Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

Answers to the 2024 Investor IQ Test. by Natalie Pace. If you score 21 correct answers or higher, then you’re in great shape! If you score 18, then you are C-level. Join us now at our next Financial Freedom Retreat to learn the life math that will save you thousands annually, earn money while you sleep, activate a much richer life, and lead to generational wealth. Below 18 correct indicates that you are in real need of a basic course in life math. (Even Ph.D.s and math geniuses might not know the basics of Wall Street… We have a lot of well-educated and financial professionals who attend our retreats!) So, consider joining us at our next Investor Educational Retreat. Our time-proven 21st Century strategies are enthusiastically recommended by Nobel Prize-winning economist Gary Becker, former TD AMERITRADE chairman and CEO Joe Moglia, McArthur Genius Award winning economist Kevin Murphy and thousands of Main Street investors. So, consider joining us at our next Investor Educational Retreat. 1. What is the most important question you should ask your Certified Financial Advisor before hiring him/her? "How much of my portfolio should I keep safe?" This question will help you to determine whether you are dealing with a trusted professional who is looking after your best interest, or a salesman who is looking to make a quick buck. The answer to this question is, "A percentage equal to your age.” As stocks are trading at elevated prices, bonds are carrying duration and credit risk, which can make them illiquid and negative-yielding, it would be even better if s/he adds, “But given the valuation and leverage concerns, we might consider overweighting into safety." If they just sidestep this question and redirect you to a risk tolerance questionnaire, that is a red flag. If they tell you not to worry because things always work out in the end, that it a sure sign that you are adopting the Buy & Hope plan, which wipes investors out in recessions – something that is never ideal, but can be devastating as we get closer to retirement. One more important thing. Since many long-term bonds are highly leveraged, subject to credit risk, vulnerable to capital loss and can be illiquid to boot, we need to know what’s safe in a Debt World, rather than just rely upon bonds, annuities or money market funds. Now is the time to clearly know exactly what we own and why. Consider getting an unbiased 2nd opinion. Call 310-430-2397 or email [email protected] for pricing and details. 2. What are 3 red flags that your financial plan is on a Wall Street rollercoaster and at risk of losing half or more of its value?

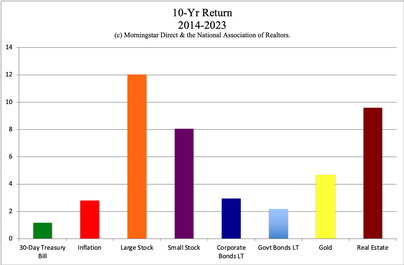

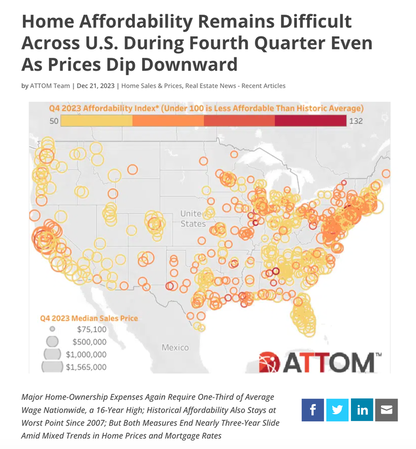

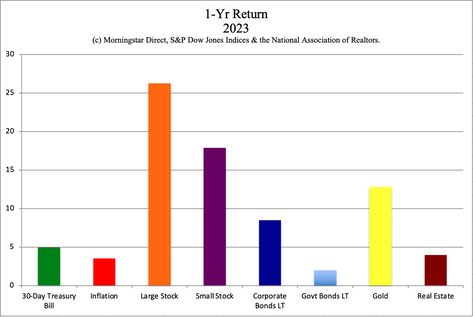

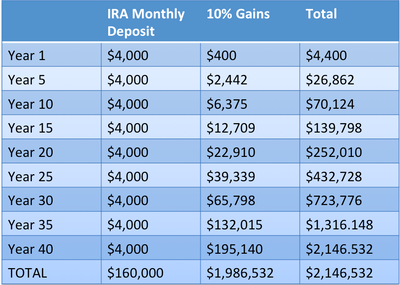

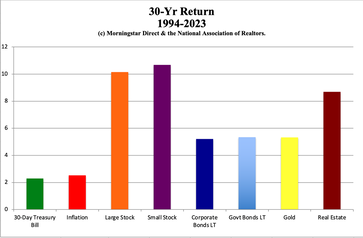

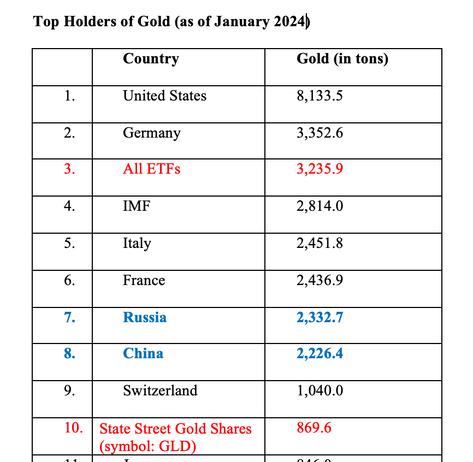

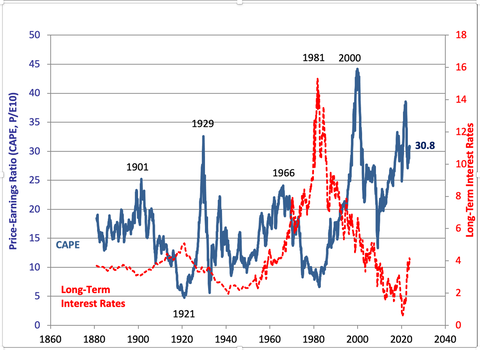

3. How much of your nest egg should you keep safe? A percentage equal to your age. Consider overweighting more into safety when assets are overpriced, the economy is weak, or you are nervous. Again, in today’s Debt World, it is important to know what’s safe. Long-term bonds are losing value and are illiquid, which makes them substantially riskier than most investors realize. (Our safe side isn’t supposed to lose money!) Money market funds can have liquidity fees, are vulnerable to capital loss and are not FDIC-insured. Annuities are more vulnerable than most investors know because insurance companies are carrying a great deal of risk and leverage, can have hidden fees and terms that mute performance, and annuities are not federally insured. 4. What's safe? You might consider short-term, creditworthy FDIC-insured CDs, Treasury Bills or bonds. Rolling, short-term maturity dates ensure that we have access and liquidity in case another investment opportunity arises, and protects us from duration risk. Read the fine print. Be cautious about extending duration beyond a few years. Factor in the credit risk. Hard assets will hold their value better than paper assets in a Debt World. So, the mantra “safe, income-producing hard assets that you purchase for a good price” is another good option. Real estate is at an all-time high in the U.S., so it will be difficult to purchase for a good price in 2024. There are some hard assets that offer the best ROI by reducing our monthly expenses (for life), which we cover at the Financial Freedom Retreat, and in our blogs and videoconferences. You don’t want to be all in on hard assets because you also need liquidity and cash flow. We spend one full day on What’s Safe at the Investor Educational Retreats. Educate yourself now on the best income-producing hard assets that are right for you, so that when prices are more attractive, you know what you want and have the means to take action and close the deal. Call 310-430-2397 to learn more. Everyone is hoping that interest rates will start getting cut in the 2nd half of 2024. However, the expectation is for the Fed Fund rate to remain in the range of 4.6%. So, hoping for relief soon in interest rates might be a pipedream. There may be work-arounds, however. 5. What is the average return of stocks over the last 10 and 30 years? Large cap stocks earned 12.03% annualized over the last decade and 10.15% over the 30-year period (source: Morningstar). Small cap stocks performed at 8.06% and 10.68%, respectively. (Asset performance graphs, and more data and resources, are distributed to Retreat Attendees.) 6. What is the average return of gold over the last 10 and 30 years? Gold returned 4.70% annualized over the 10-year period and 5.33% over the last 30 years. Gold mining stocks doubled in 2016, were flat in 2017, and doubled (again) off their 2018 lows by August 2020. Regular rebalancing (1-3 times a year) prompts us to trim high and add low. The all-time high for gold of $2,146.79 was hit on Dec. 3, 2023. The previous high of $1,895/ounce in gold in September of 2011, occurred the month after S&P Global Ratings stripped the U.S. of its AAA credit score. That was in the wake of a Congress/White House showdown over the Debt Ceiling. No one panicked when Fitch Ratings downgraded the U.S. on Aug. 2, 2023. However, that could change. 7. What is the average return of real estate over the last 10 and 30 years? Over the last decade, real estate has performed at an impressive 8.6% annualized. However, there were devastating losses during the Great Recession, when over 20 million homes were foreclosed on. The losses are not reflected in the 10-year statistic. Over a 30-year period, real estate increased 8.3% annualized.  Real estate prices are at an all-time high. Housing is largely unaffordable. According to AttomData, average income-earners would have to spend a third or more to buy a home. Rising interest rates have made this problem a crisis. 2.5% of U.S. homes are still seriously underwater on their mortgage – even with prices higher than ever. (This is largely due to loan mods.)  Homeowners are significantly wealthier than renters. So, this is definitely something to aspire to. However, there is nothing worse than buying high in real estate, and watching the value of your home sink below the amount that you owe on it! It can ruin your life and FICO score for years, if not decades. Be sure to read the Real Estate section of the 5th edition of The ABCs of Money. There are at least seven real-world case studies to inform your real estate decisions. We offer time-proven, out-of-the-box, real estate solutions in our master classes and private coaching. Email [email protected] for additional information. There is always a way to move toward our goals in a prudent manner. 8. What was the top performing investment in 2023? Bitcoin started the year in the $16,000/coin range and then rocketed up to $42,231 by Dec. 31, 2023 for gains of 171%. The high for Bitcoin is $69,000/coin. The volatility is crypto is problematic for HODL. Our pie chart system with regular rebalancing puts us on the right side of the trade. (This strategy is featured on at our Financial Freedom Retreats.)  Bitcoin hit an all-time high of $69,000 on Nov. 9, 2021. Large stocks performed quite well, with gains of 26% (source: Morningstar Direct). However, most of those gains were concentrated in the Magnificent 7, with the Dow Jones Industrial Average performing at half that speed, with gains of just 13.7%. Oil was one of the few assets that lost money in 2023, something that helped consumers keep spending. Even with high interest rates, real estate housing prices gained 4%.  9. How long will it take for you to have a nest egg as big as your annual salary if you put 10% of your income into a tax-protected (and financial predator proof) individual retirement plan and invest in stocks and bonds*? 7 ½ years. This is based upon 10% average annualized returns of stocks and bonds over a 30-year period, which is what happens in a normal economy.   10. How long will it take for your nest egg to earn more than you earn, if you put 10% of your income into a tax-protected (and financial predator proof) individual retirement plan and invest in stocks and bonds*? 25 years. This is based upon 10% average annualized returns of stocks and bonds over a 30-year period, which is what happens in a normal economy. 11. What’s the safest investment in a slow-growth, high-debt world? Bonds are starting to reward investors. However, avoiding the losses and illiquidity is tricky, unless you are quite well-informed (not just having blind faith that someone else is protecting you). FDIC-insured CDs are paying in the 5% range. However, you have to know the loopholes and read the fine print. Due to the poor credit quality of many banks, I’d still adhere to a short-term, creditworthy policy.  Hard assets hold their value better than paper assets when there is too much paper floating around (debt, like there is today). So, if you have a home or income-producing assets with equity, think twice (and consider private coaching) before turning your hard asset into paper money. At the same time, being real estate rich and cash poor can make us vulnerable, as we still need liquidity. The safe side has opportunity and money pits, which is why we spend one full day on this topic at our Investor Educational Retreats. I hosted a Bond Master Class in October of 2023. Email [email protected] if you’re interested in receiving access to the recording of the class. There are some excellent safe, income-producing, value-priced hard assets that are worth considering now, which most people are not aware of. Many hard assets are overpriced right now. If you are equity-rich, you still want to do the analysis to make sure that will remain the case if real estate asset prices decline significantly in value, as they did in the Great Recession. Be sure to read the Real Estate section of the 5th edition of The ABCs of Money. In addition to looking for some return on the safe side, think capital preservation. Liquidity will allow us to buy low when things are on sale. 2024 will allow us to do both, if we’re strategic about keeping the terms short and the creditworthiness high. 12. Which countries hold the most gold? The United States is the top holder of gold worldwide, by far, with 8,133.5 tons, followed by Germany, all ETFs, the International Monetary Fund, Italy, France, Russia and China. China and Russia have been on a gold buying spree since 2008. Both countries increased their holdings in 2023. Reports are that they are trading oil and other commodities using their own currency backed by gold, in an effort to break free from the dollar hegemony. BRICS (Brazil, Russia, India, China and South Africa) have launched their own currency. India also increased their gold holdings.  © The World Gold Council at Gold.org. Used with permission. 13. Are annuities safe? Insurance products, including life insurance and annuities, aren't insured by the FDIC. If we had not bailed out AIG in 2007, more than 50 million annuity holders would have been in real trouble. Your annuity product is only as safe as the insurance company that is selling it to you. Insurance companies don’t fare well in recessions, historically. Insurance products are like being a renter. If you can’t pay, you get tossed out. Many people pay for life insurance their entire working life, and then can’t pay when they retire – when they are really most in need. If you put that money into your own tax protected account, you could save on taxes, compound your gains, and it would be there for you when you retire, even offering some income, in addition to the capital. (Billionaire Peter Thiel reportedly has over $4 billion in his Roth IRA. Regular contributions, investing and compounding gains are that powerful.) When you can no longer contribute to your own retirement plan and Health Savings Account, they support you. We can be the boss of our wealth, once we learn The ABCs of Money that we all should have received in high school and college. Once we know what we own and invest in, and why, we can stop making everyone else rich and start living a richer life. 14. What were the top performing and the worst months for stocks over the past five years? November, July, April and October performed the best over the 5-year period (in that order), on average. September, February, March and May were all negative months. Retreat Attendees receive charts of the top-performing months and election year trends. If you’re interested in learning more about our 3-day, life transformational investor educational retreats, call 310-430-2397 or email [email protected]. 15. What was the top performing quarter for stocks over the past twenty years? October through December – the Santa Rally – performed the best over the 20-year period, but saw greater volatility than normal, particularly in December. December 2018 was the worst performing December in history, with losses of -9.2%. Understanding seasonal trends can help us with our annual rebalancing in our nest egg, and with our selling strategy for trading. We’ll be hosting a Rebalancing Master Class on Jan. 20, 2024. Regular rebalancing is a very important part of our nest egg strategy. We spend one full day on what’s hot, teaching how to identify the best investments of the year, in our Investor Educational Retreats. (The retreat is a prerequisite for the Rebalancing Master Class.) 16. What was the worst investment in 2023, NASDAQ, gold, the Dow Jones Industrial Average, bonds, cannabis, oil or real estate? Cannabis and plant-based protein continued to scrape the bottom of Wall Street. Oil prices dropped -37.93%. Bonds were pretty poor performers, and haven’t recovered the devastating drop of 2022. Stay tuned into my blogs, Instagram broadcast channel, podcasts and videoconferences for ongoing news, analysis and vital investor information. Email [email protected] with VIDEOCON in the subject line to receive the logon information for the next monthly videoconference. 17. Which year is expected to perform better, 2024 or 2025, based upon historical returns of election years? 2024 is an election year. Election years can be good, with an average 12.9% gain over the 10-year period. However, we’ve seen some disasters, such as 2008 (Great Recession) and 2000 (beginning of the Dot Com Recession). Over the last 10-20 years, election and mid-term years have been the worst performers in the election-year cycle. U.S. stocks are still quite pricey, which could mute gain possibilities this year, as could slow GDP growth. A mild recession is forecasted for 2024, possibly in the first half of the year. (We’ll know more on April 25, 2024, when the advance GDP for the 1st quarter of 2024 is published by the Bureau of Economic Analysis.) As you can see in the CAPE ratio below (Nobel Prize winning economist Robert Shiller’s stock valuation tool), the only two times that stocks were more expensive than they are now were during the Dot Com Recession and the Great Depression.  Professor Robert Shiller's CAPE ratio. Yale.edu. Having expensive stocks, unaffordable real estate, and higher interest rates than we’ve had in 15 years, as government support is easing back and credit is still tight, has increased the potential for volatility on Wall Street. There have been wild rides over the past five years. This is likely to continue as the hot and fast Wall Street whales seek to gobble up incremental gains. 18. How many companies are in the Dow Jones Industrial Average? 30 companies. Many are household brands. Most have been around for over half a century, and many are carrying far more debt than the value of the company. As I mentioned previously, the DJIA is underperforming the S&P500 by almost half. Leverage has begun to concern economists. Over 50% of the S&P500 corporate bonds are at the lowest rung of investment grade, or at junk bond status. This includes a lot of banks, brokerages, financial services and insurance companies. If you don’t understand how much debt corporations are holding, you can learn how to use this valuable tool to increase the performance of your nest egg on the 2nd day of the Investor Educational Retreat. Click to access the names of the 30 companies. The Dow Jones Industrial Average was launched in 1896. 19. How many Dow Jones Industrial Average companies were bailed out or went bankrupt in the Great Recession? Most people don't realize that 20% of the companies of the DJIA (6 companies: AIG, American Express, Bank of America, Citi, JP Morgan and General Motors) were bailed out or went bankrupt in the Great Recession. Others, like General Electric and Ford, received support. The DJIA was the leading bailout index in the Great Recession. Learn more about how to add in performance and avoid the bailouts in your funds and retirement account at the Investor Educational Retreat and in The ABCs of Money. Due to debt and leverage, it is important to remember that the higher the dividend is, the higher the risk likely is (read the chapter of the same name in The ABCs of Money for additional information). GE investors learned this the hard way in 2017. Many REIT investors are learning it now, particularly those invested in commercial real estate. 20. Which index has performed better over the last 5 years, the Dow Jones Industrial Average or the NASDAQ Composite Index? As you can see in the chart below, the NASDAQ has outperformed the DJIA. At the same time, the DJIA tends to be less volatile.  5-year performance of the NASDAQ Composite Index vs. the Dow Jones Industrial Average. Source: MSN.com. (c) Microsoft 2024. Used with permission. This is why our pie chart system includes both value (substitutions*, rather than the DJIA) and growth (NASDAQ), as well as regular rebalancing. Using this system, investors can capture gains in technology and biotechnology at the high, and buy low when recessions and other economic shocks create opportunities. Learn more at the Investor Educational Retreat and in The ABCs of Money. *We are leaning into country diversification in our value funds, due to the leverage and slow growth in the DJIA. 21. How much did investors lose between February 19, 2020 and March 23, 2020? Both the Dow Jones Industrial Average and the NASDAQ Composite Index dropped 35%. Some of the hottest stocks, including Nvidia (-38%), lost even more. However, technology stocks surged, once everyone started working and doing everything from home. 2020 gained 16.26%, with 2021 scoring 26.89% gains in the S&P500. 22. How much did investors lose during the Great Recession and the Dot Com Recession? As I mentioned above, the Dow Jones Industrial Average lost 55% in the Great Recession.  Returns of the Dow Jones Industrial Average. Source: Morningstar.com. © 2020. Used with permission. The Dot Com Recession saw a drop in the NASDAQ Composite Index of up to 78%. It took the NASDAQ 15 years to crawl back to even. As you can see in both charts, if you wait for the recession announcement, you've already lost almost half (or more) of your wealth.  Returns of the Nasdaq Composite Index March 2000 – Oct. 2002. Source: Morningstar.com. © 2020. Used with permission. We can’t afford to lose more than half and then take 7-15 years to crawl back to even – particularly if you are over the age of 50. It’s time to step off of the Wall Street Rollercoaster and into time-proven, easy systems that protect our wealth, while outperforming the major indices. These strategies cost less time and money, and allow us to sleep better at night, knowing that our wealth is protected. 23. Does Buy & Hope work? If not, what does? Buy & Hope lost more than half in 2000 and 2008 and 35% (or more) between February and March of 2020. Due to the amount of debt and leverage, and the slow rate of growth, Buy and Hold will not work going forward (until those problems are dealt with and cycled through). Our easy-as-a-pie-chart nest egg strategies with regular rebalancing earned gains in the Dot Com and Great Recessions and have outperformed the bull markets in between. Working off of the pie charts, instead of the brokerage statement, allows us to take the emotions out of the plan, and rely, instead, upon a time-proven system. This pie chart system, with annual rebalancing, is a buy low, sell high plan on auto-pilot – prompting us to do what we should be doing at each rebalancing session. Email [email protected] or call 310-430-2397, if you’d like to customize your own sample pie chart (free) or receive an unbiased 2nd opinion through our private coaching program. (We teach you how to do this yourself at the Investor Educational Retreat and at the Rebalancing Master Class.) One more thing: low interest rates create asset bubbles. (We’ve only had 5% interest rates for less than a year.) That is one of the reasons why assets drop so severely and swiftly in 21st Century recessions. Having the right amount safe and knowing what is safe in a Debt World is our best protection. 24. Why is it that so many investors are unable to Buy Low and Sell High? Buy low, sell high is a mantra that everyone knows. So, why do so few investors do it? There are a few reasons…

25. What is the 3-Ingredient Recipe for Cooking up Profits? 1. Start with what you know and love 2. Pick the Leader 3. Buy low; sell high (easy to say; hard to do) This recipe, along with my Stock Report Card, Four Questions, market strategies and data drilling, is how I earned the ranking of number one stock picker. The recipe is easy. Learning how to use these tools requires practice. You must begin by locating and analyzing data, which is actually less time and far more informative than reading blogs, which have a fraction of the information and might be written by a novice. Come to our next Investor Educational Retreat to learn firsthand how easy and effective this strategy is, and why it has worked through bull and bear markets for more than two decades now. Call 310-430-2397 or email [email protected] to learn more. If you don’t like stock picking, no problem. Our easy-as-a-pie-chart nest egg strategy is designed for money while you sleep. Once you set up your financial house properly, you’ll just need to Spring Clean it once or twice a year. 26. What are the Four Questions for Picking Winning Stocks? The Four Questions for Picking Winning Stocks. 1. What’s the product? 2. Who’s the customer? 3. Can the company continue to make a superior product going forward and get it to their customer at the best price before the competition? 4. Who’s the CEO and can s/he motivate the employees to make the best product faster, better and cheaper than the competition? As you can see, three out of four questions can be answered by being a good customer of the company. The 3rd question will benefit from you completing a Stock Report Card, and understanding how to use the data (something we teach on Day 2 of our Financial Freedom Retreat). So, the more you know about a company (ingredient #1 of the recipe for Cooking Up Profits), the easier it is to pick the leader. In Put Your Money Where Your Heart Is, I used these questions and tools to compare two companies. Google scored an A (in 2006, when it had only been publicly traded for 2 years). The Dow Component that I gave a D- to went on to declare bankruptcy a few years after this prediction was made (General Motors). Using the Stock Report Card and 4 Questions, I identified both of these trends years before these major events occurred. The book was written in 2006, three years before GM went bankrupt. In fact, I applauded Google on national television before its IPO, when most pundits pooh-poohed it. This is the power of asking the right questions and relying upon the data, rather than just listening to the mainstream media. (We also warned about General Electric years before it was booted from the DJIA. This was also evident in the data, but not in the headlines) So, are you an Einstein in investing? A complete novice? If you scored 21 correct answers or higher, then you’re in great shape! If you scored 18 right, then you are C-level. (Come to our next retreat to proceed up the path to financial wisdom!) Below 18 correct indicates that you are in desperate need of a basic course in life math, which will transform your life and relationship with money. (Email [email protected] to start with one of our free videocoaching courses in Prosperity/Abundance, Debt Reduction, Sustainability or the Thrive Budget.) Call 310-430-2397 or email [email protected] to learn more. The High Cost of Free Advice A few years ago, our team was told yet another story about someone who lost a substantial amount of money by trusting the "free" advice of a financial advisor. Learn the truth about commissions & conflicts of interest & how to get a 2nd opinion now in the guest blog “They Trusted Him. Now He Doesn’t Return Phone Calls.” Know what you own. Protect your future now! Data Sources: (c) 2024 Morningstar Direct, S&P Dow Jones Indices, the World Gold Council and The National Association of Realtors. All rights reserved. Used with permission. The information contained herein: (1) is proprietary; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar, the National Association of Realtors, the World Gold Council, Natalie Pace, nor any content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Join us at our Jan. 13-15, 2024 New Year, New You Financial Freedom Retreat. Get valuable data and tools on how to best invest and monetize in real estate. Learn nest egg strategies, how to get hot and diversified (including in EVs, crypto and AI), and what's safe in a Debt World. You'll even discover how to save thousands annually with smarter big-ticket choices. Yes, it's a complete money makeover, which is a great way to start 2024! Email [email protected] to register. Learn the 15+ things you'll master and read testimonials in the flyer (link below) and on the home page at NataliePace.com. Register with friends and family to receive the best price. "Ten minutes into the first day I was already much smarter about investing than I ever thought I would be in my life and I knew I was in exactly the right place at this retreat. I am amazed at how EASY and FUN it is to make my money work for me and those I love. I think this kind of information should be compulsory in schools. I wish I'd learned this sooner." CM  Join us for our Online New Year, New You Financial Freedom Retreat. Jan. 13-15, 2024. Email [email protected] or call 310-430-2397 to learn more. Register with friends and family to receive the best price. Click for testimonials, pricing, hours & details.  Join us for our Restormel Royal Immersive Adventure Retreat. March 8-15, 2024. Email [email protected] to learn more. Register with friends and family to receive the best price. Click for testimonials, pricing, hours & details. There is very limited availability, and you must register early to ensure that you get the exact room you want. This retreat includes an all-access pass to all of our online training for a full year for two!  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money and the 2nd edition of Put Your Money Where Your Heart Is were released in 2021. Follow her on Instagram. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Substack on Apple and Spotify. Watch videoconferences and webinars on Youtube. Other Blogs of Interest Apple's Woes Drag Down the Dow. The Winners & Losers of 2023. Ozempic, Magnificent 7 & Beyond. 2024 Crystal Ball. The Underperforming DJIA, Full of Fossil Fuels and Forever Chemicals. A Spectacular Year for 3 of the Magnificent 7. The Best ROI* (Almost 40%!) & 7 Life Hacks That Save Thousands. Portugal Eliminates Tax Advantages for Ex-Pats. Holiday Gift Giving on any Budget. Including No Budget. Once in a Century Events are Happening Every Day. The Crypto Winter Enters Its 3rd Year. Earn $50,000 or More in Interest. Safely. Finally. Freebies and Deals for Black Friday and Cyber Monday. Auto Strikes End. EV Price Wars Continue. WeWork's Bankruptcy. Half-Empty Office Buildings. Problems in our Personal Wealth Plan. Solutions for Unaffordable Housing. The Magnificent 7 Drag NASDAQ into Another Correction Cruise Ships Give Freebies to Investors. Should You Take the Bait? Should You Take a Cruise? Bonds. Banks. The Treacherous Landscape of Keeping Our Money Safe. 7 Rules of Investing Air B N Bust? Santa Rally 2023 or Time to Get Defensive? Barbie. Oppenheimer. Strikes. Streaming Wars. Netflix. Monero: A Token of Trust? 13 Lifestyle Choices to Reduce Waste, Pollution & CO2 & Save a Boatload of Dough. China Bans Apple 11-Point Green Checklist for Schools. Artificial Intelligence and Nvidia's Blockbuster Earnings Report Biotech in a Post-Pandemic World 10 Wealth Secrets of Billionaires and Royals. What Happened to Cannabis? Bank of America has $100 Billion in Bond Losses (on Paper) The USA AAA Credit Rating is on a Negative Watch. Lithium. Essential to EV Life. I'm Just Not Good at Investing. Investors Ask Natalie. Should I Buy an S&P500 Index Fund? Investors Ask Natalie. Bonds Lost More than Stocks in 2022. 2023 Company of the Year Do Cybersecurity Risks Create Investor Opportunities? Writers Strike, While Streaming CEOs Rake In Hundreds of Millions Annually. I Lost $100,000. Investors Ask Natalie. Artificial Intelligence Report. Micron Banned in China. Intel Slashes Dividend. Buffett Loses $23 Billion. Branson's Virgin Orbit Declares Bankruptcy. Insurance Company Risks. Schwab Loses $41 Billion in Cash Deposits. Fiat. Crypto. Gold. BRICS. Real Estate. Alternative Investments. BRICS Currency. Will the Dollar Become Extinct? The Online Global Earth Gratitude Celebration 7 Green Life Hacks Fossil Fuels Touch Every Part of Our Lives Are There Any Safe, Green Banks? 7 Ways to Stash Your Cash Now. Lessons from the Silicon Valley Bank Failure. Which Countries Offer the Highest Yield for the Lowest Risk? Solar, EVs, Housing, HSAs -- the Highest-Yield in 2023? Why We Are Underweighting Banks and the Financial Industry. 2023 Bond Strategy Emotions are Not Your Friend in Investing Bonds Lost -26%, Silver Held Strong. Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed