very low credit scores, neither one of those strategies are available for our personal household. Therefore, it’s critical for us to be ahead of the headlines in protecting our wealth, and in understanding what’s safe in a world where bonds lose more than stocks. When we wait for the headlines that a bank is in trouble or the economy is in a recession, it’s too late to protect our wealth. It’s a far better idea to fix the roof while the sun is still shining.  Source: MSN.com. (c) Microsoft. Used with permission. Here Are the Four Key Points We Will Cover in This Blog. The Safe Side of our Nest Egg Isn’t Supposed to Lose Money Why the Banks Failed Over Half of the S&P 500® is At or Near Junk-Bond Status (including Banks) Getting a Safe Yield is Tricky And here is additional information on each of these areas. The Safe Side of our Nest Egg Isn’t Supposed to Lose Money When we go to a financial planner, they often give us a risk tolerance test. (In our system, we use our age and market conditions as a guide, rather than risk tolerance, because emotions are not our friend in investing.) Based upon the results of that test, the broker/salesman will determine how much of your financial plan you should keep safe from losses. Traditionally, equities are more at risk, but they provide higher gains as you can see in the 10- and 30-year charts of returns below.   As an example, if you are 40 and you keep 60% safe because you’re conservative, or because you’re overweighting safe due to the risk of a recession, if the markets drop by half, which they have done in most 21st-century recessions, then your losses should be limited to just 20% or less. In most recessions, interest rates get cut and bonds perform very well. Those gains help to keep your wealth buoyant. Since 2022, with the rapid acceleration of interest rates, existing long-term bonds have lost a great deal of value. Bonds have been illiquid and negative-yielding for years. So the “safe” side of our wealth plan is not doing its job of protecting our principal. That has to do with both interest rate and credit risks. Why the Banks Failed We’ll talk about credit risk in the next point. Rapid increases in interest rates create interest rate risk. Banks that did not hedge against interest rate risk, such as the banks that failed, are vulnerable to having depositors withdraw their cash if/when the general public becomes concerned about the bank’s ability to stay afloat. Things have calmed down significantly since March because the Federal Reserve Board has set up a facility for qualified banks to get them through this period of unrealized bond losses. In the bank failures that have occurred so far, even noninsured depositors were protected. However, all of this happened under special provisions. There’s been no change to the FDIC policy, and we can’t tap the Fed’s help for our personal bond losses. Long-term bonds could outlive us, as many have 30-year terms or longer. So, waiting to get our money back could be a long, cold, low-FICO score winter. Therefore, it’s very important to take a serious look at the risk exposure on the “safe” side of our financial plan. Insurance companies that hold annuities, fund companies that sell us money market funds and other “safe“ products can be vulnerable, too. It’s very important to understand what is safe in a world where bonds are losing more than stocks. (I offer an unbiased second opinion that shows you the risks and protections of your current plan.) Here’s a link where you can read some of the comments that were made by the CEO of Silicon Valley Bank the week before it was seized by the FDIC and forced into bankruptcy. He wrote that the bank was “well capitalized.” As you can infer from his comments, the bank, insurance company, or fund company that wants to keep our business is not necessarily going to be forthright about the risks that we face. Those risks will, however, be found in the fine print, which is why it’s so important for us to know exactly what we own and why, rather than having blind faith that someone else is protecting our wealth for us. Over Half of the S&P 500® is At or Near Junk-Bond Status (including Banks) Over half of the S&P 500 is at or near junk-bond status. That includes a lot of banks and financial services companies as you can see in the charts below.   Banks, brokerages, insurance companies, private equity, and hedge funds – essentially all of the financial services industry – don’t do well in recessions. Recall the fate of AIG, Countrywide, Merrill Lynch, Lehman Bros., and Bernie Madoff, etc. Some of these companies, such as Merrill Lynch, were rescued through a merger. If you take a closer look at the bank ratings above, you’ll notice that the Canadian and Australian banks are rated higher than the U.S. banks. We’ve been underweighting the financial industry in the United States for a few years now. As with long-term bonds, you’re just not getting paid enough to take on the risk. Other more highly rated banks and countries are also providing a higher yield. Getting a Safe Yield is Tricky 1-year Treasury bills are paying a higher yield than 2-year. Both are paying a much higher yield than 10 or 30 year. When that happens, it’s called a Negative Yield Curve. As you can see in the chart below Negative Yield Curves are 100% correlated with recessions since 1980. (The grey areas indicate recessions.) As former Federal Reserve Board Chairman Ben Bernanke pointed out in a recent Morgan Stanley videoconference, “Economists are very bad at predicting recessions.“ He also noted that the yield curve is very good at predicting them. For that reason (and a few more), we are overweighting 20% additional safe, based upon market conditions.  Recessions are not announced until two quarters of negative growth have happened, and sometimes not even then, as we saw in 2022. Therefore, even if the U.S. economy does enter a recession in the second half of 2023 (as the Conference Board is predicting), the earliest we get the recession announcement will be at the end of January. Institutional investors are forward-thinking; they watch the data, not the headlines. That is why Main Street always gets caught up in such massive trauma and losses, after the whales have taken profits and the stock market has plunged. The Great Recession wasn’t officially announced until December 2008, after the Dow Jones Industrial Average had already lost over 45% (take another look at the chart at the top of the blog). Since the bottom was March 9, 2009 (6,547), most people were far closer to the bottom than the top when they became forlorn and wanted to stop the losses. Complacency abounded, even though there were economic storms on the horizon, in October of 2007, at the market high. Emotions are not our friend in investing. Again, when we wait for the headlines, we’re late. We might be feeling fairly complacent right now, even though the bank failures and Debt Ceiling Crisis are still fresh in our minds. We might be tempted to just “wait and see.” A better plan is always to be properly diversified and protected, and rebalance regularly to capture our gains. On Wall Street we call it, “Sticking to our knitting.” Bottom Line The “safe” side of our financial plan is there to preserve our wealth. It is not supposed to lose money. What can we do to determine if our plan has lost money or is at risk? At minimum, ask for a performance chart of your financial plan for the last 20 years, compared to the S&P500®. If your plan merely does with the S&P 500 does, then you are indeed exposed to a greater risk of losses than you might wish to be. Wisdom is the cure and the time is now to know exactly what we own and why, and to have a properly diversified and protected plan in place. You can learn about this at our online Investor Empowerment Retreat October 7-9, 2023. If you are interested in receiving an unbiased 2nd opinion before you go away on vacation, call 310-430-2397 or email [email protected] for pricing and information. Our unbiased 2nd opinion details exactly what you own, with color codes to show you what’s toxic in your portfolio, what’s great, and what should be better diversified. You will have a blueprint of how to get safe, protected, hot and diversified. Why is it unbiased? We don’t sell financial products. We have no incentive to sell you something that might lose money or that you don’t need. Our business model is financial education, providing the news, information, and education that Main Street investors need to thrive and live a richer life.  Join us for our Online Financial Freedom Retreat. Oct. 7-9, 2023. Email [email protected] to learn more. Register by June 30, 2023 to receive the best price and a complimentary private prosperity coaching session (value over $400). Click for testimonials, pricing, hours & details.  Join us for our Restormel Royal Immersive Adventure Retreat. March 8-15, 2024. Email [email protected] to learn more. Register with friends and family to receive the best price. Click for testimonials, pricing, hours & details. There is very limited availability, and you must register early to ensure that you get the exact room you want! This retreat includes an all-access pass to all of our online training for a full year for two!  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money was released on September 17, 2021. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Apple Podcast. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Tesla's Model Y is the Bestselling Car in the World. 2023 Company of the Year Sell in May and Go Away? Do Cybersecurity Risks Create Investor Opportunities? Writers Strike, While Streaming CEOs Rake In Hundreds of Millions Annually. I Lost $100,000. Investors Ask Natalie. Artificial Intelligence Report. Micron Banned in China. Intel Slashes Dividend. Buffett Loses $23 Billion. Branson's Virgin Orbit Declares Bankruptcy. Insurance Company Risks. Schwab Loses $41 Billion in Cash Deposits. The Debt Ceiling Crisis. What's at Stake? Fiat. Crypto. Gold. BRICS. Real Estate. Alternative Investments. BRICS Currency. Will the Dollar Become Extinct? Empty Office Buildings & Malls. Frozen Housing Market. The Online Global Earth Gratitude Celebration 7 Green Life Hacks The Debt Ceiling. Will the U.S. Stop Paying Bills in June? Fossil Fuels Touch Every Part of Our Lives Are There Any Safe, Green Banks? 8 Fires the Federal Reserve Board Needs to Put Out. 7 Ways to Stash Your Cash Now. Lessons from the Silicon Valley Bank Failure. The 2 Best Solar Stocks Which Countries Offer the Highest Yield for the Lowest Risk? Rebalance By the End of March Solar, EVs, Housing, HSAs -- the Highest-Yield in 2023? Are You Anxious or Depressed over Money? Why We Are Underweighting Banks and the Financial Industry. You Stream all the Channels. Should You Invest, Too? NASDAQ is Still Down -26%. Are Meta & Snap a Buy? 2023 Bond Strategy Emotions are Not Your Friend in Investing Investor IQ Test Investor IQ Test Answers Bonds Lost -26%, Silver Held Strong. 2023 Crystal Ball for Stocks, Bonds, Real Estate, Cannabis, Gold, Silver. Tilray: The Constellation Brands of Cannabis New Year, New Healthier You Tesla's $644 Billion Fall From Mars Silver's Quiet Rally. Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. Gardeners Creating Sanctuary & Solutions in Food Deserts. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed