Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

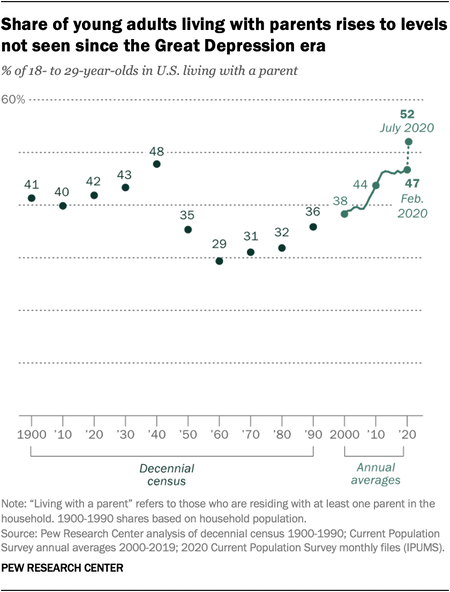

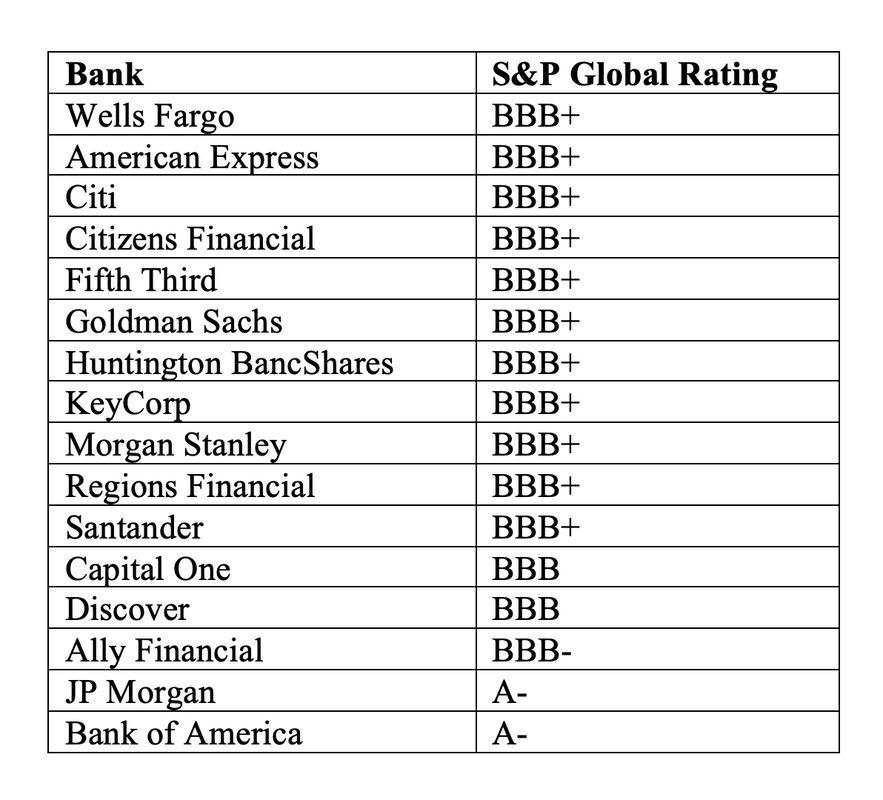

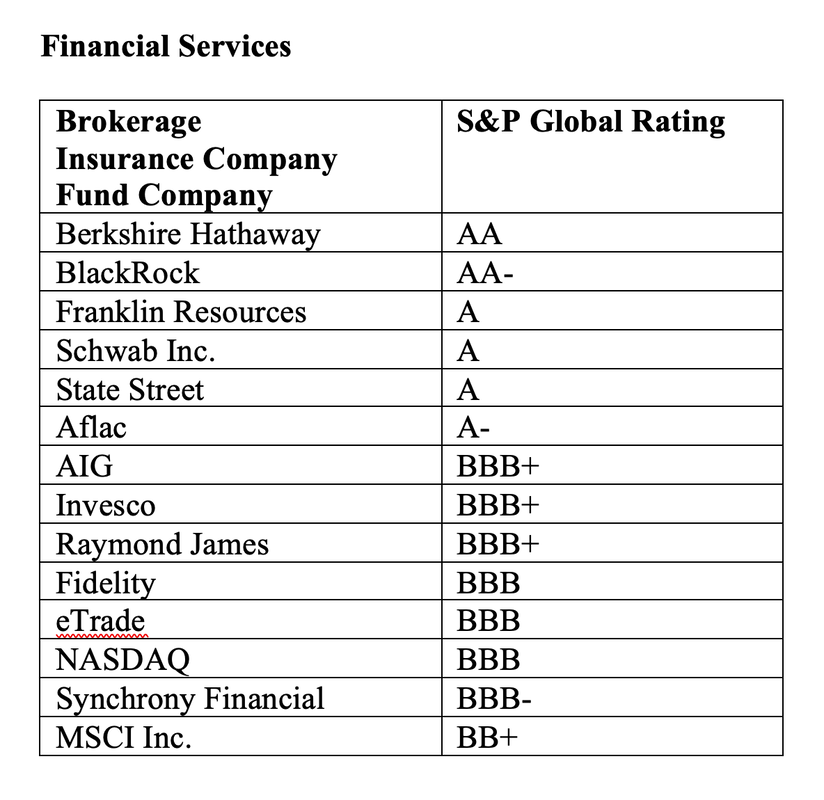

Dear Natalie, I asked my broker if I should be re-examining things, and he said, “No, we’re in a bull market.” When I asked again, he said, “Wait until after the election. The stock market will do great if Trump is re-elected.” However, I’m not convinced that waiting is the right thing to do, particularly since I remember my freak-out in March, when my nest egg was down by 35%. Can you offer some clarity? Signed, Confused. I Don’t Know Who or What to Believe. Dear Worried (and Rightfully So), First off, when you don’t know who or what to believe, trust results. By that I mean, always grade your guru before you listen to anything he says. For instance, you mentioned that your portfolio was down 35% between February 19, 2020 and March 23, 2020. If that was the case, then you are riding a Wall Street rollercoaster. When it goes up, your wealth increases. However, when it heads south, you’re vulnerable. That Buy & Hope plan has been losing more than half in each of the last two recessions. Additionally, most plans that go in whatever direction that the market does, perform about 2% under the general marketplace returns, due to fees. It’s better to be early than late. As you noticed in March, if you wait for the headlines, it’s too late to protect your wealth. So, waiting until after the election to fix a broken plan isn’t a good idea. If you look at your 2018 statements, you might notice that you also lost money in 2018. If you had the same plan in the Great Recession, then chances are quite high that you lost 55% or more, and then spent the next 7.5 years hoping and praying to recover, instead of earning gains. At the bottom of the market, the sales pitch shifts to, “If you sell now, you’ll be selling low.” There is a time-proven plan that earned gains in the Great Recession and outperformed the bull market in between. That plan is outlined in The ABCs of Money and taught at our Investor Educational Retreats. It’s also enthusiastically endorsed by Nobel Prize winning economist Gary Becker and the chairman of TD AMERITRADE, Joe Moglia (along with the many happy Main Street investors who use this system). Listen to Nilo Bolden describe her experience by clicking on her name. In other words, this plan has a Ph.D. in results.  Visit NataliePace.com to learn more about the easy nest egg strategies that saved Nilo's wealth. A well-designed plan doesn’t lose more than half in recessions. It protects you from market downturns, while allowing you to build wealth during bull markets. This plan is easy-as-a-pie-chart. Buy & Hold broker-salesmen don’t implement this plan because their own monetization and wealth strategy doesn’t profit from it. There are brokerages that are leaning into Modern Portfolio Theory with annual rebalancing – the cornerstone of the ABCs of Money. (Buy & Hold brokers say they use MPT. However, when you look at your portfolio, even if there are 20 pages of holdings, chances are very high that you are not properly diversified.) You are the boss of your money. Take ownership. You wouldn’t learn cooking from a chef who burns meals. My guess is that you are also worried because what your broker-salesman is saying doesn’t make sense. In fact, stocks fare better under Democrats (this is well-known on Wall Street). While your broker says we’re in a bull market, you’re seeing a lot of disturbing signs of the current recession. There are plenty of them. Unemployment is about 11%, according to Jerome Powell, speaking to the National Association for Business Economics on October 6, 2020 (click to read). (Read my blog to learn how the BLS has been underreporting unemployment.) There are currently 26.5 million people taking some kind of unemployment. Office buildings, apartment buildings and malls are ghost towns. 52% of 18-29 year-olds are living with a parent. This is higher than the Great Depression. The 1st and 2nd quarter 2020 GDP reports were contractions of -5% and -31.4%, respectively. Airlines and states are laying off workers in record numbers. Disney laid off 28,000 employees on September 30, 2020. September 30, 2020 is the date the government stopped subsidizing companies for employees who aren’t working.  Revenue in industries like travel, airlines, casinos and more is down by more than 80%. At the same time, over half of the S&P500 is at or near junk bond status – including a lot of U.S. banks and brokerages. As a reminder, a lot of our banks, brokerages and insurance companies wouldn’t even be in business if we hadn’t bailed them out in 2008. Have you really gotten a true picture of the economy from your broker?

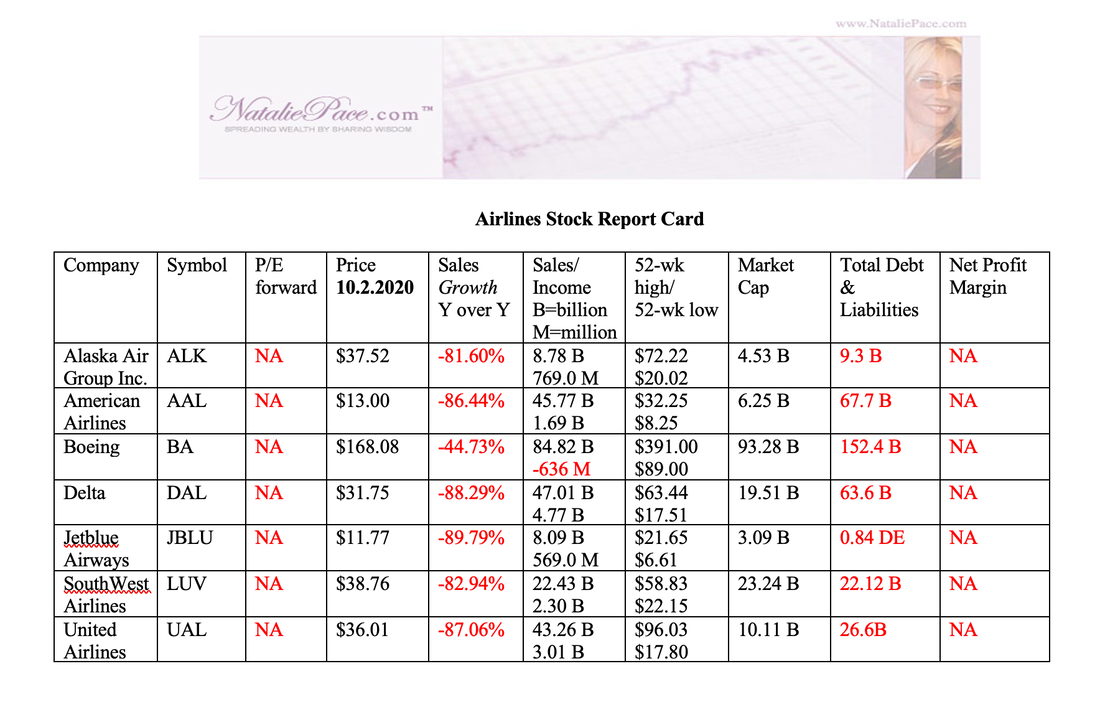

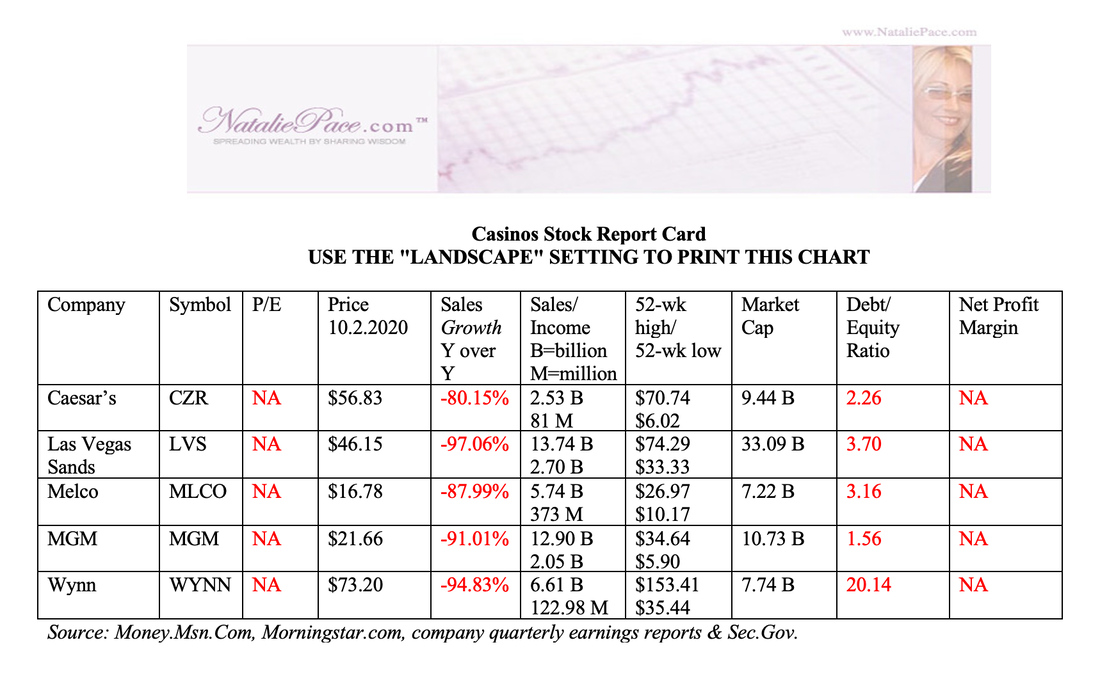

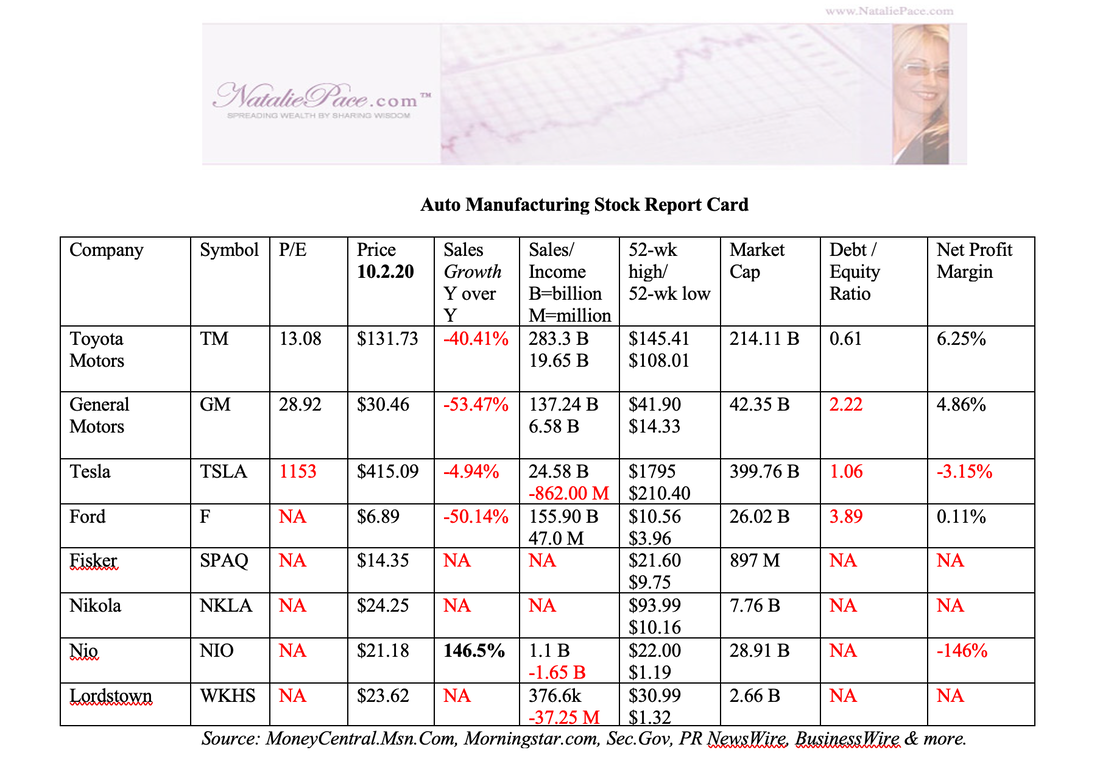

The Federal Reserve has purchased 1000 bonds and a lot of bond ETFs to try and keep things afloat – so that there is a more orderly procession through the bankruptcy courts for those companies that need to restructure their debt. (The Feds are not supposed to purchase stocks. A Wall Street insider told me that he thinks they might be, however.) Jerome Powell told Congress that, “Our actions, taken together, have helped unlock more than $1 trillion of funding, which, in turn, has helped keep organizations from shuttering, putting them in a better position to keep workers on and to hire them back as the economy continues to recover.” Here are a few Stock Report Cards on some of the more hard-hit industries. Click on the report card to access a blog, where you can get additional information on airlines, casinos and auto manufacturers (including EVs and China's Tesla).

When companies restructure, your bonds lose money. In general, bonds are illiquid and negative-yielding. Listen to my interview with Kathy A. Jones, the Chief Fixed Income Strategist at Charles Schwab Inc. on my YouTube channel for additional information on the risk in bonds, and what you can do about it. Fixed income is a word used in financial services for the “safe” side of your portfolio. Fixed income means your principal should stay intact, while you earn a predictable income. However, as you will learn in my interview with Kathy Jones, bonds are not living up to the name fixed income. You’re not getting the promised yield, and you could lose principal on your investment. This is a problem because the safe side is supposed to help keep your portfolio buoyant in troubled times. Bonds did that in the Great Recession and the Dot Com Recession, but are as risky as stocks in the current recession. These are all facts. If you knew where to access the official statistics and data, it would be easy to confirm. (I’ve provided links to many of the government agencies that provide the data. Just click on the blue-highlighted words to access them.) You can access other experts explaining what’s really going on in the economy by scrolling through the videos on my YouTube.com/NataliePace channel. There you will find my interview with Howard Silverblatt, the Senior Index Analyst at the S&P Dow Jones Indices (home to the S&P500®), who candidly told our viewers that stock prices are so high he needs to get a Kleenex because his nose is bleeding. Federal Reserve Board chairman Jerome Powell has been very candid about the challenges of the current recession. When he testified before Congress on September 22, 2020, he said, “The path ahead continues to be highly uncertain… A full recovery is likely to come only when people are confident that it is safe to reengage in a broad range of activities.” The Bottom Line We are in an unprecedented recession. The economy is being propped up with a flood of cash, the buying of almost 1000 bonds, a moratorium on evictions and foreclosures, paying people who don’t go to work, and broker salesmen who tell their clients not to do anything. That is always the case in recessions, which is why it typically takes about 18-24 months for stock prices to hit rock bottom. Everyone waits, until something terrible happens. There are a series of unfortunate events that cause a sell-off each time. Then things stabilize (or in the case of 2020 recover). Then another terrible thing happens, followed by another a few months later, again and again, until the bottom is finally reached. If you wait until the headlines and brokers turn apocalyptic, which they always do at the bottom of the market after a carnage of client losses, it will (obviously) be too late to protect your wealth. In fact, at that point, it would be a better idea to buy low. However, if you have lost half of your wealth and all of your liquidity, then you won’t be in a position to buy low. When things are over leveraged, it is really only a matter of time before some industries and companies have to restructure and change their business plan. We’ve seen that with retail for two years now. The airlines, the travel industry, casinos, commercial real estate, auto manufacturing, hospitality and many more industries are in trouble. As you can see in the Stock Report Cards above, many have lost more than half of their revenue. Most of these industries, including our banks, were highly leveraged before the pandemic. As I’ve said many times, more than half of the S&P500® are at or near junk bond status, including a lot of financial services companies. In adverse times, speculative companies have a lot of trouble. You don’t want that trouble to come on your dime. The right answer is not to sell everything and go live in a yurt. It is to be properly diversified and protected, and to know what is safe in a world where bonds are illiquid and negative yielding, money market funds have redemption gates and liquidity fees, stocks and real estate are overpriced and insurance companies and banks are in the large group hanging out just above junk bond status (and would not be in business if we hadn’t bailed them out in 2008). Losing more than half every eight to ten years and then spending the bull market crawling back to even is a Wall Street roller coaster and a terrible plan. A better strategy is to protect your wealth and liquidity, so that when asset prices tank, you have the capital to buy low. A properly diversified plan allows you to benefit from bull markets – even mini bull markets that are manufactured during a recession (and could be short-lived). Editor’s Note: All of the blue-highlighted words above link to blogs where you can learn more. There is also a list of recent blogs below.  Natalie Pace New Year, New You Wealth Empowerment Retreat. Jan. 16-18, 2021. Call 310-430-2397 to learn more. Other Blogs of Interest The October Surprise Is Your Bank a Junk Bond Do Stocks Fare Better Under Democrats or Republicans? Put Your Money Where Your Heart Is. Crystal Ball for the Remainder of 2020 (Including the Election). Microcap Gaming Company Doubles 2Q 2020 Revenue. Apple & Tesla Stock Splits. Schwab's Chief Fixed Income Strategist on What's Safe. China's Tesla (Nio). 2Q Sales Soar. Why Are You Still Renting? (Errr. There is More Than This to Consider!) MedMen's Turnaround Plan Attracts A-List Board Members. Wealth Myths That Keep You Poor. Prosperity Truths That Make You Rich. Protecting Your Wealth and Home in a Recession. Technology and Silver are Golden. The Economy Contracts 32.9% in the 2nd Quarter of 2020. Real Estate: Feeling Equity Rich? Make Sure That Feeling Isn't Fleeting. Airline Revenue Plunges 86%. 10 Questions for College Success Bank Earnings Season. Crimes. Cronyism. Speculation. Real Estate Solutions for a Post-Pandemic World. Copper and Chile Update. Gold Soars. Some Gold Funds Tank. Will the Facebook Ad Boycott De-FANG Stocks? Why Did My Cannabis Stock Go Down? Which Countries Are Hot in a Global Pandemic? Is Your Financial Advisor Good at Navigating Stormy Seas? $10 Avocados, Lies, Damn Lies, Statistics & Wall Street Secrets. It's Never a Crash. Work From Home and Intergenerational Housing. Biotech Races for a Coronavirus Cure. Are You Worried About Money? May is a Good Time for Rebalancing. Is FDIC-Insured Cash at Risk of a Bank Bail-in Plan? Why Did my Bonds Lose Money? Cannabis Update. Recession Proof Your Life. Free Videocon Monday, May 10, 2020. The Recession will be Announced on July 30, 2020. Apple Reports Terrible Earnings. We Are in a Recession. Unemployment, Rising Stocks. What's Going On? 8 Money Myths, Money Pits, Scams and Conspiracy Theories. 21st Century Solutions for Protecting Your Home, Nest Egg & Job. Wall Street Insiders are Selling Like There is No Tomorrow. Why Are My Bonds Losing Money? Tomorrow is Going to be Another Tough Day. Price Matters. Stock Prices are Still Too High. Should You Ride Things Out? 7 Recession Indicators Corona Virus Update. The Bank Bail-in Plan on Your Dime. NASDAQ is Up 6X. CoronaVirus: Which Companies and Countries Will be Most Impacted. Is Tesla Worth GM and Ford Combined. Artificial Intelligence is on Fire. Is it Time to Buy S'More? Take the Retirement Challenge. 2020 Investor IQ Test. Answers to the 2020 Investor IQ Test. The Cannabis Capital Crunch and Stock Meltdown. Does Your Commute Pollute More Than Planes? Are Health Care Costs Killing Your Budget? 2020 Crystal Ball. The Benefits of Living Green. Featuring H.R.H. The Prince of Wales' Twin Eco Communities. What Love, Time and Charity Have to do with our Commonwealth. Interview with MacArthur Genius Award Winner Kevin Murphy. Unicorns Yesterday. Fairy Tales Today. IPO Losses Top $100 Billion. Price Matters. Will There be a Santa Rally? It's Up to Apple. Harness Your Emotions for Successful Investing. What the Ford Downgrade Means for Main Street. The Dow Dropped Over 1000 Points Do We Talk Ourselves into Recessions? Interview with Nobel Prize Winning Economist Robert J. Shiller. Ford is Downgraded to Junk. Gold Mining ETFs Have Doubled. The Gold Bull Market Has Begun. The We Work IPO. The Highs and Hangovers of Investing in Cannabis. Recession Proof Your Life. What's Your Exit Strategy? It's Time To Do Your Annual Rebalancing. Are You Suffering From Buy High, Sell Low Mentality? Financial Engineering is Not Real Growth. The Zoom IPO. Uber vs. Lyft. Which IPO Will Drive Returns? Boeing Cuts 737 Production by 20%. The Lyft IPO Hits Wall Street. Should you tak Cannabis Doubles. Did you miss the party? 12 Investing Mistakes The High Cost of Free Advice. 2018 Was the Worst December Since the Great Depression. Russia Dumps Treasuries and Buys Gold OPEC and Russia Cut Oil Production. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed