Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

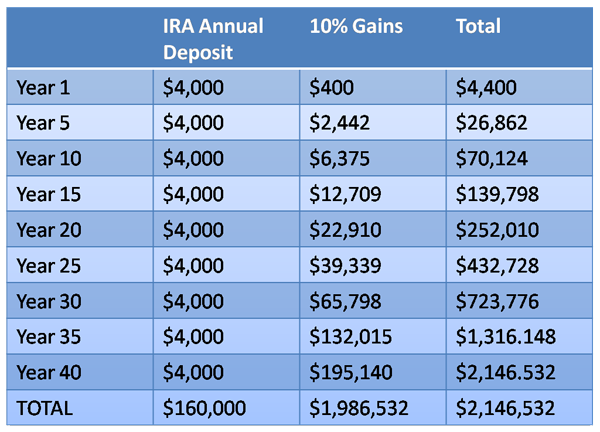

Salar de Uyuni. Bolivia. January 2007. Picture by Ezequiel Cabrera. Wiki Commons Licensing. Used with permission. Answers to the 2019 Investor IQ Test. by Natalie Pace. Feb. 12, 2019 1. What is the most important question you should ask your Certified Financial Advisor before hiring him/her? "How much of my portfolio should I keep safe?" This question will help you to determine whether you are dealing with a trusted professional who is looking after your best interest, or a salesman who is looking to make a quick buck. The answer to this question as we enter the 11th year of a bull market is, "A percentage equal to your age for sure. But this late in the business cycle, we might consider overweighting even more safe." One more important thing. Bonds are highly leveraged, subject to credit risk and vulnerable to capital loss. So, you need to understand what’s safe, rather than just relying upon bonds to keep you safe. Get 12 questions and answers to help you interview your Certified Financial Planner candidates in Put Your Money Where Your Heart Is (aka You Vs. Wall Street in paperback), in the chapter "Brokers are Salesmen, Not Surgeons." 2. What are 3 red flags that your financial plan is in peril? *If you lost 30% or more in the Great Recession and you haven’t made any changes, you’re more vulnerable today than you were then. Don’t confuse a bull market with wisdom. Everyone has made money since 2009, except 2018, when everyone lost money – even on their “safe” side, in bonds. *If you have more than just a few pages of holdings in your financial plan, your gains could be destroyed in fees and commission. You are not as diversified as you believe, as pages and pages of holdings can still just be the same type of holdings over and over again. You’re more at risk than you know. *The NASDAQ is up five times the low of March 9, 2009. The Dow Jones Industrial Average is up about 3.25 times. If your returns over the last decade is lower than this, your plan needs reviewing. Now is the time to do this assessment because Alan Greenspan, Warren Buffet and Robert Shiller have all been saying that stocks and bonds are in a bubble for over a year. During the last two corrections (2000 and 2008), most people lost more than half of their retirement. 15+ million homes were auctioned or repossessed by banks when the real estate bubble burst before the Great Recession. Wisdom and time-proven systems are the cure. The NASDAQ Composite Index Compared to the Dow Jones Industrial Average 1984-2019  Source: Google Finance. © Alphabet Inc. Used with permission. If you’d like a second opinion on your current plan from an unbiased analyst with a time-proven track record of saving homes and nest eggs since 1999, while earning the ranking of No. 1 stock picker, call 310-430-2397. 3. How much of your nest egg should you keep safe? A percentage equal to your age. Consider overweighting more safe when the economy is stumbling or a bull market is going into its 11th year (as is the case in 2019). This simple strategy helped followers of Natalie Pace earn gains in the last two recessions, and then build upon that solid foundation in the bull markets in between. In today’s world, it is important to know what’s safe. Bonds lost money in 2018, and are riskier than most investors realize. Money market funds have redemption gates and liquidity fees. 4. What's safe? Hard assets will outperform paper assets in a world where there is too much monopoly money and broken pension promises floating around. So, the mantra is “safe, income-producing hard assets that you purchase for a good price.” It’s hard to buy real estate at a good price in 2019. You don’t want to be all in on hard assets because you also need liquidity and cash flow. That is why some of the best hard asset investments are those that reduce your monthly expenses (for life). That is why I spend one full day on What’s Safe at the Investor Educational Retreats. Shop for this year’s low-hanging fruit. Educate yourself on the best income-producing hard assets that are right for you now, so that when prices are more attractive, you know what you want and have the means to move on it. Call 310-430-2397 to learn more. 5. What is the average return of stocks over the last 10 and 30 years? Large cap stocks earned 13.12% annualized over the last decade and 9.97% over the 30-year period. Small cap stocks performed at 13.08% and 10.87%, respectively. (Asset performance graphs, and more, are available to 2019 Retreat Attendees.) 6. What is the average return of gold over the last 10 and 30 years? Gold returned 3.10% annualized over the 10-year period and 3.79% over the last 30 years. While gold doesn’t look like much on paper, gold mining stocks doubled in 2016, and are currently on sale for 75% off. The all-time high of $1,895/ounce in gold occurred in September of 2011, the month after Standard and Poor’s downgraded the U.S. credit. 7. What is the average return of real estate over the last 10 and 30 years? Real estate prices are higher today than they were before the Great Recession – meaning real estate is largely unaffordable in many areas, particularly for Millennials and the middle class. How does that play out in returns for homeowners? If you started owning your home 30 years ago, you’ve made 5.8% annualized – that is if you avoided using your home equity as an ATM machine pre-2006! If you purchased a decade ago, you might have been a victim of the more than 17 million auctions and bank REOs (repossessions). Over the last decade, real estate has performed at 4.90% annualized. (It took over a decade for real estate to recover from the Great Recession.) 8. What was the top performing investment in 2017? Publicly traded cannabis stocks Cronos and Canopy Growth saw explosive gains in their share price. Cronos is up almost five times from its low over the past 52-weeks, while Canopy Growth has doubled. Aphria and Aurora Cannabis have not enjoyed the same kind of success, however. Both stocks are slightly lower where they were a year ago. And there are also some fakers, particularly in the high risk penny pot stocks. So, cannabis is smoking hot, but not all investments are going to get you high. Bitcoin rose almost 14X in 2017. Since then, however, it’s tanked to become the worst performer, by far, in 2018. Bitcoin was valued at $20,000/coin in December of 2017. Today, it trades for $3,600, for losses of 82%! Sadly, cryptocurrency has been rife with pump and dump schemes and MLM Ponzi scams, so buyer beware! Most investors lost a lot of money in 2018. NASDAQ lost 5%, the Dow Jones Industrial Average dropped 6%, gold prices sank by 3% and oil prices tanked by 25%. With stock and bond prices back near their all-time highs, investors should be taking a more defensive stance. Companies have been borrowing cheap money and buying back their own stock – using financial engineering to make their earnings look strong and their share prices look on sale. However, with the amount of risk that has now entered the marketplace, it’s important to remember that there comes a time when the price you pay to borrow is prohibitive, and you have to pay back your loans with earnings (rather than borrowing from Peter to pay Paul). In other words, no Wall Street party built on leverage lasts forever. 9. How long will it take for you to have a nest egg as big as your annual salary if you put 10% of your income into a tax-protected (and financial predator proof) individual retirement plan and invest in stocks and bonds*? 7 years. Based upon 10% average annualized returns of stocks and bonds over a 30-year period, which is about what those assets have done over the 30-year period, from 1989-2018. 10. How long will it take for your nest egg to earn more than you earn, if you put 10% of your income into a tax-protected (and financial predator proof) individual retirement plan and invest in stocks and bonds*? 25 years. Based upon 10% average annualized returns of stocks and bonds over a 30-year period, which is about what those assets did from 1989-2018. 11. What’s the best investment strategy in a slow-growth, high-debt world? Hard assets hold their value better than paper assets when there is too much paper floating around. Market timing doesn’t work, and you still need liquidity. So, it’s not a good idea to just put everything into cash and real estate. So, learn how to diversify properly (you don’t need 18-pages of holdings), avoid the Bailouts, add in hot industries, keep enough safe, overweight safe in volatile times and rebalance 1-3 times a year. Most hard assets are overpriced right now, so it offers a good period of time to research and determine exactly what is right for you. Value capital preservation more than reaching for yield. It will allow you to buy low when things are on sale. 12. Which countries hold the most gold? The United States is the top holder of gold worldwide, by far, with 8,133.5 tons, followed by Germany, the International Monetary Fund, All ETFs, Italy, France, Russia and China. China and Russia have been on a gold buying spree since 2008. Reports are that they will start trading oil and other commodities using their own currency backed by gold, breaking free from the dollar. (Click to read my report on Russia and Gold.) There are multiple reports that the U.S. banks and brokerages have been selling their client’s gold assets (sometimes without permission) in a price fixing scandal, which has kept gold prices in the U.S. and Europe lower than the rest of the world. Deutsche Bank settled a lawsuit, and agreed on Dec. 2, 2016 to name names of other banks that were price-fixing gold. 13. Are annuities safe? Insurance products, including life insurance and annuities, aren't insured by the FDIC. If we had not bailed out AIG in 2007, more than 50 million annuity holders would have been in real trouble. Your annuity product is only as safe as the insurance company that is selling it to you. Recessions are hard on insurance companies, so we may see some troubled insurance companies in the next recession (as we did in the Great Recession). Insurance products are like being a renter. If you can’t pay, you get tossed out. Many people pay for life insurance their entire working life, and then can’t pay when they retire – when they are really most in need. If you put that money into your own tax protected account, you could save on taxes, compound your gains, and it would be there for you when you retire, even offering some income, in addition to the capital.  (c) Natalie Pace. 2019. All rights reserved. 14. What is the 3-Ingredient Recipe for Cooking up Profits? 1. Start with what you know and love 2. Pick the Leader 3. Buy low; sell high (easy to say; hard to do) This recipe, along with my Stock Report Card, Four Questions, market strategies and data drilling are how I earned the ranking of number one stock picker. The recipe is easy. Learning how to use these tools requires practice. You must begin by locating and analyzing data, which is actually more less time and more informative than trying to read articles to figure out what to invest in. Articles provide a sliver of the data that is available, once you know where to look, and come with opinions, many of which are immature, incomplete and inexperienced. Come to my next Investor Educational Retreat to learn firsthand (from me) how easy and effective this strategy is, and why it has worked through bull and bear markets for more two decades now, while most strategies have bankrupted investors. 15. What are the Four Questions for Picking Winning Stocks? The Four Questions for Picking Winning Stocks. 1. What’s the product? 2. Who’s the customer? 3. Can the company continue to make a superior product going forward and get it to their customer at the best price before the competition? 4. Who’s the CEO and can s/he motivate the employees to make the best product faster, better and cheaper than the competition? As you can see, three out of four questions can be answered by being a good customer of the company, and the 3rd question can be answered by completing a Stock Report Card. So, the more you know about a company (ingredient #1 of the recipe for Cooking Up Profits), the easier it is to pick the leader. In Put Your Money Where Your Heart Is, I used these questions and tools to compare two companies. The one that everyone questioned, which I gave an A to, went on to become one of the most successful IPOs of all time (Google). The Wall Street darling Blue Chip, which I gave a D- to, went on to declare bankruptcy (General Motors). FYI: I identified both of these trends years before these major events occurred. The book was written in 2006, three years before GM went bankrupt. I applauded Google on national television before its IPO, when most pundits pooh-poohed it. This is the power of asking the right questions, rather than just listening to the mainstream media. 16. What were the top performing and the worst months for stocks over the past five years? November, July, February & May performed best over the 5-year period (in that order), on average. December, January and September were negative months. 2019 Retreat Attendees receive charts of the top-performing months and election year trends. If you’re interested in learning more about our 3-day, life transformational investor educational retreats, call 310-430-2397 or email info @ NataliePace.com. 17. What was the top performing 2-month period for stocks over the past twenty years? March & April – the Spring Rally – performed the best over the 10 and 20-year period, but saw only a little over 1% rise in the 5-year trend. December 2018 was the worst performing December in history, killing the historical returns of the Santa Rally. Understanding seasonal trends can help you with your annual rebalancing in your nest egg, and with your selling strategy for your trading. I spend one full day on what’s hot, teaching you how to identify the best investments of the year, in my Investor Educational Retreats. 18. What was the worst investment in 2018, NASDAQ, gold, the Dow Jones Industrial Average, bonds, cannabis or real estate? Bitcoin and cryptocurrency were the worst investments in 2018 – losing 3/4ths or more of their value. (If you were caught up in a pump-and-dump scam, then you likely lost it all.) It was easy to lose money in 2018. Stocks lost money. Bonds lost money. Oil tanked by 25%. Gold miners dropped another 13.7%. Real estate prices continued to rise, but remain unaffordable to locals in many of the cities with the strongest job opportunities. I spend one full day at the Investor Educational Retreats on What’s Safe and How to Get Safe. Call 310-430-2397 or email info @ NataliePace.com to learn more. 19. Which year is expected to perform better, 2019 or 2020, based upon historical returns of election years? 2019 is a pre-election year. Pre-election years are rock stars historically, boasting average annual gains of 15.6% over the last three decades. However, over the last decade, the pre-election year has been the worst performer. 2000, an election year, was the beginning of the Dot Com Recession. 2008, an election year, ushered in the devastating Great Recession. 20. How many companies are in the Dow Jones Industrial Average? 30 companies. Many are household brands. And many are carrying far more debt than the value of the company. Leverage has begun to concern economists. If you don’t understand how much debt corporations are holding, it’s time to learn The ABCs of Money that we all should have received in high school. General Electric isn’t the only blue chip that is likely to slash its dividend and lose market value. Click to access the names of the 30 companies. The Dow Jones Industrial Average was launched in 1896. 21. How many Dow Jones Industrial Average companies were bailed out or went bankrupt in the Great Recession? Most don't realize that 20% of the companies of the Dow (6 companies: AIG, American Express, Bank of America, Citi, JP Morgan and General Motors) were bailed out or went bankrupt in the Great Recession. Others, like General Electric and Ford, received support. New Chips are far safer, and higher performing, than Blue Chips, both in terms of growth, but also in terms of the fiscal health of their balance sheets. Learn more about how to add in performance and avoid the bailouts in your funds and retirement account at the Investor Educational Retreat and in The ABCs of Money. Since the Great Recession, the NASDAQ Composite Index has offered far superior returns than the Dow Jones Industrial Average, even factoring in dividends. In fact, the higher the dividend, the higher the risk. *All highlighted phrases are explained in greater detail at the Natalie Pace Investor Educational Retreats. Call 310-430-2397 or email [email protected] to learn now. Yesterday our team was told yet another story about someone who lost it all by trusting in the "free" advice of a financial advisor. Learn the truth about commissions & conflicts of interest & how to get a 2nd opinion now in my blog “The High Cost of Free Advice.” Know what you own. Stay free! Data Sources: (c) 2018 Morningstar Direct and The National Association of Realtors. All rights reserved. Used with permission. The information contained herein: (1) is proprietary; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar, the National Association of Realtors, Natalie Pace, nor any content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Other Blogs of Interest The State of the Union CBD Oil for Sale. The High Cost of Free Advice. Apple's Real Problem in China: Huawei. 2019 Crystal Ball. 2018 is the Worst December Ever. Will the Feds Raise Interest Rates? Should They? Learn what you're not being told in the MSM. Why FANG, Banks and Your Value Funds Are in Trouble. When the Santa Rally is a Loser, the Next Year is a Bigger Loser. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Trade Deficit Hits an All-Time High. Wall Street Plunges 800 Points. How to Protect Yourself. Rebalance and Get Safe in December. Here's Why. The Best Investment Decision I Ever Made. Thanksgiving 2018 Stocks Losses. Black Friday Sales. Get a 2nd Opinion on Your Current Investing Strategy. What's Safe for Your Cash? FDIC? SIPC? Money Markets? Under the Mattress? The Real Reason Stocks Fell 602 Points on Veterans Day 2018. Will Ford Bonds Be Downgraded to Junk? 6 Risky Investments. 12 Red Flags. 1 Easy Way to Know Whom to Trust With Your Money. Whom Can You Trust? Trust Results. October Wipes Out 2018 Gains. Will There Be a Santa Rally in 2018? The Dow Dropped 832 Points. What Happened? Bonds are In Trouble. Learn 5 Ways to Protect Yourself. Interest Rates Projected to Double by 2020. 5 Warning Signs of a Recession. How a Strong GDP Report Can Go Wrong. Should I Invest in Ford and General Electric? Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable however NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed