Natalie Pace Blogs

Photo of Natalie Pace by Marie Commiskey. Avalon Photography.

|

|

|

|

|

|

|

|

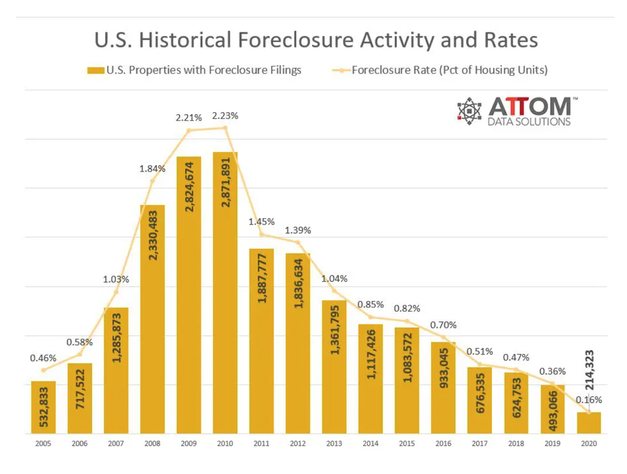

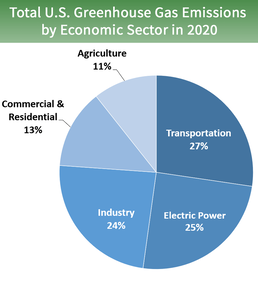

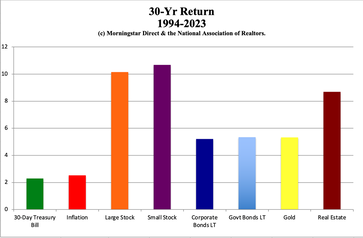

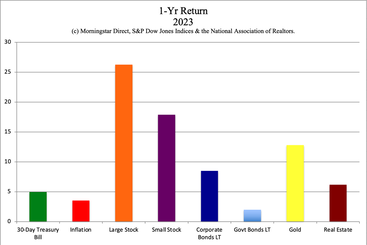

9 Inflation, Budgeting, Debt & Investing Solutions. Save Thousands. Earn Money While We Sleep. In today’s inflationary world, it’s easy to feel overwhelmed, to put too much on our credit card, to get into trouble with debt, and to stop saving/investing toward our own future and for unforeseen emergencies. However, there are solutions that can reverse this trend, even in today’s world of high prices. The cure for a world that doesn’t add up lies in increasing our income and decreasing our expenses. That might feel impossible. Yet there are many ways that we can do this, nine of which are listed below. The changes we need to embrace are not found in the mainstream. (Otherwise, everyone would be adopting them, and we would all be living the life of our dreams!) We have to stop our money from flying out the window, and start keeping more of it for ourselves. When we learn how to: · Stop making everyone else rich at our own expense, · Keep more of our income with smarter choices, and · Start earning money while we sleep… We begin increasing our wealth and living a richer life. (It’s also better for the planet.) Here are the topics we will cover in the blog. Should I buy a home? Should I cut out café lattes and avocado toast? Should I move away from the expensive city? Almost half of my income is going on housing! I’m only spending $35 a week on gasoline and about $120 a month on utilities. Food has gotten so expensive! I’ll start investing once I pay off my debt Health Savings Account Which brokerage account should I open? And here is more information on each topic. Should I buy a home? Buying a home allows us to stop making the landlord rich. However, if we buy high and the value of our home drops precipitously, that could ruin our credit score, our lives, and our livelihood for a very long time. It’s important to know two key facts about homeownership, and to make sure that we are buying a home we can afford, for a good price, in a community with good neighbors. I outline 10 questions to ask/answer before buying a home in the Real Estate section of The ABCs of Money, 5th edition.  What are two compelling facts about homeownership? Buying a home is highly correlated with wealth. The mean net worth of homeowners is nearly 10 times that of renters, at $1,530,900 versus $154,900 (source: Federal Reserve Board). Over 20 million American homes were foreclosed on before, during and after the Great Recession (source: AttomData).  Should I cut out café lattes and avocado toast? Skipping daily Starbucks could save us $1825 or more every year. That’s a lot of money. If you’re making Starbucks rich, consider what you might enjoy a lot more than a warm drink. (Massages? A weekend getaway?) However, most of us are having trouble making ends meet because of the strangling costs of housing, transportation, insurance and food – our basic needs. If we can get creative about reducing those expenditures, we now have a springboard from which to launch the life of our dreams – to thrive, instead of feeling buried alive in bills. Keep reading for a few ideas. Should I move away from the expensive city? Many cities have become unaffordable. The temptation is to move away, and try to convince our employers to let us work from home. Working from home could save us thousands of dollars each year, and a boatload of time that we don’t spend commuting. Whether we stay in the metro or move to the suburbs, if we can work from home at least a few days of the week, we’ll save a lot of time and money. Cities offer metros, bike lanes and other affordable ways to get around. We don’t need to own a car or pay for car insurance, car payments, maintenance or gasoline in cities that offer these amenities. That’s potentially worth $8,000 or more on average per vehicle. If we move into a more affordable area for housing, we should factor in the extra money we’ll pay on transportation and the time we’ll spend sitting in traffic before we take the leap. There may be other ways to reduce our housing expenditures that won’t require gridlock. Since transportation is the biggest CO2 emitter in the U.S., city dwellers tend to have a much lower footprint than suburbanites.  Source: EPA.gov Almost half of my income is going on housing! When 30% or more of our budget is going toward housing, we might not have enough left over for food. Unplanned expenses might have to go on credit cards. This is a road to debt servitude. The way to thrive is to keep our basic needs under 50% of our income, including housing, transportation, taxes, food, insurance, etc. Read the Thrive Budget section of The ABCs of Money, 5th edition for a step-by-step guide on how to do this. One way that people are reducing their housing costs is by sharing a home. Intergenerational housing is higher today than it was in the Great Depression. Saving money on housing could mean that we have a down payment to buy a home in the coming years. Thinking of our parents, grandparents and kids in an intergenerational wealth plan is one of the most powerful ways to keep the money in the family and stop making the landlord rich. Every cent we own and every moment we spend is always an investment. Cohousing can also be a way to reduce student debt. Should you au pair while in college, or live with an elderly adult? Would both of you eat better as a result? Getting creative about the benefits of shared living space could be the biggest gamechanger in our budget, as that is by far one of the biggest expenses – adding up to tens of thousands of dollars saved annually! Cohabitating could save us almost $20,000 Cohousing is one way that single mothers can keep $19,000 or more a year for themselves, in savings on housing, groceries, childcare and transportation. Having another adult in the home gives us more personal time, which improves our mental health and decreases feelings of isolation. (There was a funny, classic play, film and TV show about two divorced men sharing an apartment, called The Odd Couple.) Check out my interview with CoAbode’s founder and chairman Carmel Boss at YouTube.com/NataliePace. FYI: As a young, single mother, I shared a home with another single mom. It was one of the pivotal choices I made to create this life that I love. Many other successful women have done the same, including Gloria Allred. I’m only spending $35 a week on gasoline and about $120 a month on utilities. $35/week is $1825/year. $120/month is $1440/year. Any corporation that can make the monthly bill low enough has a chance of attaching a leech to your body that siphons your money over to them. Think of all of these little bills, including streaming services, life insurance, email providers, banks, etc., and see just how many of them you really need. Is there a way that you can eliminate the bill altogether, or reduce the price dramatically? A personal energy audit could save us $4000 annually – more if your weekly gasoline or monthly utility bills are higher. As I mentioned above, the average person spends about $8,000/year on each vehicle, when you factor in the car payment, gasoline, insurance and maintenance. Imagine what kind of bucket-list vacation you might take, or how fast you could stockpile a down payment for a house, if you weren’t making the gas station, utility, insurance company and car manufacturer rich. Reducing our energy costs can be done with simple energy efficiency upgrades on our living space, and by carpooling, taking mass transportation and/or walking/biking more. Yes, this requires a little personal education and rethinking of our lifestyle. However, when the carrot can be so much money, it’s worth being courageous about our choices. Oftentimes, the change offers increased fun and health for us. For example, walking to the store and for errands, instead of driving, can improve our physical health. Food has gotten so expensive! Food costs increased 2.2% over the past year (source: BLS.gov). We’ve also discovered that some of our food has high levels of pesticides, which are unhealthful (could increase our medical costs). If we spend $250/month on produce, we could save $3,000/year by growing our own vegetables. If we live in an apartment or rent, this still might be possible in a community garden, like the Compton Community Garden. If we are busy professionals, there might be an organization that does this for us, like Good Neighbor Gardens. If we want to have healthier food choices and a more engaging learning environment for our children, there are many organizations that help us to plant student gardens. Check out the Kids and Food/Soil episodes of the Earth Gratitude docuseries for ideas and resources. I’ll start investing once I pay off my debt At the top of this blog, I said that one of the solutions to a budget that has us struggling to survive is to increase our income by earning money while we sleep. Investing allows us to do that. Compounding is so powerful that the sooner we start, the better off we’ll be for our entire life! Depositing 10% of our income into an IRA or 401(k) and having that 10% earn an annualized 10% gain means that we will have more money in our retirement account than we earn in 7 1/2 years, and our money makes more than us in 25 years.  Source: NataliePace.com Think it’s hard to make a 10% annualized gain? The average returns of stocks over the last 30 years have been 10%.  Source: Morningstar Direct, S&P Dow Jones Indices, National Association of Realtors. The S&P500 earned 26.3% in total return in 2023!  Source: Morningstar Direct, S&P Dow Jones Indices, National Association of Realtors. A debt problem is a budgeting problem. So, the solutions outlined above will help us to stop putting bills on credit cards. Reducing the amount we owe can be a little trickier. There is a Debt section in The ABCs of Money, 5th edition, and a free video coaching series on the Thrive Budget Life Hacks at YouTube.com/NataliePace. The leaps we take to reclaim our life by earning money while we sleep and living within our means (with creative choices that keep the money in the family) go a long way to solving our debt problem. Health Savings Account If we are healthy and spending an arm and a leg on health insurance, health savings accounts could save us thousands annually. We’ll still have health insurance (at a very high deductible) for emergencies. However, we could save thousands annually in premiums, while also receiving a tax credit for the amount we deposit into our HSA. Learn more about HSAs in The ABCs of Money, 5th edition and at IRS.gov. Which brokerage account should I open? Since our goal is to stop making the taxman, the debt collector, the insurance salesman, the gas station, the utility company, etc. rich at our own expense, we want to be aware of all of the ways that we can pay less in taxes. The Health Savings Account mentioned above is one way. However, investing in tax protected retirement accounts is another. When we invest and compound within tax-protected retirement accounts, we avoid paying capital gains taxes. That can amount to savings of up to 37% of the gains. Billionaire Peter Thiel has $5 billion in his Roth IRA, according to ProPublica, which he never paid capital gains on, and will not even pay income taxes on when he starts his distributions (unless the laws change)! Billionaire Warren Buffett often admits that he pays a lower tax rate than his secretary. Each of his kids has their own foundation. (Protecting our wealth has a lot to do with setting up the proper accounts, organizations and corporations.) What kind of brokerage account should you open? Accounts to consider include:

Since retirement accounts allow us to invest and compound our gains without capital gains taxes, it’s a good idea to max out our contributions into these accounts and invest in them first, rather than just a traditional brokerage account. Bottom Line If we want to fly, we have to lighten our load. Earn more. Spend less. Invest more. Thrive more. When we learn the life math that we all should have received in high school, our life transforms immediately. When we start investing in things that we know and love, instead of just “paying bills,” our life will change immediately, and this world will become a much more beautiful place. A life like this increases in value every single day and becomes more valuable not just to us, but to those around us, as well. Join us at our April 27-29, 2024 Spring Financial Freedom Retreat. Learn how to protect your wealth, hedge against a weaker dollar, invest and compound your gains, green your retirement plan, easy and efficacious nest egg strategies, how to get hot and diversified (including in artificial intelligence and EVs), how to evaluate IPOs and other stocks, and what's safe in a Debt World. You'll even discover how to save thousands annually with smarter big-ticket choices. Yes, it's a complete money makeover. Email [email protected] to register. Learn the 15+ things you'll master and read testimonials in the flyer on the home page at NataliePace.com. Register with friends and family to receive the best price. "Ten minutes into the first day I was already much smarter about investing than I ever thought I would be in my life and I knew I was in exactly the right place at this retreat. I am amazed at how EASY and FUN it is to make my money work for me and those I love. I think this kind of information should be compulsory in schools. I wish I'd learned this sooner." CM If you’d like an unbiased 2nd opinion on your current wealth plan, email [email protected] for pricing and information.)  Join us for our Online Spring Financial Freedom Retreat. April 27-29, 2024. Email [email protected] or call 310-430-2397 to learn more. Register with friends and family to receive the best price. Click for testimonials, pricing, hours & details.  Join us for our Restormel Royal Immersive Adventure Retreat. March 7-14, 2025. Email [email protected] to learn more. Register by April 30, 2024 to receive $200 off the regular price. Click for testimonials, pricing, hours & details. There is very limited availability, and you must register early to ensure that you get the exact room you want. This retreat includes an all-access pass to all of our online training for a full year for two and three 50-minute private, prosperity coaching sessions!  Natalie Wynne Pace is an Advocate for Sustainability, Financial Literacy & Women's Empowerment. Natalie is the bestselling author of The Power of 8 Billion: It's Up to Us and is the co-creator of the Earth Gratitude Project. She has been ranked as a No. 1 stock picker, above over 835 A-list pundits, by an independent tracking agency (TipsTraders). Her book The ABCs of Money remained at or near the #1 Investing Basics e-book on Amazon for over 3 years (in its vertical), with over 120,000 downloads and a mean 5-star ranking. The 5th edition of The ABCs of Money and the 2nd edition of Put Your Money Where Your Heart Is are the most recent releases of these books. Follow her on Instagram. Natalie Pace's easy as a pie chart nest egg strategies earned gains in the last two recessions and have outperformed the bull markets in between. That is why her Investor Educational Retreats, books and private coaching are enthusiastically recommended by Nobel Prize winning economist Gary S. Becker, TD AMERITRADE chairman Joe Moglia, Kay Koplovitz and many Main Street investors who have transformed their lives using her Thrive Budget and investing strategies. Click to view a video testimonial from Nilo Bolden. Check out Natalie Pace's Substack podcast on Apple and Spotify. Watch videoconferences and webinars on Youtube. Other Blogs of Interest China & Russia Double Their Gold Holdings. 2024 Investment of the Year? The Reddit IPO. Meme Stock or Snap Land? Tesla's Factory in Germany Taken Offline by Activists. Bitcoin Sets a New Record High. The Importance of Rebalancing. Beyond Meat's Shares Surge. Quaker Oats' Pesticide Problem. Stocks are Flying High. Why Aren't Mine? Cut Your Tax Bill in Half. 9 Tips. Celebrity Jet CO2. Green Washing. The Facts. Some Solutions. Copper: Essential to the Clean Energy Transition. Uh. Oh. More Bank Trouble. Are Amazon, Square and Other Tech Companies Ripping Us Off? Housing. Unaffordable. What Works? Case studies and creative solutions. Don't Reach for Yield. Closed-End Funds. 2024 Investor IQ Test. Answers to the 2024 Investor IQ Test. Apple's Woes Drag Down the Dow. The Winners & Losers of 2023. Ozempic, Magnificent 7 & Beyond. 2024 Crystal Ball. The Underperforming DJIA, Full of Fossil Fuels and Forever Chemicals. A Spectacular Year for 3 of the Magnificent 7. The Best ROI* (Almost 40%!) & 7 Life Hacks That Save Thousands. Portugal Eliminates Tax Advantages for Ex-Pats. Holiday Gift Giving on any Budget. Including No Budget. Once in a Century Events are Happening Every Day. The Crypto Winter Enters Its 3rd Year. Earn $50,000 or More in Interest. Safely. Finally. Freebies and Deals for Black Friday and Cyber Monday. Auto Strikes End. EV Price Wars Continue. WeWork's Bankruptcy. Half-Empty Office Buildings. Problems in our Personal Wealth Plan. Solutions for Unaffordable Housing. Cruise Ships Give Freebies to Investors. Should You Take the Bait? Should You Take a Cruise? Bonds. Banks. The Treacherous Landscape of Keeping Our Money Safe. 7 Rules of Investing Air B N Bust? Barbie. Oppenheimer. Strikes. Streaming Wars. Netflix. Monero: A Token of Trust? 13 Lifestyle Choices to Reduce Waste, Pollution & CO2 & Save a Boatload of Dough. China Bans Apple 11-Point Green Checklist for Schools. Artificial Intelligence and Nvidia's Blockbuster Earnings Report Biotech in a Post-Pandemic World 10 Wealth Secrets of Billionaires and Royals. What Happened to Cannabis? Bank of America has $100 Billion in Bond Losses (on Paper) Lithium. Essential to EV Life. I'm Just Not Good at Investing. Investors Ask Natalie. Should I Buy an S&P500 Index Fund? Investors Ask Natalie. Bonds Lost More than Stocks in 2022. Do Cybersecurity Risks Create Investor Opportunities? I Lost $100,000. Investors Ask Natalie. Artificial Intelligence Report. Micron Banned in China. Intel Slashes Dividend. Buffett Loses $23 Billion. Branson's Virgin Orbit Declares Bankruptcy. Insurance Company Risks. Schwab Loses $41 Billion in Cash Deposits. Fiat. Crypto. Gold. BRICS. Real Estate. Alternative Investments. BRICS Currency. Will the Dollar Become Extinct? The Online Global Earth Gratitude Celebration 7 Green Life Hacks Fossil Fuels Touch Every Part of Our Lives Are There Any Safe, Green Banks? 7 Ways to Stash Your Cash Now. Lessons from the Silicon Valley Bank Failure. Which Countries Offer the Highest Yield for the Lowest Risk? Why We Are Underweighting Banks and the Financial Industry. 2023 Bond Strategy Emotions are Not Your Friend in Investing Bonds Lost -26%, Silver Held Strong. Save Thousands Annually With Smarter Energy Choices Is Your FDIC-Insured Cash Really Safe? Money Market Funds, FDIC, SIPC: Are Any of Them Safe? My 24-Year-Old is Itching to Buy a Condo. Should I Help Him? The 12-Step Guide to Successful Investing. The Bank Bail-in Plan on Your Dime. Rebalancing Your Nest Egg IQ Test. Answers to the Rebalancing Your Nest Egg IQ Test. Important Disclaimers Please note: Natalie Pace does not act or operate like a broker. She reports on financial news, and is one of the most trusted sources of financial literacy, education and forensic analysis in the world. Natalie Pace educates and informs individual investors to give investors a competitive edge in their personal decision-making. Any publicly traded companies or funds mentioned by Natalie Pace are not intended to be buy or sell recommendations. ALWAYS do your research and consult an experienced, reputable financial professional before buying or selling any security, and consider your long-term goals and strategies. Investors should NOT be all in on any asset class or individual stocks. Your retirement plan should reflect a diversified strategy, which has been designed with the assistance of a financial professional who is familiar with your goals, risk tolerance, tax needs and more. The "trading" portion of your portfolio should be a very small part of your investment strategy, and the amount of money you invest into individual companies should never be greater than your experience, wisdom, knowledge and patience. Information has been obtained from sources believed to be reliable. However, NataliePace.com does not warrant its completeness or accuracy. Opinions constitute our judgment as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors. Comments are closed.

|

AuthorNatalie Pace is the co-creator of the Earth Gratitude Project and the author of The Power of 8 Billion: It's Up to Us, The ABCs of Money, The ABCs of Money for College, The Gratitude Game and Put Your Money Where Your Heart Is. She is a repeat guest & speaker on national news shows and stages. She has been ranked the No. 1 stock picker, above over 830 A-list pundits, by an independent tracking agency, and has been saving homes and nest eggs since 1999. Archives

July 2024

Categories |

RSS Feed

RSS Feed