Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

State Street Advisors sculpture of Fearless Girl in its original location. She's now in front of the NYSE. The numbers you need to know about what’s really going on. A check up on the latest indicators, and a sobering look at what is really driving the market, and emerging industries, like cryptocurrency, cannabis and the gold rally. The Federal Reserve Board is widely predicted to lower interest rates by 25 basis points today at 2:00 p.m. ET. However, it’s important to remember that even though the White House and Wall Street are pressuring the Feds to act early, that doesn’t mean they will. December 2018’s rate hike is proof of that. A slight majority of governors on the federal reserve board are keenly aware that pervasive low interest rates have created financial imbalances, overleverage and asset bubbles. Actually, all of them are aware of this. However, Randy Quarles, one of the current Administration’s recent additions to the board, believes “monetary policy should be guided primarily by the outlook for unemployment and inflation and not by the state of financial vulnerabilities.” (It’s hard to imagine a board governor actually saying this a mere 12 years after the worst bank meltdown the world has seen since the Great Depression.) Lowering interest rates at this time should keep unemployment low and inflation from sinking further. However, this is a risky move due to the level of leverage (which is eyepopping astronomical) and because the U.S. is already too close to zero to really get help from lower interest rates when the economic storms start swirling. What financial vulnerabilities? Which Feds are more hawkish? Check out my blog on these subjects by clicking on the blue highlight. See the data below for yourself. Below is what I’ll cover… Slow Growth

Astronomical Debt

Market Highs and Elevated Risk

Emerging Industries

And here’s the data on each point. Slow Growth

Everyone loves lower taxes. However, in your own home, if you reduce your income, you know you had better cut your costs. Otherwise, you might lose your home or end up in bankruptcy court. The same holds true with the Federal government. The tax cuts dramatically reduced the income of the federal government. This was not made up for in economic growth, as the American people were promised. And now, debt and deficits have soared to all-time, perilous highs.

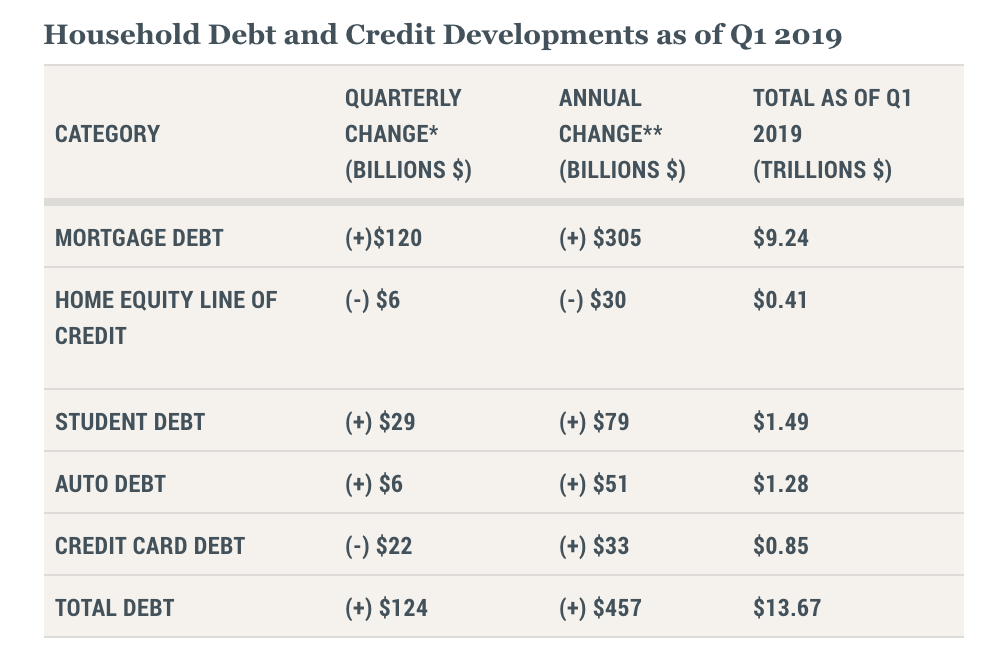

Source: Federal Reserve Bank of New York Center for Microeconomic Data. (c) 2019. Used with permission.

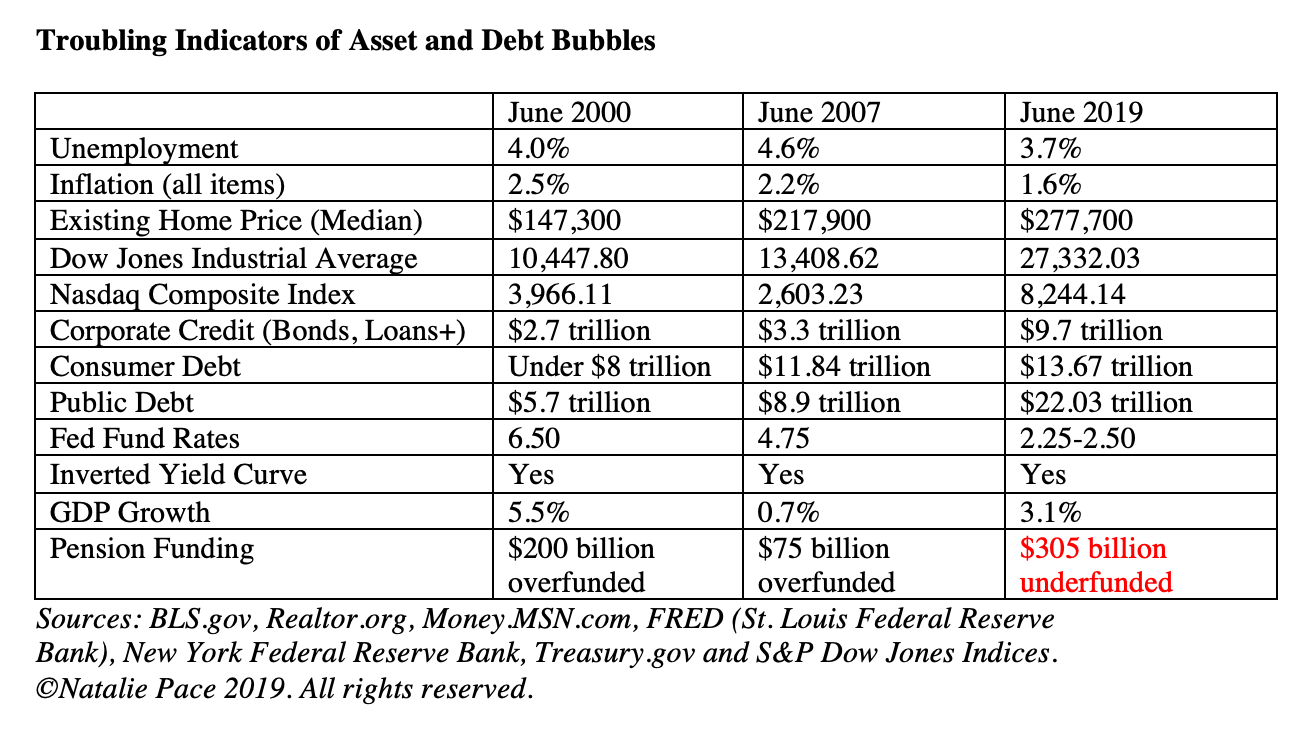

Elevated valuation pressures tend to be associated with excessive borrowing by businesses and households because both borrowers and lenders are more willing to accept higher degrees of risk and leverage when asset prices are appreciating rapidly. The associated debt and leverage, in turn, make the risk of outsized declines in asset prices more likely and more damaging. Similarly, the risk of a run on a financial institution and the consequent fire sales of assets are greatly amplified when there is significant leverage involved. In other words, the economy today looks a lot like it did in 2008, when we had to bail out the banks. Next time, however, the banks will resort to a bail-in program – on your dime. (Keep reading.)

Used with permission.

Market Highs and Asset Risks.

Emerging Industries Libra & Cryptocurrency. Facebook’s Libra cryptocurrency has a vision to create a more globally inclusive currency, based in block-chain and backed by a basket of assets (unlike most cryptocurrency that have no asset backing). The obstacles include a pervasive, inherent lack of trust that users have about Facebook. Additionally, government entities, like Congress and the Federal Reserve Board, want a thorough examination of Libra before it is allowed to infiltrate the monetary system. As for Bitcoin, Ethereum, Litecoin and others, these are mostly trading platforms. Very little actual consumption purchases are happening with the coins themselves simply because you can’t have a currency that is valued at $20,000/coin on one day and $6,000 just a few months later.

If the Feds cut interest rates, that, historically, kicks Wall Street back into gear. However, the “smart money” knows that the cut is coming due to economic weakness. Additionally, a rate cut is already built into the current record-highs. If the Feds don’t cut interest rates, something that few on Wall Street are expecting to happen, it’s because they are concerned about financial stability. The “smart money” will understand quite clearly that the Feds are deliberately taking away the punch bowl of this bull market, which has been largely built upon businesses and consumers borrowing from Peter to pay Paul. In this case, we may see another Wall Street tantrum, such as we saw in December of 2018, when the Federal Reserve Board dared to defy the White House and raised interest rates. Stocks sank 10%, for the worst performing December since the Great Depression. In either scenario, it seems very clear that we are in the latter days of this business cycle. That’s not what you’re going to hear from your broker-salesman. They will tell you how great your investments are doing (now that stocks, real estate, etc. are at an all-time high). That is why you have to be the boss of your money, and adopt a time-proven plan that doesn’t have a leaky roof that floods your financial home when economic storms hit. I’ll offer comments on the Fed decision on my Twitter feed around 2:00 p.m. ET today. You can access it on the home page at NataliePace.com. Now is the time to fix the roof while the sun is shining (while the markets are at an all-time high). If you'd like to learn time-proven strategies that earned gains in the last two recessions and have outperformed the bull markets in between, join me at my Wild West Investor Educational Retreat this Oct. 19-21, 2019. Click on the flyer link below for additional information, including the 15+ things you'll learn and VIP testimonials. Call 310-430-2397 to learn more. Register by July 31, 2019 to receive the best price. I'm also offering an unbiased 2nd opinion on your current retirement plan. Call 310.430.2397 or email [email protected] for pricing and information.

Other Blogs of Interest Red Flags in the Boeing 2Q 2019 Earnings Report The Weakening Economy. Think Capture Gains, Not Stop Losses. Buy and Hold Works. Right? Wall Street Secrets Your Broker Isn't Telling You. Unaffordability: The Unspoken Housing Crisis in America. Are You Being Pressured to Buy a Home or Stocks? What's Your Exit Strategy? Will the Feds Lower Interest Rates on June 19, 2019? Should You Buy Tesla at a 2 1/2 Year Low? It's Time To Do Your Annual Rebalancing. Cannabis Crashes. Should You Get High Again? Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth The Zoom IPO. 10 Rally Killers. Fix the Roof While the Sun is Shining. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. Tesla Delivery Data Disappoints. Stock Tanks. Why Did Wells Fargo's CEO Get the Boot? Earth Gratitude This Earth Day. Real Estate is Back to an All-Time High. Is the Spring Rally Over? The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What's Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed