Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

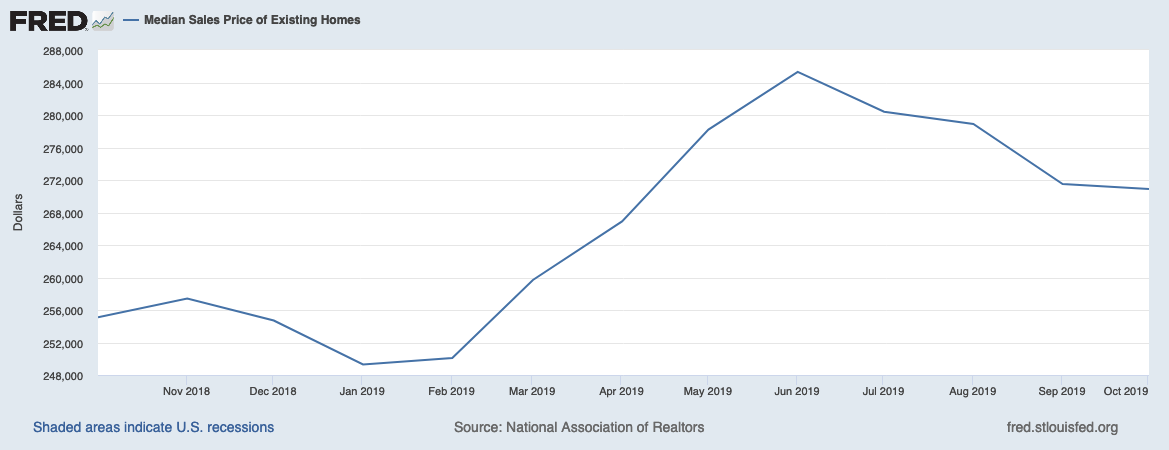

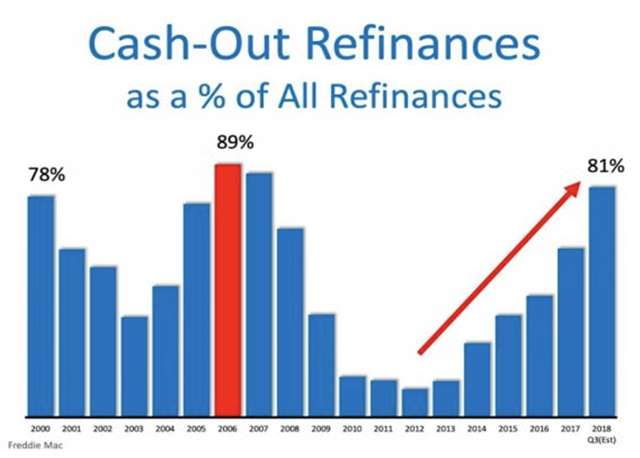

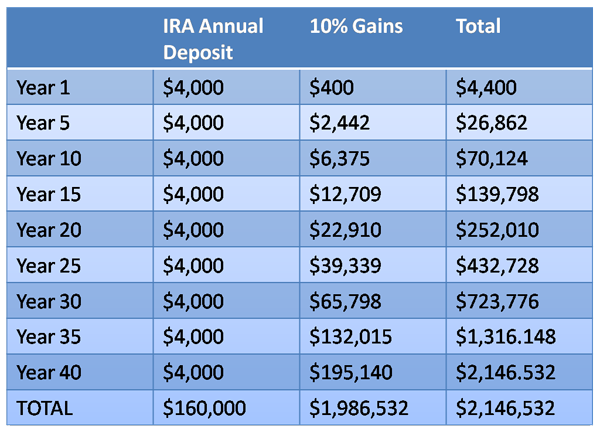

Real Estate Prices Decline. Includes Strategies for Homeowners and Renters. Home price gains over the past decade have been impressive. In June of 2019, the median sales price of existing homes nationwide hit an all-time high of $285,300. Price appreciation was led by the West (87.7%), the South (52.3%) and the Midwest (47.7%), with the North East witnessing the slowest increase, at 29.9%. However, since June, the median sales price of existing homes has been declining. The decline of the last few months marks the first time in over a decade that home prices have headed south. The average sales price slid to $270,900 between June and October 2019 (source: National Association of Realtors).  However, in the Great Recession over 10 million homes were lost. And even today, over a decade later, with real estate prices at all-time highs, 3.2 million mortgages are still 25% or more higher than the value of the home (in other words, the mortgage is underwater). This data is a reminder that buying high, or refinancing high and pulling out the cash, can be a perilous idea. Currently, 74% of U.S. median-priced housing markets are out of reach to average wage earners (source: Attom Data). When buyers become scarce, prices are under pressure. Lawrence Yun, the Chief Economist of the National Association of Realtors, and others in the industry have been calling for more home construction to bring down prices for years. There is a movement toward intergenerational housing. Micro and affordable housing are buzz words. Meanwhile, 34% of renters and 25% of homeowners spend more than 30% of their income on housing (source: Freddie Mac). That is likely the primary reason that consumer debt just hit $14 trillion – the highest it has ever been, and why cash-out refinances are back to pre-recession highs. The Home Equity ATM Machine Red Flag is Back. With Tips on How to Protect Yourself. Have you recently done a refinance on your home, where you pulled the cash out to make ends meet? You are not alone. According to Freddie Mac, the percentage of cash-out refinances as a percentage of all refinances hit an all-time high in the 4th quarter of 2018 – just as it was in 2000 (before the Dot Com Recession) and 2006-2007 (before the Great Recession). The percentage of cash-out refinances was 82% at the end of 2018, 89% in 2006 and 83% in 2000. Freddie Mac is quick to point out that the total amount cashed out this year is far less in dollar terms than 2006, and that the amount of home equity is still very strong. $14.8 billion (inflation adjusted) was cashed out in the 4th quarter of 2018, compared to $104.8 billion in the 2nd quarter of 2006. U.S. households own real estate totaling $25 trillion, with debt of $10 trillion. So, there’s still a lot of equity on the table – $15 trillion – assuming home values remain elevated. If you factor in the $14 trillion of consumer debt, the American consumer is flying a little close to the trees, particularly if home prices continue to abate.  More Spending and Debt Can Plunge Consumer Resilience Consumers have been a bright spot in GDP growth, while business and national spending have been declining. The new wealth created in households (largely concentrated in the top 1% of households) may prove to be transitory, however, just as it was in 2007. Why and how? Both real estate and stocks are back to all-time highs. Both assets dropped dramatically in the Great Recession, wiping out personal disposable income, and leaving many homeowners with a financial hangover that took a decade to recover from. When home equity is used as an ATM machine that is a warning sign that the household budget is under distress. Additionally, tariffs and a weakening worldwide economy put pressure on Wall Street. Stocks lost money in 2018, as did corporate bonds. The Number of Homes Seriously Underwater is Still an Issue It’s interesting that at a time when real estate prices are at an all-time high and home lending standards are still considered to be conservative, the number of severely underwater homes is still 3.5 million (source: Attom Data Solutions). That means that 1 in 15 mortgages are seriously underwater, worth 25% more than the value of the home. How is that happening? Here’s the math. A homeowner manages to keep his/her home through the Great Recession, but needs a loan modification in order to afford the payments. The bank has already written the nonperforming loan off. Now the mortgage can be rewritten, with new fees, at a higher principal, with all of the unpaid monthly mortgage payments, penalties and refinance fees tacked onto the total amount owed. The bank then gives a very low interest rate to the homeowner with a payment that is affordable only if you think that paying over a third of your salary to a mortgage that is at least 25% higher than the value of your home is a sound strategy. The homeowner feels strapped and out of options, and knows that this is a short-term solution that leaves them holding the short end of the stick, but signs on the dotted line anyway in order to be able to stay in their home for a little while longer. In that manner, yet another loan modification that puts the homeowner severely underwater slips quietly into the data. International Sales Lead Exodus & Unaffordability A lot of real estate executives point to international buyers whenever they encounter guff from their clients about affordability. However, in 2019, the drop in international purchases of American real estate plunged by 36% (source: The National Association of Realtors). China continued to be the top buyer of U.S. real estate for the 7th consecutive year. However, sales to Chinese home buyers dropped by 56% year over year. What’s Your Best Strategy if You are Borrowing to Make Ends Meet, or if Your Bank is Offering You an Underwater Loan Mod? If your home is underwater now at the top of the market, then the sooner that you acknowledge this, the faster you can adopt a more sustainable budget and recover. The longer you wait, the more stress you will have. You may only be prolonging the inevitable. If prices continue to fall, your situation will only become more dire. Praying and hoping that home prices will continue rising forever is not a sound assumption, especially if they are unaffordable to most of the denizens who live in your community. In short, it’s time to rethink your budget from the ground up. Cutting out café lattes is not going to fix things. Cash-out refinances and underwater loan mods are band-aids that will not stop the cash bleed in your budget. It’s the big-ticket spending that is keeping you hand-to mouth. Housing has become unaffordable, as has transportation, health insurance and many other big-ticket bills. There are solutions, however. Now is the time to address this – while the home prices and stock prices are at all-time highs. It’s a great idea to fix the roof while the sun is still shining. Once the economy weakens, your options could be more limited. The Thrive Budget If you want to fly and thrive, you’ve got to lighten your load. Below are 7 Strategies to Consider. How to Thrive, Instead of Being Buried Alive in Bills 1. Taxes Lower your tax base by contributing to your 401K (pre-tax) and by investing in your retirement funds (where you can typically avoid capital gains taxes). Start learning the difference between earned income, which is taxed at very high rates, and passive income, which is how the wealthy pay lower rates than their executive assistants. This is a way to keep more of your money and to start compounding your gains. 2. Increase Your Passive Income, While Lowering Your Taxes Long-term capital gains can be 0-20%, depending upon your tax bracket. When capital gains occur in your tax-protected retirement account, they are not taxed. When you invest in your individual retirement accounts, you are earning money while you sleep, which is a strategy of the wealthy. (Rich people don’t put their money in jars.) If you invest 10% of your income in tax protected retirement accounts, and that earns a 10% gain, then you’ll have more money in your accounts than you earn in 7 and a half years. Your money will make more than you do in about 25 years.  This Savings vs. Investing chart uses the salary of an individual earning $40,000 annually. Higher salaries will result in much higher gains! Contact Natalie Pace at 310-430-2397 for more information on sound strategies for your nest egg. 3. Cut Your Health Insurance Costs If you are healthy and spending an arm and a leg on health insurance, then consider opting for a high deductible and a Health Savings Account. The savings you achieve on your health insurance premiums can go to increase your own wealth in your HSA, instead of just making the health insurance company rich. HSAs are the best long-term health care plan. You will also receive a tax credit. Learn more at IRS.gov. 4. Rethink Housing Intergenerational housing and micro housing are the hottest new trends going. Is it best for each family member to live in an apartment and make the landlord rich, or learn to live together again and keep the money in the family? Only you can be the judge. However, the more you can combine households, the lower the costs for each adult will be. The nuclear family is rapidly becoming a page in history. Millennials who live close to parents may have the added benefit of sharing food costs and lower child care costs. While downsizing might fix your budget, making better use of the space you’re in might be an even better idea. 5. Reduce Your Commute The average person spends $7500 annually on their personal vehicle, including the car payment, insurance, maintenance and gasoline. This increases when gas prices rise, as they are predicted to do, if Saudi Arabia and Russia have their way. Can the family give up one car? Should you move closer to work? Can you take public transportation, ride a bike or purchase an e-scooter, at least for quick trips near your home? The new micro-mobility companies, like Bird, Uber, Lyft and Spin are covering the funding for better bike lanes. If your city or campus has not yet discovered this last-mile solution, it’s worth leading the charge for change. 6. Do an Air-Test on Your Home Are you heating and cooling the outside of your home? Are you a Leaks-R-Us dwelling? Do you still use incandescent bulbs thinking they are cheaper? Are you aware of the savings of a simple counter-top toaster oven for small baking needs? Getting megawatt smart could cut your electric bill in half or more. For most Americans the savings will be in the thousands of dollars. 7. Take Advantage of the 30% Tax Credit for Solar and Energy Efficiency Upgrades If you live in a sunny state, the math for rooftop solar has never been more compelling. There is a 30% tax credit in play through the end of 2019, which drops to 26% in 2020 and 22% in 2021. (So, consider this now.) Click for additional information on the EnergyStar.gov website. Solar panels have never been more affordable. Many homeowners take a $300/month bill down to $30/month. You may be able to borrow from your 401K or Individual Retirement Account (IRA) to cover the purchase costs of purchasing and installing rooftop solar panels and a solar water heater. Be sure to get your megawatt usage down as low as possible before you get your quote. The number of panels that you need is determined by how much electricity you use. Stop Making Everyone Else Rich The goal is to stop making the tax man, banker, landlord, utility company, gasoline station, insurance salesman and more rich at your own expense. Wisdom and innovative thinking, accompanied by bold changes, are the cure when your household budget has you buried alive in bills and struggling to survive.  Call 310-430-2397 or email info @ NataliePace.com to learn more. Other Blogs of Interest Hong Kong Slides into a Recession. China Slows. They Trusted Him. Now He Doesn't Return Phone Calls. Beyond Meat's Shares Dive 67% in 2 Months. Price Matters. Will There be a Santa Rally? It's Up to Apple. Will JP Morgan Implode on Fairy Tales and Unicorns. Harness Your Emotions for Successful Investing. What the Ford Downgrade Means for Main Street. The Dow Dropped Over 1000 Points Tesla's 3Q 2019 Deliveries Could Hit 100,000. Do We Talk Ourselves into Recessions? Interview with Nobel Prize Winning Economist Robert J. Shiller. The Winners and Loser of a Clean Energy Policy. Make the Climate Strike Personal. Ford is Downgraded to Junk. From Buried Alive in Bill to Buying Your Own Island. The Manufacturing Recession. An Interview with Liz Ann Sonders. Gold Mining ETFs Have Doubled. The Gold Bull Market Has Begun. The We Work IPO. The Highs and Hangovers of Investing in Cannabis. Recession Proof Your Life. China Takes a Bite Out of Apple Sales. Will the Dow Hit 30,000? A Check Up on the Economy Red Flags in the Boeing 2Q 2019 Earnings Report The Weakening Economy. Think Capture Gains, Not Stop Losses. Buy and Hold Works. Right? Wall Street Secrets Your Broker Isn't Telling You. Unaffordability: The Unspoken Housing Crisis in America. Are You Being Pressured to Buy a Home or Stocks? What's Your Exit Strategy? Will the Feds Lower Interest Rates on June 19, 2019? Should You Buy Tesla at a 2 1/2 Year Low? It's Time To Do Your Annual Rebalancing. Cannabis Crashes. Should You Get High Again? Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth The Zoom IPO. 10 Rally Killers. Fix the Roof While the Sun is Shining. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. Tesla Delivery Data Disappoints. Stock Tanks. Why Did Wells Fargo's CEO Get the Boot? Earth Gratitude This Earth Day. Real Estate is Back to an All-Time High. Is the Spring Rally Over? The Lyft IPO Hits Wall Street. Should you take a ride? Cannabis Doubles. Did you miss the party? 12 Investing Mistakes Drowning in Debt? Get Solutions. What's Hot in 2019? The Debt Ceiling Was Hit (Again) on March 1, 2019. How Bad Will the GDP Report Be? 2019 Investor IQ Test The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. 14/8/2020 12:38:47 am

I will need a real estate agent to help me with buying a new home. I will make sure to build up my credit before starting the buying process. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed